Factors matter, not assets因子比资产重要

Need to look through asset class labels to understand the factor content.

Assets are bundles一系列 of factors

Risk premiums reflect their underlying factor risks

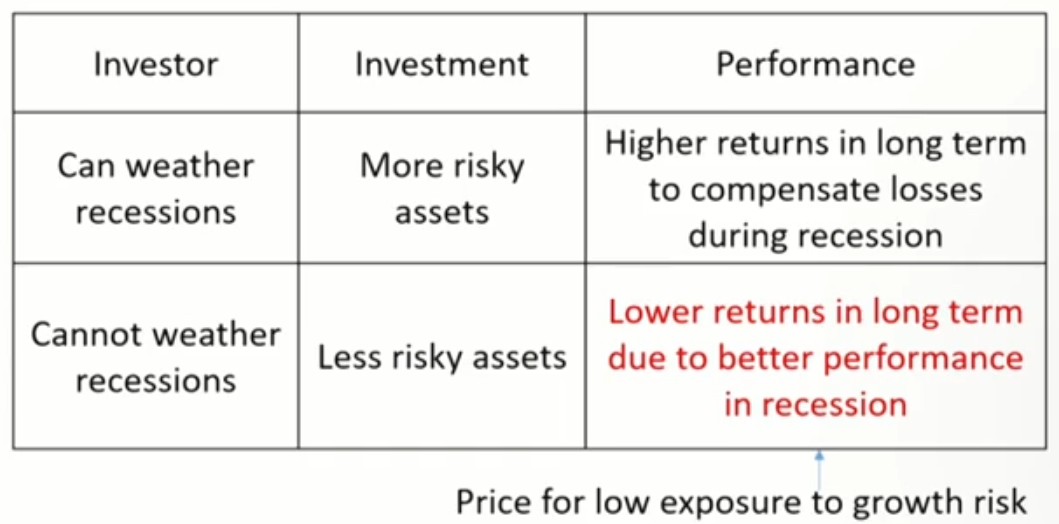

Different investors need different risk factors不同人对因子的需求不同

Different investors have different optimal exposures to different sets of risk factors

Bad times不景气时期: Each different factor defines a different set of bad times and the investors who bear these factor risks need to be compensated in equilibrium by earning factor risk premiums因子表现不好的时期

Risk premium: Investors are paid risk premiums in normal time一般市况 as compensation for taking risks单价

Exposure: Assets are bundles of factor risks, and it is the exposures to the underlying factor risks that earn risk premiums数量

Factor Theory and CAPM

An important theory of factor risk is the CAPM.

One factor: market factor. All risky assets have risk premiums determined only by their exposure to the market portfolio E\left(R_i\right)=R_f+\beta\left(R_m-R_f\right)

CAPM was revolutionary: the risk of an asset was not how the asset behaved in isolation but how that asset moved in relation(β) to other asset and to the market as a whole

Assumptions:

Investors are expected to make decisions solely in terms of expected values and standard deviations of the returns on their portfolios只取决于均值方差

Investor plan for the same single holding period单期投资,不调仓

Investor have homogeneous expectations or beliefs同质化假设

An individual cannot affect the asset price by buying or selling action (price taker)

All assets, including human capital, are tradable

Failures

The asset risk premiums depend only on the asset's beta and there is only one factor(market factor) matters

CAPM assumes that investors have only financial wealth没考虑负责

Investors have unique income streams and liabilities

Investors have mean-variance utility假设投资者是理性人 Asymmetric treatment of risk(more distressed by losses than pleased by gains)对风险和收益的效用不对称

Single-period investment horizon假设单期

Investors have homogeneous expectations假设同质化

In reality, investors do not all share the same beliefs

No taxes or transaction costs

Individual investors are price takers

The informed investor is trading and moving prices

Information is costless and available to all investors假设信息是无成本的

Lesson 1: Factor - Don't hold an individual asset, hold the factor

Individual stocks: are exposed to the market factor, which carries the risk premium, but also have idiosyncratic risk个体风险,which is not rewarded by a risk premium

Market factor portfolio: investors can diversify away the idiosyncratic part and increase their returns

Systematic risk: The market factor is systematic and affect all assets因子系统性影响资产

Lesson 2: Optimal exposure - Each investor has his or her own optimal exposure of factor risk

Investors have different proportions of the risk-free asset and the market portfolio.

Lesson 3: Risk premium - The factor risk premium is determined by risk aversion of average investor and the volatility of market波动性高、厌恶程度高导致风险单价高 E\left(R_{\mathrm{m}}\right)-R_f=\bar{\gamma} \sigma_m^2

\bar{\gamma} is the risk aversion of average investor平均厌恶程度: 100% in the mean-variance efficient (MVE) portfolio position is the risk aversion of the market. Utility=E(R)-\frac{1}{2} \gamma \sigma^2

The \beta is a measure of how that stock co-moves with the market portfolio, and the higher the co-movement, the higher the asset's beta

Higher betas mean low diversification benefits引入低\beta的资产对组合的分散化效果更好

If the asset pays off when the market has losses, the asset has a low beta在市场表现差的时表现好的资产有低\beta. If the payoff of an asset tends to be high in bad times, this is a valuable asset to hold and its risk premium is low代价是长期的收益少

Multifactor and EMH

Multifactor models recognize the bad times can be definedmore broadly than just bad returns on the market portfolio不同因子的不景气时期不同,平均表现更好

In equilibrium, investors must be compensated for bearing these multiple sources of factor risk

We denote the SDF as m which is an index of bad time.Any risk premium exists because it is compensation for losing money during bad times \begin{aligned} & m=a+b_1f_1+b_2f_2+\cdots+b_k f_k \\ & \mathrm{E}\left(R_i\right)-R_f=\left(\frac{\operatorname{cov}\left(R_i, m\right)}{\operatorname{var}(m)}\right)\left(-\frac{\operatorname{var}(m)}{E(m)}\right)=\beta_{i, m} \lambda_m\end{aligned}

Multi-beta relation for an asset's premium: \mathrm{E}\left(R_i\right)=R_f+\beta_{i,1} \mathrm{E}\left(f_1\right)+\beta_{i,2} \mathrm{E}\left(f_2\right)+\ldots+\beta_{i, \mathrm{k}} \mathrm{E}\left(f_k\right) E\left(f_K\right) is the risk premium of factor k B_{i k} is the beta of asset i with respect to factor k

Assume it is costly to collect information and to trade on that information

Active managers earn excess returns as a reward for gathering and acting on costly information

Active managers search for pockets of inefficiency, and in doing so cause the market to be almost efficient搜索信息使得市场靠近有效

The deviations from efficiency have two forms: Rational explanation: high returns compensate for losses during bad times.The key is defining those bad times因子不够 Behavioral explanation: Under-or overreaction to news or events(inefficient updating of beliefs or ignoring some information)反映错误; Structural barriers: e.g.entry of capital, regulatory requirements市场障碍

Factors

Types of factors

Assets are buffeted by risk factors.The risk factors offer premiums to compensate investors for bearing losses during bad times.

Macro, fundamental-based factors宏观因子

Economic growth

Inflation

Volatility

Investment factors可投资因子

Static factors静态: simply go long to collect a risk premium (e.g., market factors)做多就用收益

Dynamic factors动态: can only be exploited through constantly trading different types of securities做多+做空实现盈利

Macro Factors

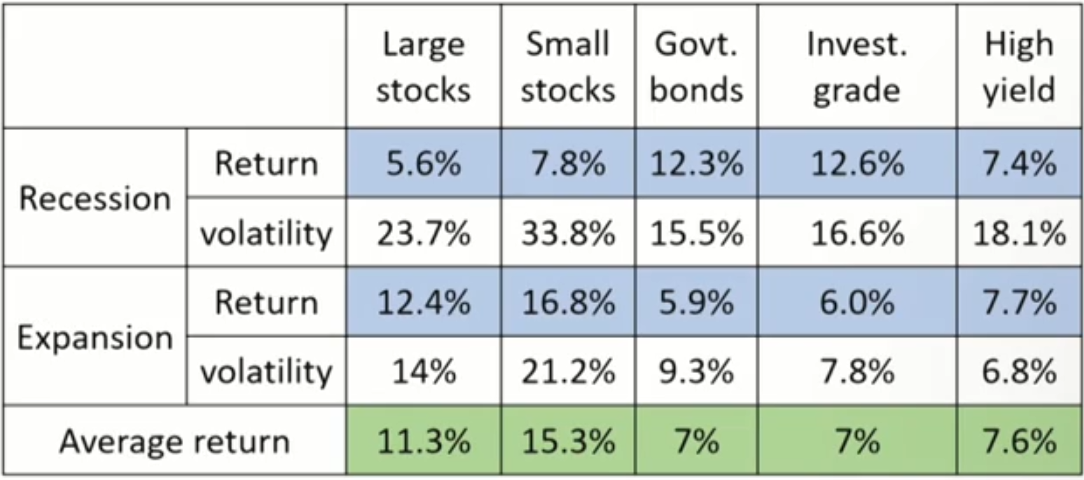

Macro factors affect all investors and the prices of assets.Although macro factors may have different impact on different investors, in general, bad outcomes of macro factors define bad times for the average investor.

A shock异动 to a factor matters more than the level of the factor

Economic growth

Volatility tends to be very high during bad times. All asset returns are much more volatile during recessions.

Risky assets generally perform poorly and are much more volatile during periods of low economic growth.

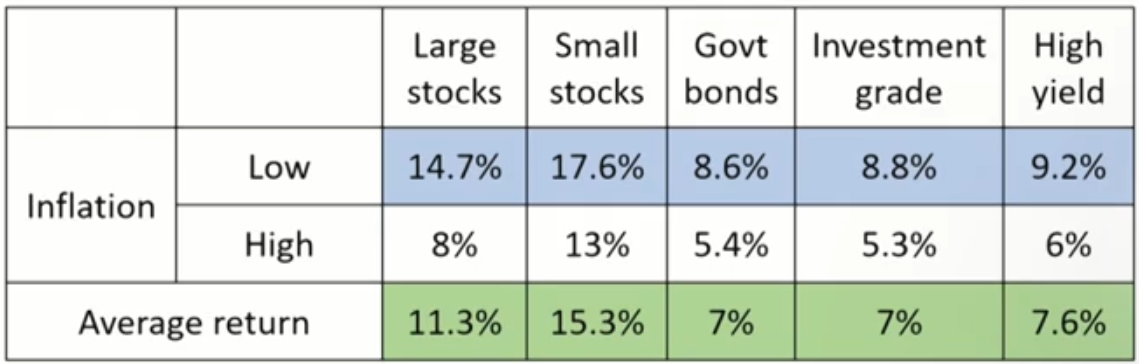

Inflation

High inflation tends to be bad for both stocks and bonds

Volatility

Volatility and stock returns: negative relations (leverage effect).

Bonds offer some respite during periods of high volatility高波动率时债券收益与波动率可能正相关

Manage volatility: Dislike volatility: Investors who is sensitive to volatility could increase bond position (but not always pay off in high volatility); Buy volatility protection (long put, volatility swap) Can afford volatility: sell volatility protection (short put); Sell volatility generates high and steady payoffs during stable times which compensate large losses in a huge crash (inevitable large losses that occur every decade).

Volatility is negatively linked to the returns of many assets and strategies.

Volatility is a factor with a negative price of risk: To collect a volatility premium requires selling volatility

protection.

Other macro factors

Productivity risk

Demographic risk

Political risk

Dynamic factors

Macro factors like inflation and economic growth cannot be directly traded.

Dynamic factors have a big advantage that they can be easily traded in investors' portfolios →long-short portfolio

Fama-French three-factor model: incorporates the systematic factors of market index, firm size (market capitalization) and book-to-market ratio: \mathrm{E}\left(R_i\right)=R_f+\beta_{i, M K T} \mathrm{E}\left(R_m-R_f\right)+\beta_{i, \mathrm{SMB}} \mathrm{E}(S M B)+\beta_{i, \mathrm{HML}} \mathrm{E}(H M L)

Size factors: The SMB factor was designed to capture the outperformance of small firms relative to large firms.

Since the mid-1980s there has not been any significant size effect

Responses to the disappearance of the size effect:

The original discovery of the size premium could have just been data mining Rational investors bid up the price of small cap stocks until the effect was removed

Value factors: Long value stocks and short growth stocks.

Growth stocks成长股: low book-to-market ratios

Value stocks价值股: high book-to-market ratios

Rational theories of the value premium Flexibility of response to shock: value firms and growth firms differ in how flexible they are and how quickly they can respond to shocks. Value firms are riskier because they cannot shift their firm activities to more profitable activities in bad times (high and asymmetric adjustment costs)价值股不灵活

Bebavioral theories of the value premium Overreaction or overextrapolation: investors tend to overextrapolate past growth rates into the future.

Value stocks are cheap because investors underestimate their growth prospects.价值股被低估

Growth firms are expensive because investors overestimate their growth prospects.成长股被高估

Momentum factors: to buy stocks that have gone up over the past six (or so) months (winners) and short stocks with the lowest returns over the same period(loser). Momentum is also called "trend" investing

Momentum effect: winner stocks continue to win and losers continue to lose.

Four-factor model(Carhart model) \mathrm{E}\left(R_i\right)=R_f+ \beta_{i, \mathrm{MKT}} \mathrm{E}\left(R_m-R_f\right)+\beta_{i, \mathrm{SMB}} \mathrm{E}(S M B)+\beta_{i, \mathrm{H} M L} \mathrm{E}(H M L)+\beta_{i, \mathrm{~W} M L} \mathrm{E}(W M L)

Monetary policy and government risk during extraordinary times: for the loser stocks, government bailouts put a floor underneath the prices of these stocks to stop the tendency to keep losing

Behavioral theories of the momentum premium: momentum can be generated in two ways. Delayed overreaction: causes the price to persistently drift upward Underreaction: the price does not go up as much as it should have to fully reflect how good the news actually was. Investors then learn and cause the stock to go up again the next period.

Summaries about dynamic factors

The size, value and momentum strategies are all cross-sectional strategy, meaning that it compares one group of stocks against another group of stocks in the cross section

Momentum strategy: positive feedback strategy. Stocks with high past returns are attractive, momentum investors continue buying them and they continue to go up

Value strategy: negative feedback strategy. Stocks with declining prices eventually fall far enough that they become value stocks

Alpha and Anomaly

Active management

Alpha: average return in excess of a benchmark. Benchmark is passive and can be produced without any particular investment knowledge or even human intervention超过基准的部分

Excess return (active returns): r_t^{e x}=r_t-r_t^{b m k}

Average excess return: \alpha=\frac{1}{\mathrm{~T}} \sum_{t=1}^T r_t^{e x}

Tracking error constraints are imposed to ensure a manager does not stray too far from the benchmark.偏离基准的程度

The larger the tracking error, the more freedom the manager has

Information ratio: the average excess return per unit of risk.承担一单位跟踪风险获得的超额回报

Information ratio(IR): \frac{\text { active return }}{\text { tracking error }}=\frac{\alpha}{\bar{\sigma}}

Special case: when the benchmark is risk-free rate

\begin{align}&\alpha=\overline{r_t-r_{f t}} \\ &\text{ IR }=\text{ Sharpe Ratio }=\frac{\overline{r_t-r_{f t}}}{\sigma}\end{align}

Fundamental law

Grinold fundamental law基本定律: \mathrm{IR} \approx I C \times \sqrt{B R}

Information coefficient(IC)信息系数: the correlation of the manager's forecast with the actual returns预测与真实的相关系数

The breadth of the strategy(BR): how many bets are taken次数

Creating alpha: by making bets that deviate from that benchmark. The key to generating alphais forecasting

How good asset managers at forecasting准确程度

How many bets努力程度

Assumptions of fundamental law: each active return is independent from the other active return forecasts for that period and independent from the forecast for that security in subsequent periods回报是独立的、预测是独立的

Limitations of fundamental law:

ICs are assumed to be constant across BR

Manager whom you find may truly have a high IC, but the one hundredth manager whom you hire probably does not

It is difficult to have truly independent forecasts in BR

The benchmark portfolio holding 27% in the risk-free asset and 73% in the Russell 100

不是直接对index回归

Factor benchmarks

The factor benchmark describes the systematic components of asset i's return

\begin{align}&\mathrm{E}\left(r_i\right)-r_f=\beta_i\left[\mathrm{E}\left(r_m\right)-r_f\right] \\ \text { if } &\beta_i=1.3\rightarrow \mathrm{E}\left(r_i\right)=-0.3r_f+1.3\mathrm{E}\left(r_m\right) \\ &\mathrm{E}\left(r_i\right)=\alpha_{\mathrm{i}}+\underbrace{\left[-0.3r_f+1.3\mathrm{E}\left(r_m\right)\right]}_{\mathrm{E}\left(\mathrm{r}_{\mathrm{bmk}}\right)}\end{align}

The benchmark portfolio holding -30% in the risk-free asset and 130% in the market portfolio

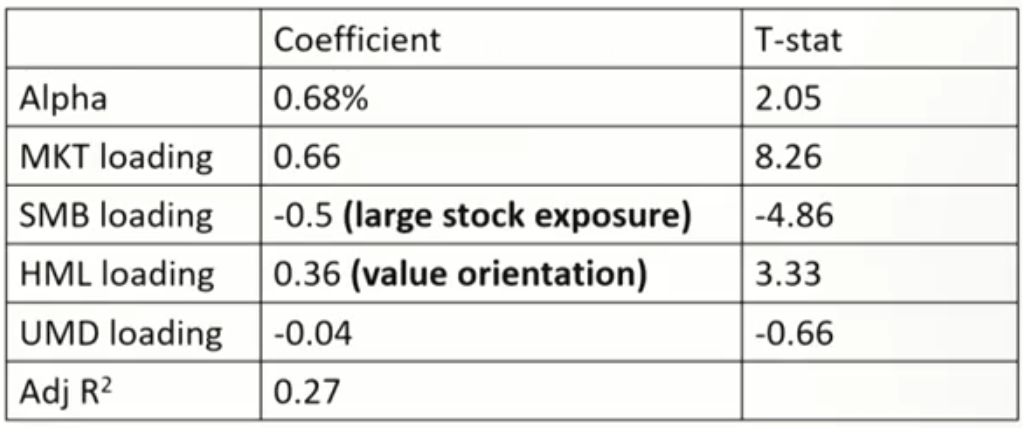

Factor regressions r_{\mathrm{it}}-r_{f t}=\alpha+\beta\left(r_{\mathrm{mt}}-r_{f t}\right)+s\mathrm{SMB}_t+h \mathrm{H M L}_t+u \mathrm{U M D}_t+\varepsilon_{i t}

s = 0 if a stock co-moves neither with small nor large stocks, it's a medium-size stock

s > 0 stock moves together with small stocks

s < 0 stock moves together with large stocks

Statistical significance of alpha: determines whether the alpha reliably indicates ability.

Null (H0):Alpha is zero

Alternative (HA): Alpha is not zero t(\hat{\alpha})=\frac{\hat{\alpha}-0}{\hat{\sigma}(e) / \sqrt{N}}

Time-varying factor: introduced "style analysis" to handle time-varying benchmarks where the factor exposures evolve through time.

Style analysis seeks to rectify two potential shortcomings of factor regression:

The Fama-French portfolios are not tradable

The factor loadings may vary over time.

The collection of index funds that replicate the fund is called the "style weight"

Non-linear payoffs: alphas are computed in a linear framework. There are many nonlinear strategies, especially those involving dynamic option strategies, that can masquerade as alpha.

Why do dynamic, nonlinear strategies yield false measures of alpha?

Buying and selling options changes the distribution of returns

Low-risk anomaly

Traditional financial theory: in CAPM for example, there should be a positive relation between risk and return.传统认为风险越大收益越高

The risk anomaly: stocks with low betas and low volatilities have high returns.

Volatility is negatively related to future returns波动率大收益低

Realized beta is negatively related to future returns低\beta股票未来回报多

Minimum variance portfolios do better than the market最小方差组合比市场组合表现好

Explanation

Leverage constraints杠杆限制: investors wish to take on more risk but are unable to take on more leverage.

Agency problems代理人问题: Institutional managers have constraints

Long only: If a stock has negative alpha, manager needs to short stock and he or she cannot do so. The tracking error constraint also limits the underweight position.做空限制

Preference: Investors have a preference for high-volatility stocks, then they bid up stocks until they have low returns(and vice versa)偏好高风险股票

Portfolio risk management

Portfolio Construction

5 inputs to the portfolio construction process

Current portfolio: near certainty

Alphas: are often unreasonable and subject to hidden biases

Covariances

Active risk aversion: target level of active risk consistent with an active risk aversion

Transactions costs

Refining alphas

Motivation: Most active managers construct portfolios subject to certain constraints, agreed upon with the client. These limits can make the portfolio less efficient, but they are hard to avoid.

Not take short positions.

Limit the amount of cash in the portfolio.

Liquidity.

Alphas can be adjusted so that they are in line with investor or manager's desires for risk control and various constraints

Steps:

Scale the alphas确定取值范围

\begin{gathered}\alpha=\text { volatility } \cdot \text {IC} \cdot \text { Score } \\ \alpha \in[0-z \times\text {IC} \times \text { volatility },0+z \times\text {IC} \times \text { volatility }]\end{gathered}

Score has a mean of zero and standard deviation of one原始分值,映射为标准正态分布

Information coefficient: Correlation between actual and forecasted outcomes.

Trim alpha outliers剔除异常值: very large positive or negative alphas can have undue influence.

Closely examine all stocks with alphas greater in magnitude than three times the scale of the alphas.

Neutralization中性化: If our initial alphas imply an alpha for the benchmark, the neutralization process recenters the alphas to remove the benchmark alpha使基准的\alpha为0 Benchmark-and cash-neutral alphas: Adjusting the benchmark alpha to zero. The optimal position that uses benchmark will have a beta of one. Risk-Factor-neutral alphas: will include only information on the factors the manager can forecast

Specific factor risk: Decomposition of risk allows differing aversions to these different sources of risks拆分成一般风险和特定风险

\text{Utility} =\alpha_p-\left(\lambda_{A, CF} \cdot \sigma_{A, C F}^2+\lambda_{A, S P} \cdot \sigma_{A, S P}^2\right)

Since specific risk arises from bets on specific assets, a high aversion to specific risk reduces bets on any one stock

For managers of multiple portfolios, aversion to specific risk can help reduce dispersion离差

Transaction costs

Transactions costs: are the costs of moving from one portfolio allocation to another.

Rebalancing incurs transactions costs at that point in time. Transaction costs must be amortized over the investment horizon in order to determine the optimal portfolio adjustments.

Revisions and rebalancing: fund manager should make the correct trade-off between expected active return, active risk,and transactions costs.

If the manager is not sure of his or her ability to correctly specify the alphas, the active risk, and the transactions costs, less frequent revision may be a safeguard

The shorter time horizon for forecasting alphas, the larger amounts of noise. Rebalancing for very short horizons would involve frequent reactions to noise, not signal

Revisions and rebalancing M C V A_n=\alpha_n-2\times \lambda_A \times \sigma_\alpha \times M C A R_n

MCVA(Marginal contribution to value added): shows how value added, as measured by risk-adjusted alpha, changes as the holding of the stock is increases.

MCAR(Marginal contribution to active risk): measures the rate at which active risk changes as we add more of stock n The change in value added also depends upon the impact(at the margin) on active risk of adding more of stock n

No trade region \begin{gathered}-S C_n \leq M C V A_n \leq P C_n \\2\times \lambda_A \times \sigma_\alpha \times M C A R_n-S C_n \leq \alpha_n \leq P C_n+2\times \lambda_A \times \sigma_\alpha \times M C A R_n\end{gathered}

Determination of the no-trade region: transactions costs,risk aversion, alpha and the riskiness of the assets.

Portfolio construction techniques

Objective: maximizing active returns minus an active risk penalty \text{Value added}=\alpha_p-\lambda_A \cdot \sigma_\alpha^2- \text{transaction cost}

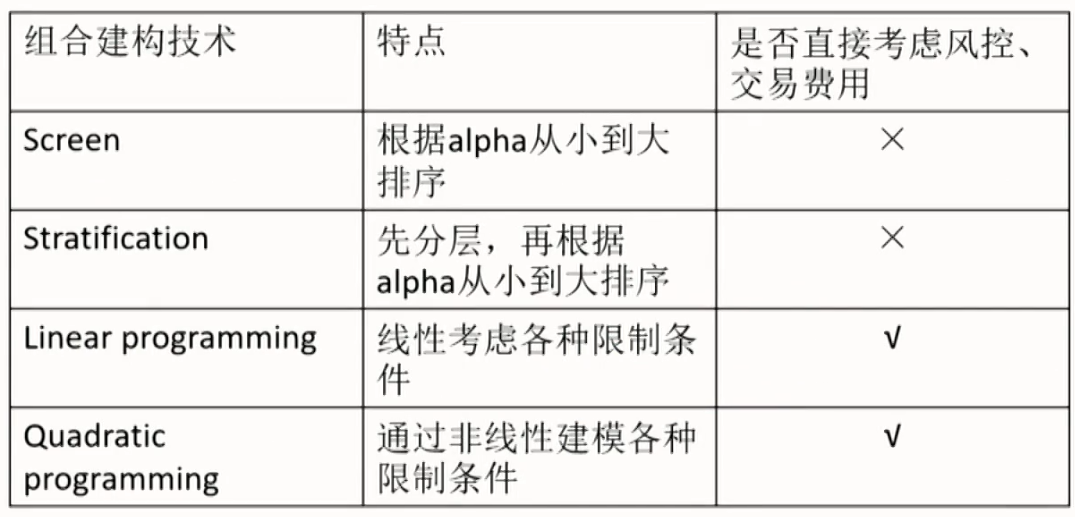

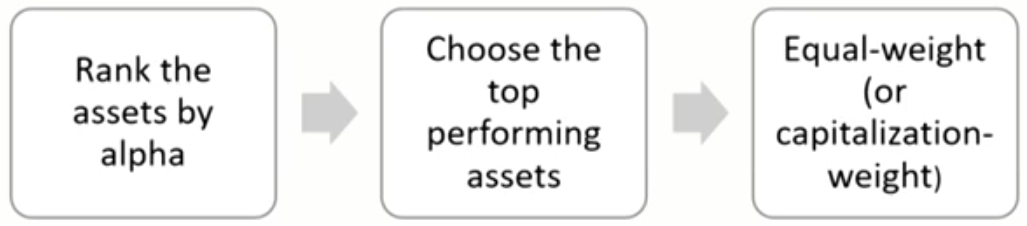

Screen(筛选)

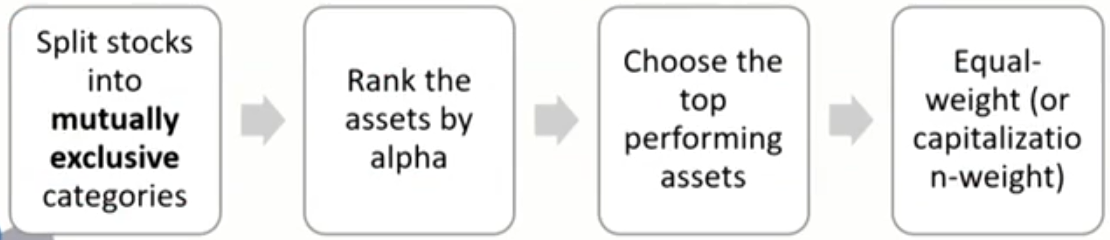

Stratification(分层)

Linear programming(线性规划)

Quadratic programming(二次规划)

Screen

Divide the universe of assets into buy, hold, and sell decisions based on the rankings of alpha直接排序操作

Purchase any assets on the buy list not currently in the portfolio, and sell any assets in the portfolio that are on the sell list

Risk control:

Include a sufficient number of stocks and by weighting them to avoid concentration in any single stock

Transactions costs are limited by controlling turnover

Advantages:

Simple; easy to understand and computerize

Clear link between cause (buy, sell or hold) and effect (portfolio performance)

The screen is robust. It depends solely on ranking so wild estimates of alphas will not alter the result Enhances alphas by concentrating the portfolio in the high-alpha stocks

Disadvantages lgnore all information in the alphas apart from the rankings Excluded assets with lower alphas

Stratification

Split the list of assets into mutually exclusive categories分层,内部排序操作

Risk control: make sure that the portfolio has a representative holding in each category. Chosen well, the categories can lead to reasonable risk control while some important risk dimensions are excluded, risk control will fail.

Linear programming: characterizes assets along dimensions of risk, e.g. industry, size, volatility, and beta (without making the dimensions mutually exclusive)

Objective of linear programming: maximize the portfolio's alpha less transactions costs while remaining close to the benchmark portfolio in the risk control dimensions.

It also includes explicit transactions costs, a limit on turnover,and upper and lower position limits on each asset

Advantages: takes all the information about alpha into account and controls risk by keeping the characteristics of the portfolio close to the characteristics of the benchmark

Disadvantages

Hard to produce portfolios with a prespecified number of stocks.

The risk-control characteristics should not work at cross purposes with the alphas

Quadratic programming: explicitly considers alpha, risk, and transactions costs.

Advantage: Including all the constraints and limitations one finds in a linear program.

Disadvantage: A great many more inputs than the other portfolio construction techniques.More inputs mean more noise.

Causes and Methods for Dispersion

Dispersion: fund managers run separate accounts for multiple clients but the portfolio returns are not identical.

Dispersion is the difference between the maximum return and minimum return for separate account portfolios.

Reasons

Client-driven: constrains from clients

Manager-driven: a lack of attention (separate accounts exhibit different betas and different factor exposures through lack of attention)

If transactions costs were zero, dispersion would disappear,at no cost to investors

Analytical Methods

Portfolio VaR measures

Delta-normal model: all individual security returns are assumed normally distributed.

Traditional portfolio analysis: based on variances and covariances, which is why it is sometimes called the covariance matrix approach.

Individual VaR: The VaR of one component taken in isolation. V a R_i=z \times \sigma_i \times\left|V_i\right|=z \times \sigma_i \times\left|w_i\right| \times V_p

z = the z-score associated with the level of confidence(95%:1.645;99%: 2.326)

V = the market value of the individual asset or portfolio

σ= the standard deviation of the individual asset return or portfolio return

w = the proportion or weight in the position

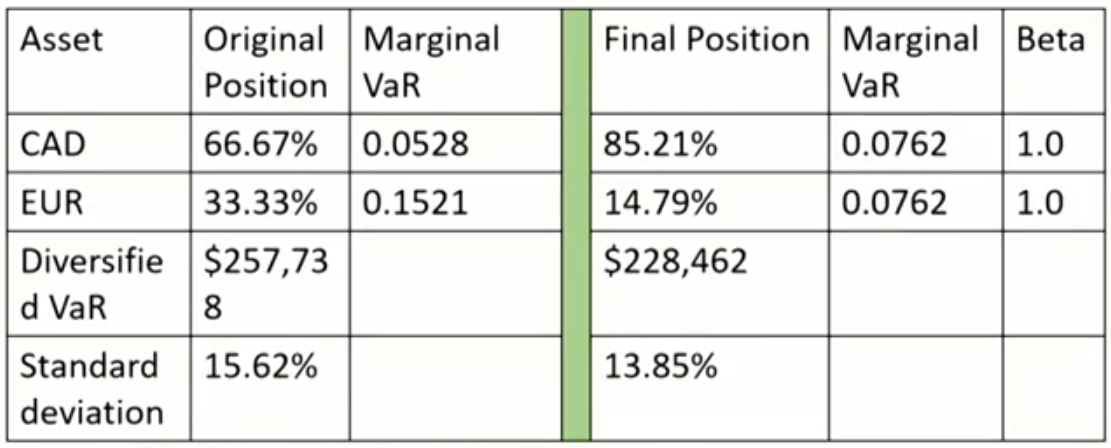

Diversified VaR: takes into account diversification benefits between components z \cdot \sigma_p \cdot V_p

Variance for portfolio of two assets: \sigma_p^2=w_1^2\sigma_1^2+w_2^2\sigma_2^2+2w_1w_2\sigma_1\sigma_2\rho_{12}

Uncorrelated(\rho is zero): V a R_p=\sqrt{V a R_1^2+V a R_2^2}

Perfectly correlated(\rho is one): V a R_p=V a R_1+V a R_2

Undiversified VaR: is the sum of individual VaRs.

Undiversified VaR ≥ Diversified VaR

Diversification benefit: the difference between the diversified VaR and the undiversified VaR which typically is shown in VaR reporting systems. \sigma_p=\sigma \sqrt{\frac{1}{N}+\left(1-\frac{1}{N}\right) \rho}

All assets have the same risk.

All correlations are the same.

Equal weight is put on each asset.

VaR tools

Marginal VaR(MVaR):the change in portfolio VaR resulting from taking an additional dollar of exposure to a given component.对单个资产增量的VaR M V a R_i=\frac{\partial V a R}{\partial(\text { investment })}=z \frac{\partial \sigma_p}{\partial w_i} =z \frac{\operatorname{cov}\left(R_i, R_p\right)}{\sigma_p}=z \cdot \sigma_i \cdot \rho_{i p}=z \cdot \beta_i \cdot \sigma_p=\frac{V a R_p \cdot \beta_i}{V_p}

Incremental VaR: is the change in VaR owing to a new position引入新投资组合增加的VaR \text{Full Incremental VaR}=V a R_{p+a}-V a R_p

The main drawback of this approach is that it requires a full revaluation of the portfolio VaR with the new trade(quite time-consuming for large portfolios)难计算

Incremental VaR估算\approx M V a R_i \cdot V_i

Component VaR(CVaR): A partition of the portfolio VaR that indicates how much the portfolio VaR would change approximately if the given component was deleted每个资产对组合VaR的贡献 C V a R_i=M V a R_i \times V_i =M V a R_i \times w_i \times V_p=V a R_p \times \beta_i \times w_i

Percentage contribution (%) to VaR of component: \begin{gathered}i=\frac{C V a R_i}{\operatorname{VaR}_p}=w_i \beta_i \\ C V a R_1+\operatorname{CVaR}_2+\cdots+C V a R n=\operatorname{VaR}_p\left(\sum_{i=1}^n w_i \beta_i\right)=\operatorname{VaR}_p\end{gathered}

Risk management

Only taking risk into consideration → global minimum A manager can lower a portfolio VaR by:

Lowering position with the highest marginal VaR

Adding position with the lowest marginal VaR

When the portfolio risk has reached a global minimum:

All MVaR must be equal.

All betas must be equal.

Taking return and risk into consideration → optimal portfolio Maximize the Sharpe ratio with VaR of the portfolio:

Maximize the Sharpe ratio with VaR of the portfolio: \frac{\overline{R_p}-\overline{R_f}}{V a R_p}

Lowering allocation to the position with the lowest excess expected return to marginal VaR.

Adding allocation to the position with the highest excess expected return to marginal VaR. \frac{R_i-R_f}{M V a R_i}

When the has reached a minimum:

All the ratios of \frac{R_i-R_f}{M V a R_i} must be equal.

All the ratios of \frac{R_i-R_f}{\beta_i} must be equal.

VaR and Risk Budgeting

Types of risks

Absolute risk vs. Relative risk

Investment asset managers can have different perceptions of risk.

Absolute risk: is the risk of a dollar loss over the horizon

Relative risk: is the risk of a dollar loss in a fund relative to its benchmark.

If the excess return of the asset over the benchmark is normally distributed, VaR can be measured from the relative perspective: V a R_{\text {relative }}=z \cdot \sigma_\alpha \cdot V

Policy-mix risk: is the risk of a dollar loss owing to the policy mix selected by the fund. The risk from passive funds investment, this risk represents that of a passive strategy

Active-management risk: is the risk of a dollar loss owing to the total deviations from the policy mix

Most of the risk is due to the policy mix.

The active-management VaR is rather small.

The policy-mix VaR and active-management VaR do not add up to the total-asset VaR

Funding risk

A pension fund with defined benefits promises a stream of fixed payments to retires. If the assets are not sufficient to cover these liabilities, the shortfall will have to be made up by the fund's owner (provide additional contributions to the fund).

Risk should be viewed in an asset liability management(ALM) framework Funding risk: the value of assets will not be sufficient to cover the liabilities of the fund

Surplus: is the difference between the value of the assets and the liabilities.

If liabilities consist mainly of nominal payments, their value will behave like a short position in a long-term bond

\begin{aligned}

Surplus& = Assets - Liabilities\\

\Delta Surplus &=\Delta Assets -\Delta Liabilities =A \cdot R_A-L \cdot R_L\\

R_{\text {surplus }}&=\frac{\Delta \text { Surplus }}{\text { Asset }} =\frac{\Delta \text { Asset }}{\text { Asset }}-\frac{\Delta \text { Liabilities }}{\text { Liabilities }} \times \frac{\text { Liabilities }}{\text { Asset }} \\

& =R_{\text {asset }}-R_{\text {libility }} \frac{L}{A}

\end{aligned}

Surplus at risk (SaR)面临的向下变化量,单尾 \begin{gathered}\sigma_{\text {surplus }}=\sqrt{A^2\cdot \sigma_A^2+L^2\cdot \sigma_L^2-2\cdot A L \sigma_A \sigma_L \rho}\quad (\text { dollar term }) \\ \operatorname{SaR}=\mid E(\Delta \text { Surplus })-z c \sigma_{\text {surplus }} \mid\end{gathered}

The confidence interval for expected end-of-year surplus双尾 \begin{gathered}{\left[E\left(\text { Surplus }_1\right)-z \sigma_s, E\left(\text { Surplus }_1\right)+z \sigma_s\right]} \\ E\left(\text { Surplus }_1\right)=\text { Surplus }_0+E(\Delta \text { surplus })\end{gathered}

Sponsor risk: surplus risk can be extended to the risk to the owner of the fund who ultimately bear responsibility for the pension fund. Economic risk: is the variation in the total economic earnings of the plan sponsor. (if the firm enjoys greater operating profits, the surplus risk may be less of a concern.) Cash-flow risk: is the risk of year-to-year fluctuations in contributions to the pension fund.不确定要拿多少钱补养老金导致现金流不确定

VaR applications to investment management

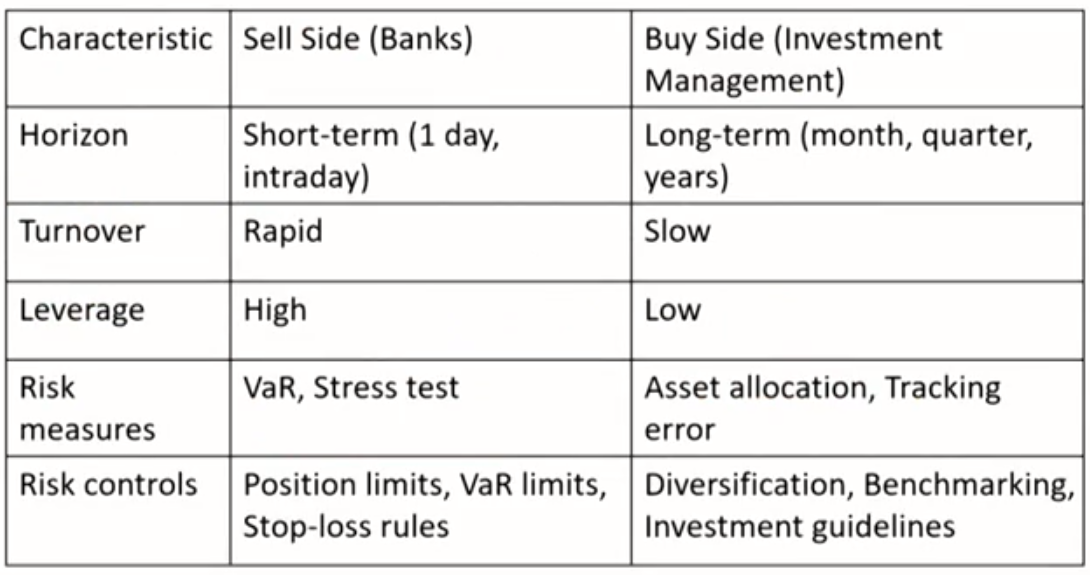

Sell side versus buy side:

Investment process of large investors (e.g. pension funds)

Step One: strategic, long-term asset-allocation study

Based on mean-variance portfolio optimization

Determines the amounts to be invested in various asset classes

Step Two: delegate fund managers

Conduct performance evaluation periodically relative to their benchmark

Investment guidelines and some additional restrictions: duration, maximum deviations from equity-sector weights, maximum amounts of foreign currency to hedge, etc.

Institutions exposed to a diversity of risk, to complex financial instruments, and to changing positions should benefit from VaR risk management systems.

Take diversification into account.

A need for stronger, centralized risk management systems (Financial instruments are becoming more complex).

Most investment portfolios are dynamic.

Hedge fund: poses special risk measurement problems.

High leverage

Lack of transparency

Heterogeneous

Some groups have greater turnover than traditional investment managers → risk management systems similar to the bank

Check compliance

Unauthorized investment: some securities may be prohibited because of their risks or for other reasons (e.g.,political or religious). But some fund managers sometimes trade in and out of unauthorized investment before the client realized what happened.

Monitor risk

Fund managers and investors would notice a sudden jump in the reported VaR of the fund.The reason may be:

A manager taking more risk.

Different managers taking similar bets.

More volatile markets.

VaR can be reverse engineered to understand where risk is coming from using VaR tools(e.g., component VaR, marginal VaR).

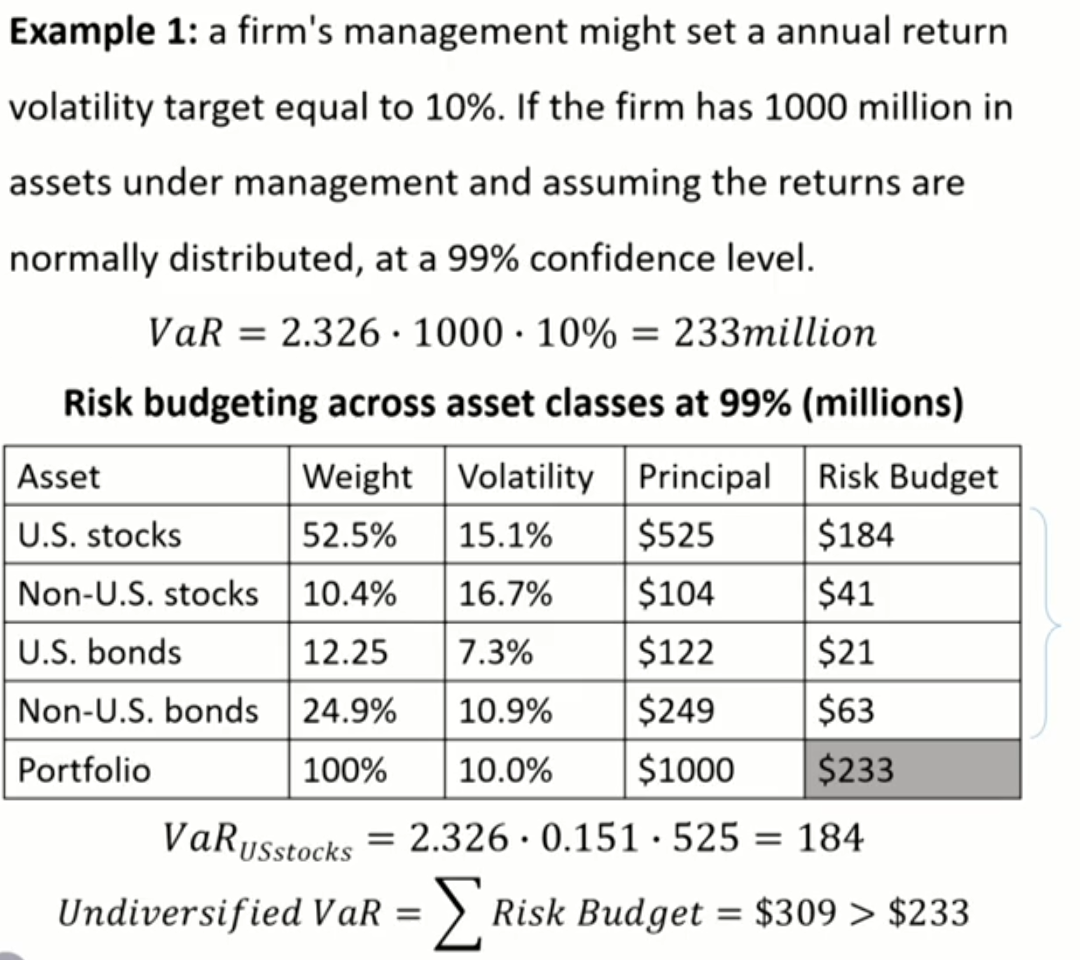

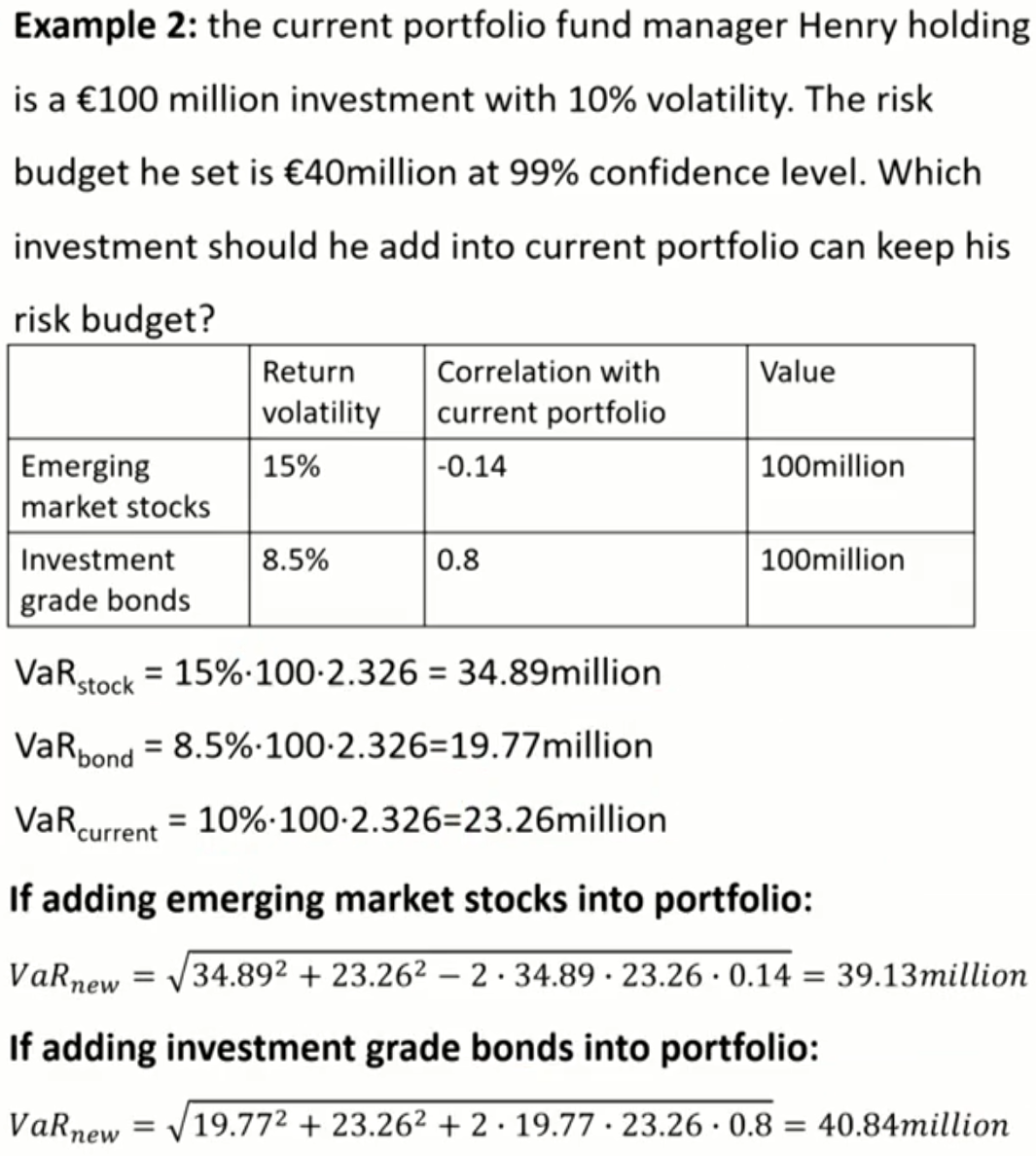

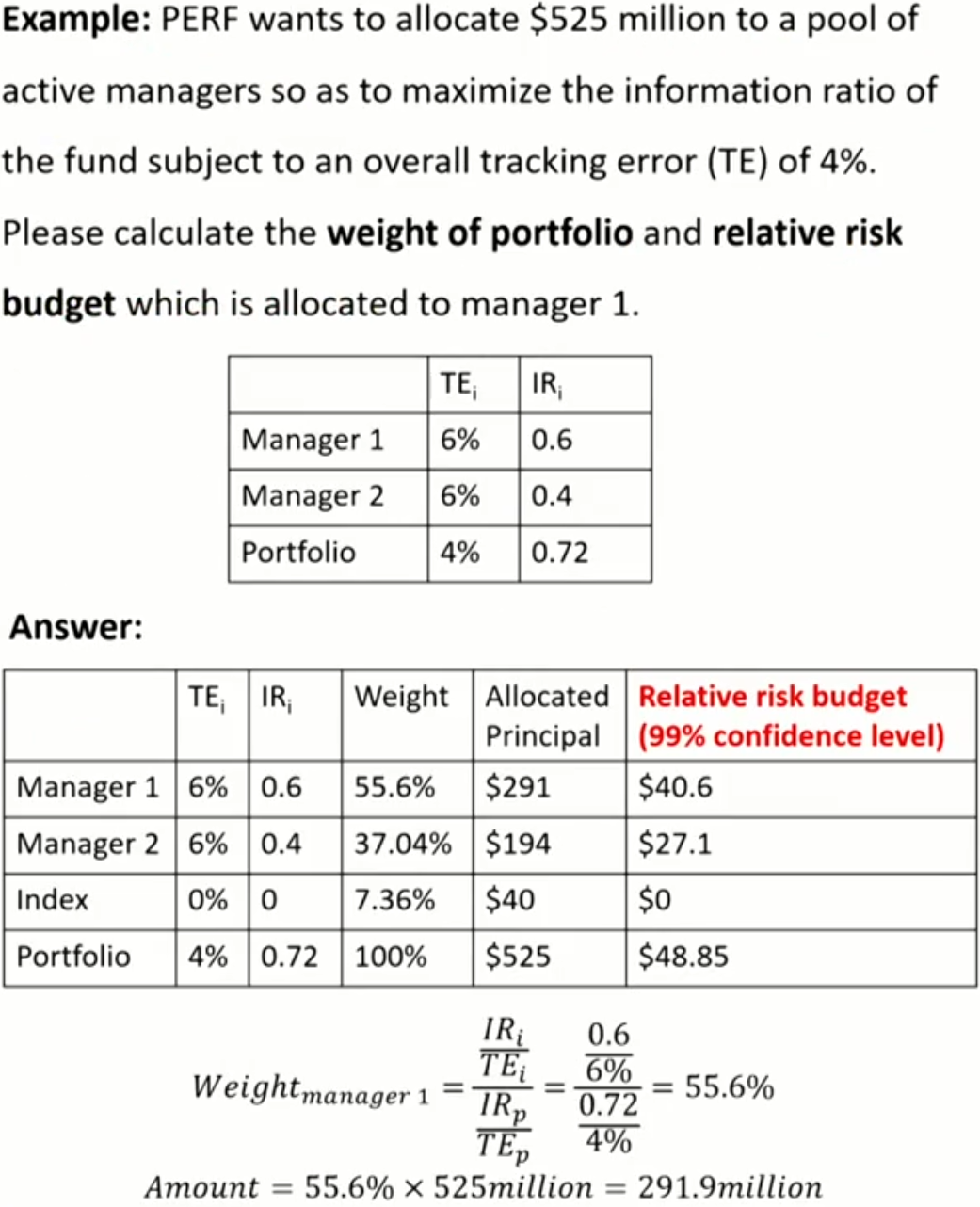

Risk budgeting

Risk budgeting: the process of decomposing the aggregate risk of a portfolio into its constituents, using these risk measures to allocate assets, setting limits in terms of these measures, and then using the limits to monitor the asset allocations and portfolio managers

across asset classes

across active managers给基金经理分配资金的权重

A greater risk budget should be allocated to managers with better performance, as measured by the IR criterion

Weight of portfolio managed by manager i: w_i=\frac{\frac{I R_i}{T E_i}}{\frac{I R_p}{T E_p}}=\frac{\frac{\alpha_i}{T E_i^2}}{\frac{\alpha_p}{T E_p^2}}

Assume that the deviations for each manager are independent of each other

TE: track error

The residual weight is allocated to the index.未分配的权重给基准

Risk Monitoring

VaR vs. Tracking error

VaR: the maximum dollar loss associated with a given level of statistical confidence over a given period of time.

To achieve targeted levels of dollar VaR, owners of capital allocate capital among asset classes.

Tracking error: gauges the risk profile relative to a benchmark (standard deviation of excess returns).

Tracking error is used to describe the extent to which the investment manager is allowed latitude to differ from the index.

Three-legged risk management tool

Risk plan

Set expected return and expected volatility(e.g., VaR and tracking error)

Define the bright line between those events that are merely disappointing and those that inflict serious damage

Paint a vision of how risk capital will be deployed to meet the organization's objectives.

The risk plan should identify critical dependencies that exist inside and outside the organization.

Risk budget

The risk budget should quantify the vision of the risk plan

Using mean-variance optimization to determine appropriate weights for each class(expected returns, risks,and covariances, organization's strategic objectives and risk tolerances).

Ensure ROE and RORC must exceed some minimum levels.

Simulate the performance of a portfolio(e.g. downside scenarios)

Risk monitoring

Risk capital is a scarce commodity, so monitoring controls should exist to ensure that risk capital is used in a manner consistent with the risk budget

Risk monitoring is required to ensure that material deviations from risk budget are detected and addressed in a timely fashion.

Risk management units(RMUs)

RMUS:

Role: oversee the risk exposures of portfolios and ensure that such exposures are authorized and in line with risk budgets.

Must be established independently from the business areas and operate as a controlling or monitoring function

have an independent reporting line to senior management.

Gathers, monitors, analyzes, and distributes risk data to managers, clients, and senior management in order to better understand and control risk.

Should not manage risk, but rather measure risk.

Watches trends in risk as they occur and identifies unusual events to management in a timely fashion.

Identifies and develops risk measurement and performance attribution analytical tools

Provides tools for both senior management and individual portfolio management to better understand risk in individual portfolios and the source of performance.

Helps ensure that transactions are authorized in accordance with management direction and client expectations.

Liquidity Considerations

Liquidity duration买资产不影响价格需要的间隔时间: the number of days required to liquidate any given security. L D_i=\frac{Q_i}{0.15\cdot V_i}

LD: liquidity duration statistic for security

15%: we do not wish to exceed 15% of the daily volume in that security to avoid a material adverse earning impact.

Q: number of shares held in security

V: daily volume of the security

Portfolio Evaluation

Return calculation

Time-weighted returns: The compound return that $1 initially invested in the portfolio over a stated measurement period. \begin{gathered}\left(1+R_G\right)^n=\left(1+R_1\right)\left(1+R_2\right)\left(1+R_3\right) \ldots\left(1+R_n\right) \\1+R_G=\left[\left(1+R_1\right)\left(1+R_2\right)\left(1+R_3\right) \ldots\left(1+R_n\right)\right]^{1/ n}\end{gathered}

Each return has an equal weight in the geometric average The geometric average is referred to as a time-weighted average.

Dollar-weighted returns: accounts for the timing and amount of all cash flows into and out of the portfolio. C F_0+\frac{C F_1}{1+D W R}+\cdots+\frac{C F_n}{(1+D W R)^n}=0

Compare

DWR(If more funds to invest):

Before favorable time: the dollar-weighted rate of return will tend to be elevated (higher/increased).

Before unfavorable time: the dollar-weighted rate of return will tend to be depressed (lower/decreased)

TWR: The use of the time-weighted return removes distortions of fund investing, providing a better measure of a manager's ability to select investments over the period.

Risk-adjusted performance measures

Sharpe ratio: divides average portfolio excess return over the sample period by the standard deviation of returns (total risk) over that period. \text{Sharpe Ratio} =\frac{\overline{R_p}-\overline{R_f}}{\sigma_p}

Treynor ratio: like the Sharpe ratio, Treynor's measure gives excess return per unit of risk, but it uses systematic risk instead of total risk. \text{Treynor Ratio}=\frac{\overline{R_p}-\overline{R_f}}{\beta_p}

Sharpe ratio vs. Treynor ratio:

Well-diversified portfolio: performance evaluation using Sharpe ratio and Treynor ratio will give the same ranking result.

Not well-diversified portfolio: it may be ranked relatively higher using Treynor ratio than using Sharpe ratio.

Jensen's alpha: is the average return on the portfolio over and above that predicted by the CAPM, given the portfolio's beta and the average market return. \alpha_p=\overline{r_p}-\left[\overline{r_f}+\beta_p\left(\overline{r_m}-\overline{r_f}\right)\right]

Information ratio: measures excess return over benchmark per unit of risk. I R=\frac{\alpha_p}{\sigma\left(\alpha_p\right)}

A higher information ratio indicates better performance.

Modigliani-squared measure(M2): we adjust the return of portfolio to the same standard deviation as the index.Because the market index and portfolio have the same standard deviation, we can compare their performance simply by comparing returns. M^2=\frac{\sigma_m}{\sigma_p}\left(R_p-R_f\right)-\left(R_m-R_f\right)

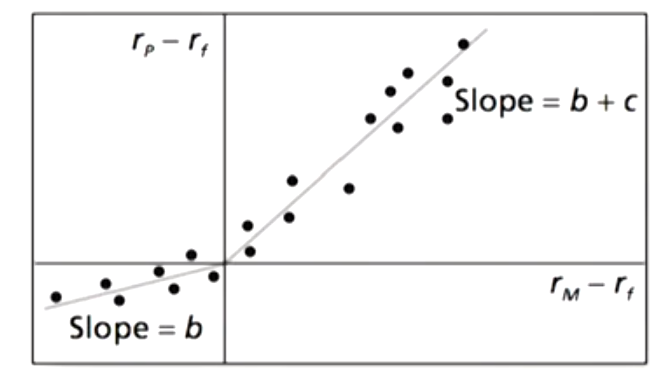

Market timing

Market timing involves shifting funds between a market-index portfolio and a safe asset depending on whether the market index is expected to outperform the safe asset.

Assume fund manager holds only the market-index portfolio and T-bills.

No market timing (the weight of the market are constant) R_p-R_f=a+b\left(R_m-R_f\right)+e_p

With market timing (Treynor and Mazuy) R_p-R_f=a+b\left(R_m-R_f\right)+c\left(R_m-R_f\right)^2+e_p

With market timing (Henriksson and Merton) R_p-R_f=a+b\left(R_m-R_f\right)+c\left(R_m-R_f\right) D+e_p

D is a dummy variable with O for bear markets(RM < Rf)and 1for bull markets(RM > Rf).

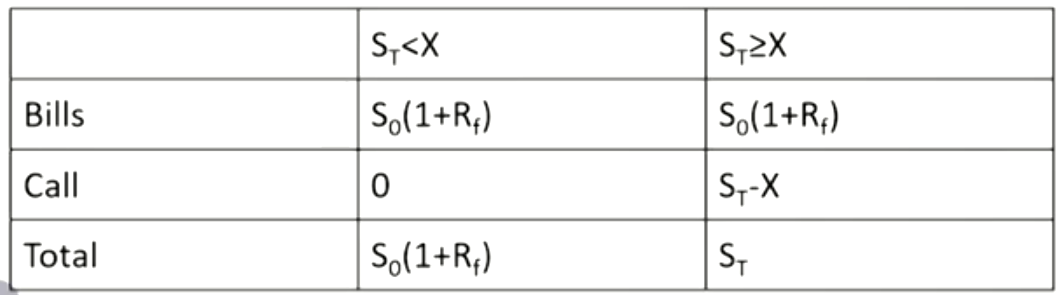

Call option model

The perfect foresight is equivalent to holding a call option on the equity portfolio. The rate of return is at least the risk-free rate.

Suppose that the market index currently is at S_0 and that a call option on the index has an exercise price of X=S_0(1+R_f).

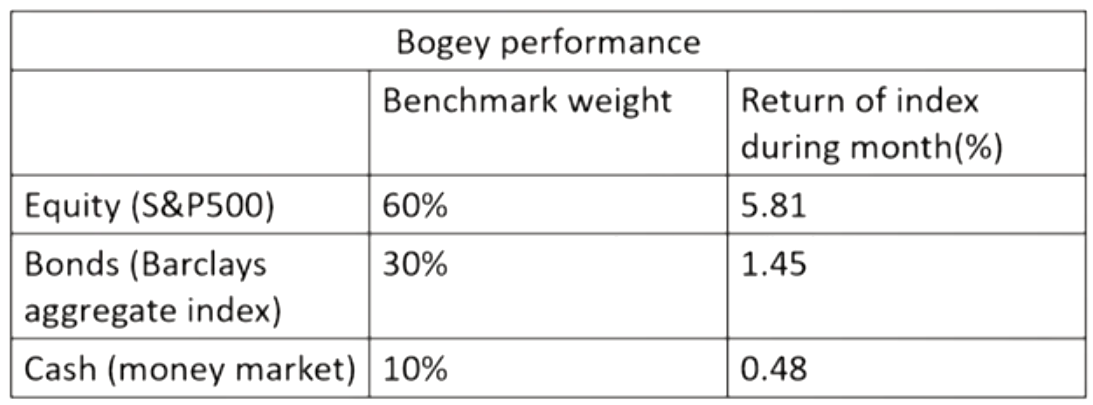

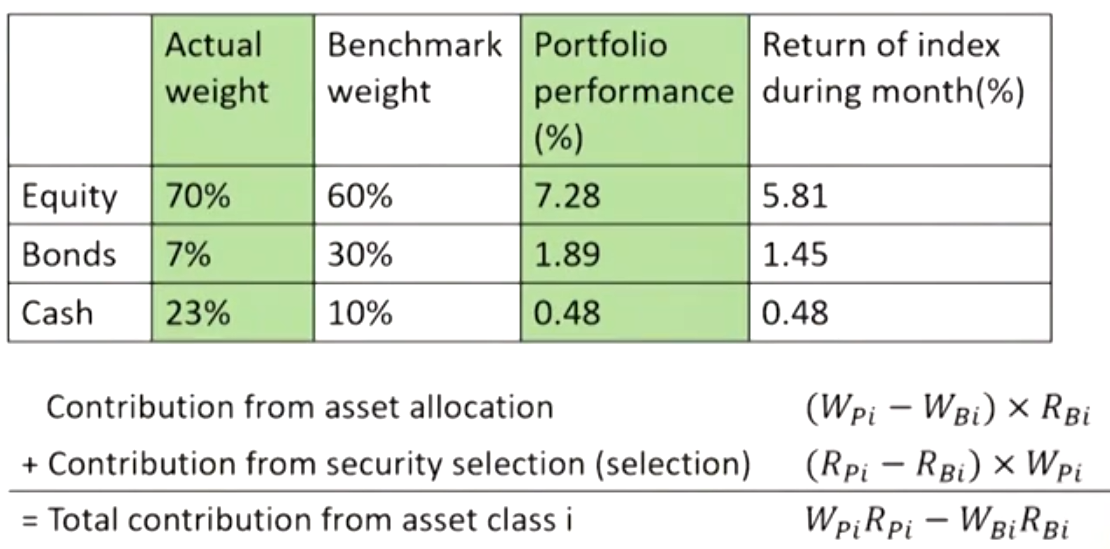

Performance attribution

Example: The portfolio return over the month is 5.34%

Asset allocation: Broad asset market allocation choices across equity, fixed-income, and money markets.

Selection:

Industry (sector) choice within each market.

Security choice within each sector.

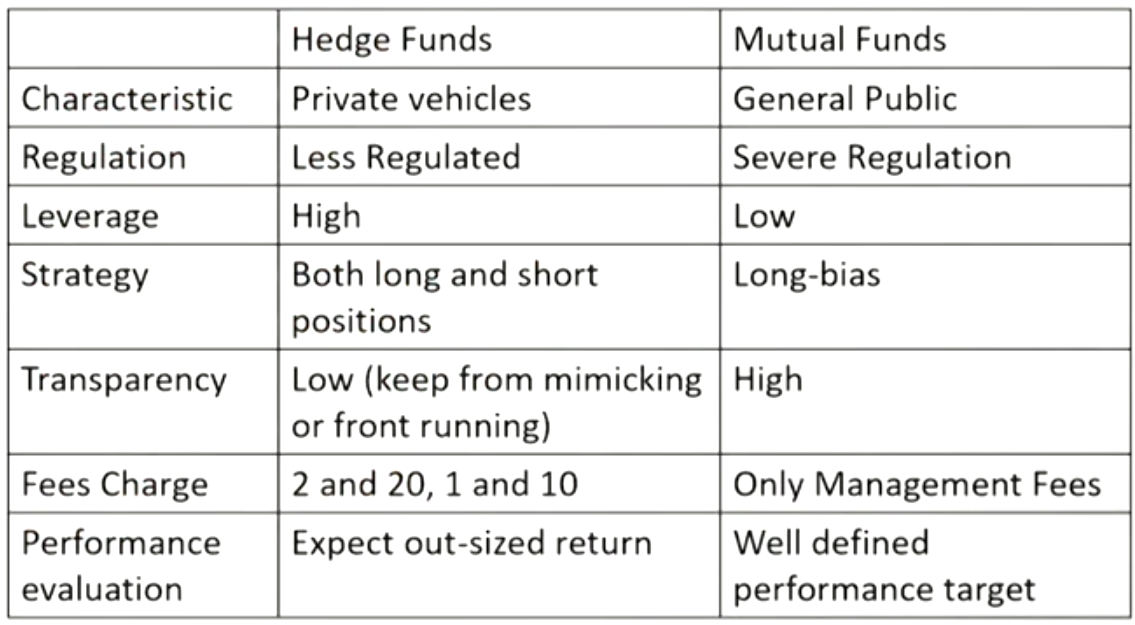

Hedge Funds

Hedge Funds

Characteristics of hedge funds

Databases of hedge funds

Self-Selection bias (selection bias): Manager who have funds with an unimpressive track record will not wish to have that information exposed. In other words, there may well be a tendency to "put the best face forward".只展示好的导致表现好

Backfill bias: When a new fund replaces a deleted fund in an index, the past performance of the new fund is inserted.只加入好的导致表现好

Issues from illiquid assets and the solutions

Correlation with other asset classes will be lowered (appearance of low systematic risk)对冲基金收益率被高估

Using regression with additional lags of the market factors and summing the coefficient across lags.加入滞后项回归

Volatility will be lowered (low total risk)对冲基金风险被低估

Taking autocorrelation into account when extrapolating risk to longer horizons.考虑自相关系数

Directional hedge fund styles趋势跟踪

Managed futures (CTAs, commodity trading advisors): focus on investing in listed bond, equity, commodity futures, and currency markets, globally.

Systematic trading programs are employed. Managed futures fund managers rely upon historical price data and market trends.

A significant amount of leverage is often employed since the strategy involves the use of futures contracts.

Global macro:

Focuses on identifying extreme price valuations and leverage is often applied on the anticipated price movements in equity, currency, interest rate and commodity markets.

employs a top-down global approach to concentrated on forecasting how political trends and global macroeconomic events affect the valuation of financial instruments.

Profits can be made by correctly anticipating price movements in global markets and having the flexibility to use a broad investment mandate, with the ability to hold positions in practically any market with any instrument.

Similarity between global macro and managed futures

these managers behave like asset allocators taking bets in different markets utilizing a range of strategies opportunistically.

Event-driven styles:

Merger arbitrage: attempts to capture the spreads in merger or acquisition transactions involving public companies after the terms of the transaction have been announced.

In a fixed exchange ratio stock merger, one would go long one and short another one according to the merger ratio,in order to isolate the spread and hedge out market risk.

Distressed securities: This strategy invests across the capital structure of companies subject to financial or operational distress or bankruptcy proceedings. Such securities often trade at discount to intrinsic value due to difficulties in assessing their proper value, lack of research coverage, or an inability of traditional investors to continue holding them.

This strategy is generally long-biased in nature.

Distressed managers typically attempt to profit on the issuer's ability to improve its operation or the success of the bankruptcy process that ultimately leads to an exit strategy.

The main feature of this investment strategy is long exposure to credit risk of corporations with very low credit ratings.

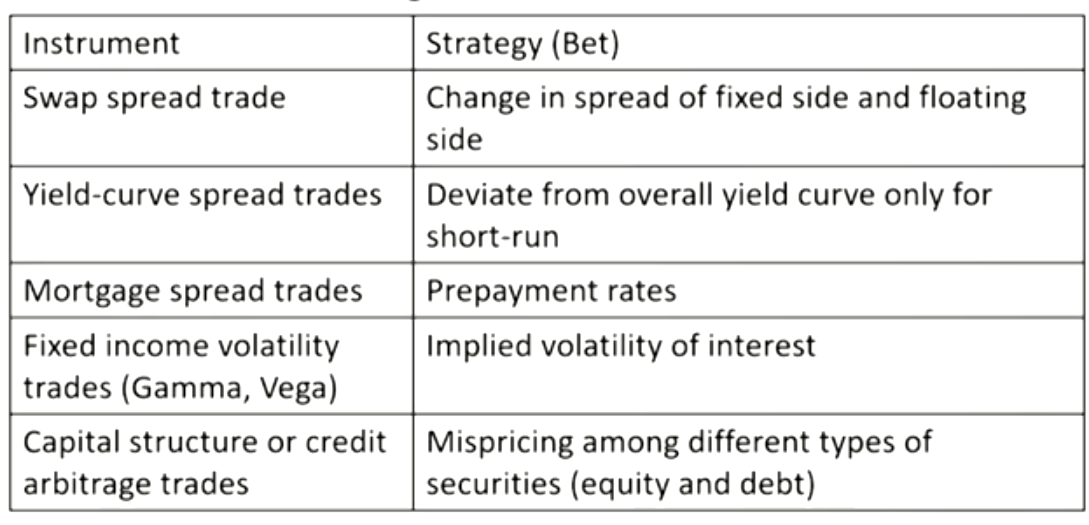

Relative value and arbitrage-like strategies

Fixed income arbitrage: attempts to generate profits by exploiting inefficiencies and price anomalies between related fixed income securities.

Strategies may include leveraging long and short positions in similar fixed income securities that are related either mathematically or economically.

Convertible arbitrage: aims to profit from the purchase of convertible securities and the subsequent shorting of the corresponding stock when there is a pricing error.

The number of shares shorted is based on a delta neutral or market neutral ratio. As a result, under normal market conditions, the arbitrageur generally expects the combined position to be insensitive to fluctuations in the price of the underlying stock.

Pricing anomaly

Gamma/vega trading

Long/short equity: invests in both long and short sides of equity markets, generally focusing on diversifying or hedging across particular sectors, regions or market capitalizations.

Managers typically have the flexibility to shift from value to growth; small to medium to large capitalization stocks; and net long to net short.

30-40% of hedge funds are long/short.

Niche strategies:

Dedicated short: takes more short positions than long positions and earn returns by maintaining net short exposure in long and short equities.

The returns are negatively correlated to equities.

Emerging markets: invests in currencies, debt, equities,and other instruments of countries with emerging or developing markets.

The markets are typically measured by GDP per capita.Such countries are considered to be in a transitional phase between developing and developed status.

Equity market neutral strategy: there is no single common risk factor that drives the return behavior of equity market neutral funds. Return behavior suggests that different funds apply different trading strategies with a similar goal of achieving almost zero beta(s) against a broad set of equity indices.

Hedge fund performance

In practice, evaluating hedge funds poses considerable practical challenges:

The risk profile of hedge funds may change rapidly

Take time-varying bets on different risk factors and the risk profile is nonlinear and responsive to changing equity market conditions.

Considerable ability to manipulate conventional performance measures.

Expose the fund to infrequent but severe losses.

Hedge funds tend to invest in illiquid assets.

When hedge funds are evaluated as a group, survivorship bias can be a major consideration, because turnover关门率 in this industry is higher than for investment companies such as mutual funds.

Convergence of risk factors

An important feature that attracts investors to the hedge fund industry is the variety of strategies hedge fund managers deploy and the diversity of assets to which these strategies are applied.

However, during times of stress, portfolio diversification implodes, and seemingly diverse hedge fund portfolios converge in terms of risk factors.

The risk behind cannot be easily mitigated by simply spreading one's capital to different hedge fund strategies.

The need to consider hedging a tail risk event in a hedge fund portfolio is clear.

The risk management of hedge fund portfolios must take into consideration nonlinear risks such as rare but dramatic market events the manifestation of which can take place on either the asset side and/or the liability side of a hedge fund's balance sheet.

Agency problem

There is a concern about the asymmetry in risk sharing between principal and agent inherent in variable compensation schemes of which hedge fund style incentive fees is one such variation.

The problem arises when the incentive fee which hedge fund managers are entitled to, typically at 15-20% of new profits,ends up enticing a fund manager to take unreasonable bets.

If fund has a negative return, managers still obtain management fee.

How to reduce asymmetric risk:

High water mark.

Lower incentive fees for fund managers.

High fund closure costs.

Force a fund manager to invest in any fund that he manages.

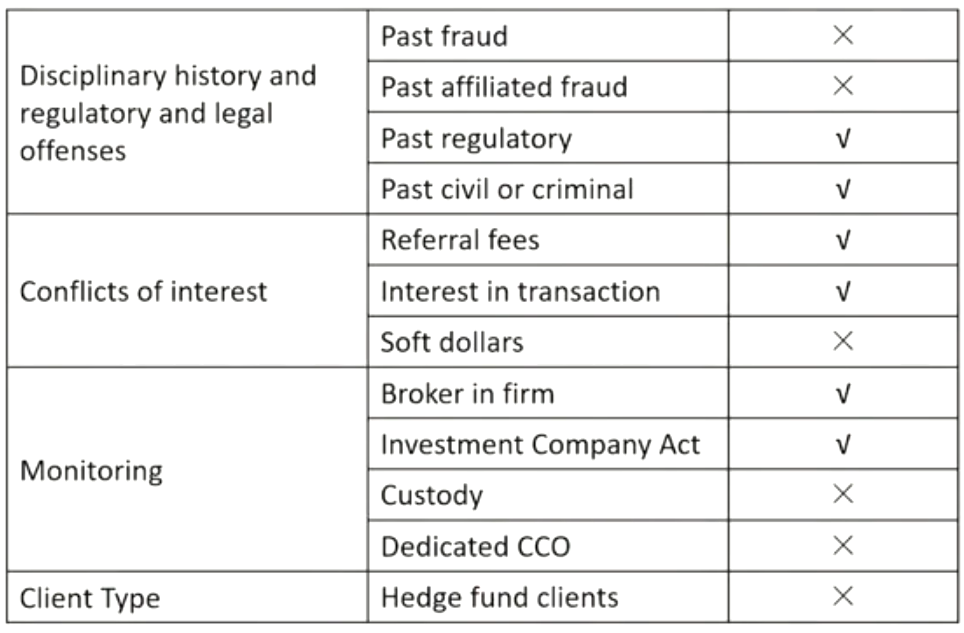

Performing Due Diligence on Specific Managers and Funds

Due diligence basics

Due diligence is the term used to describe the process of evaluation and analysis that an investor follows to get comfortable with a strategy, manager, and a fund prior to making an investment.

Reasons for failures of funds in the past

Bad investment decisions: funds can make several compounded bad decisions or just a few concentrated calls on the markets or individual securities that perform very poorly

Fraud: accounting frauds, valuation frauds, or misappropriation of funds.

Extreme events: excessive leverage, improbable probabilities,unexpected events and tail risk.

Lack of liquidity:

A flood of unanticipated withdrawals of capital at the least opportune time.

Squeeze.

When liquidity dries up, funds cannot meet redemptions

Poor controls: a lack of supervision or compliance controls related to insider trading.

Elements of the due diligence process

Today, both managers and investors spend a great deal of time trying to learn where a manger's "edge" is coming from and that their investment is safeguarded and properly valued.

The goal is to find out what is really going on at the fund and not just have a pitch book recitation by the investor relations staff.

Investment management

Strategy:

Manager's self-described style

Concentrated positions

Turnover and number of days to liquidate

Stop losses

Short sales used

OTCderivatives

Central trading desk

Generate returns for existing investors or grow AUM?

Equity ownership: some firms do not share equity ownership among the portfolio managers or traders in the firm; other firms use equity ownership as a key feature of their professional talent retention program and to attract and groom new talent for future leadership position.

Track record reliable

Whether the track record is comparable to similar strategies

Managers:

Newer managers: ask former colleagues, partners,managers, clients, or other independent parties.

Established managers: motivation, behavior during crisis or stress periods; ability to communicate to investor.

Potential risks that a strategy will be exposed and additional idiosyncratic risks

Inputs and assumptions used in the firm's risk models

Written policies and procedures to monitor and measure each of the applicable risk

Security valuation

Portfolio leverage and liquidity

Tail risk exposure (Return distribution, skewness or kurtosis.)Risk reports (Review and revise on a regular basis)

Consistency of the fund terms with the investment strategy.

Operational environment

Internal control assessment

Qualifications of people at the fund

The quality of the written policies and procedures

The ability of the team to execute, fund's exposure to derivative counterparties

The protections provided by its governance structure

In-house compliance or outsourced relationship with a compliance service provider

Documents and disclosure

An investor needs to verify with the listed law firm in the fund documents that they were responsible for the original content and for any updates.

Fund offering memo, subscription agreement, limited partnership agreement, investment management agreement, Form ADV and website are all saying the same thing at the same point in time.

Either insufficient or extremely broad risk disclosure

Check the equity section to see if the general partner is continuing to invest in the fund

Service provider evaluation

Business model risk and fraud risk

Business model risk: deals with the risks encompassed in simply running the business of being a hedge fund.

Adequate cash on hand.

Where does the working capital come from.

Succession plan (key person insurance).

What happens if too many investors redeem at the same time.

Break-even AUM.

Business model risk and fraud risk

Fraud risk

Potential indicators:

Lack of trading independence

Investor complaints about lack of liquidity.

Litigation in civil court alleging fraudulent acts.

Personal trading by managers

Aggressive shorting and organized efforts to spread rumors.

A high percentage of illiquid investment

Finding Bernie Madoff: Detecting Fraud by Investment Managers

Fraud by investment managers

Ponzi scheme: on December 11, 2008, the securities and exchange commission (SEC) charged Bernard Madoff with securities fraud for committing an $18 billion Ponzi scheme.

The opportunities advisers have to exploit investors.

The importance of limiting advisers' opportunistic behavior through either market or regulatory forces.

In the U.S., the regulatory system protects investors primarily through mandatory disclosure.

Fraud: fraud cases harm the firm's investment clients.

Not include insider trading, short sale violations, brokerage fraud, or other crimes, unless they cause direct losses to the firm's investment clients.

Information disclosure

Form ADV:

the Investment Advisers Act: expressly defines and prohibits investment adviser fraud, requires all advisers with more than $25 million in assets under management (AUM) and with 15 or more U.S. client to register with the SEC

Investment advisers: any entity that receives compensation for managing securities portfolios or providing advice regarding individual securities. Firms: all mutual funds, nearly all institutional investment funds, and many hedge funds in the U.S.

Registered investment advisers: must file Form ADV to disclose past regulatory violations and potential conflicts of interest

An investor who avoided the 5% bf firms with the highest ex ante predicted fraud risk would avoid 29% of fraud cases and over 40% of the dollar losses from fraud

Although to obtain these benefits, the investor would have to forgo investing with 5% of non-fraudulent advisers.

Predicting fraud

Compensated for fraud risk

Are investors compensated for fraud risk?

High fraud risk may provide off-setting benefits that improve investment performance.

Results: do not provide evidence that investors receive compensation for fraud risk.

Barriers and costs

The lack of compensation for fraud risk does not necessarily imply that investors are irrational.

Investors could be compensated in some other unmeasured fashion.

Investors may predict fraud risk based on reputations,personal contacts,or other information

Barriers to accessing Form ADV outweigh the benefits.

For most investors, the cost of individually downloading thousands of Form ADV filings may well have exceeded the perceived benefits.

To implement a fraud prediction model, an investor would have had to collect manually a large number of Form ADV filings, convert the filings into a database, and estimate a prediction model.

Improving ways

Allowing public access to historical Form ADV filings would reduce the marginal cost of increased enforcement by facilitating investors' use of these data.

This should reduce the marginal benefit to an investment adviser of committing fraud due to an increase in the probability of detection.

Improved public access to these disclosure data could reduce the occurrence of fraud