Portfolio diversification also generally offer equivalent expected returns with lower overall volatility of returns,which means the risk is reduced.

Portfolio approach to investing: evaluating individual securities in relation to their contribution to the risk and return of the whole portfolio分析对投资组合的影响

Porttfolio Management Process

Planning

Understanding the clients'objectives and constraints.

Developing the investment policy statement (IPS).

The benchmark should be specified in IPS for evaluation.

IPS should be reviewed and updated regularly.

Execution

Asset allocation

Security analysis

Portfolio construction and trade executions

Feedback

Portfolio monitoring and rebalancing

Performance evaluation and reporting

Types of Investors

Type of investors

Individual investors

Individuals

Defined contribution (DC) pension plan归类于个人投资

Institutional investors

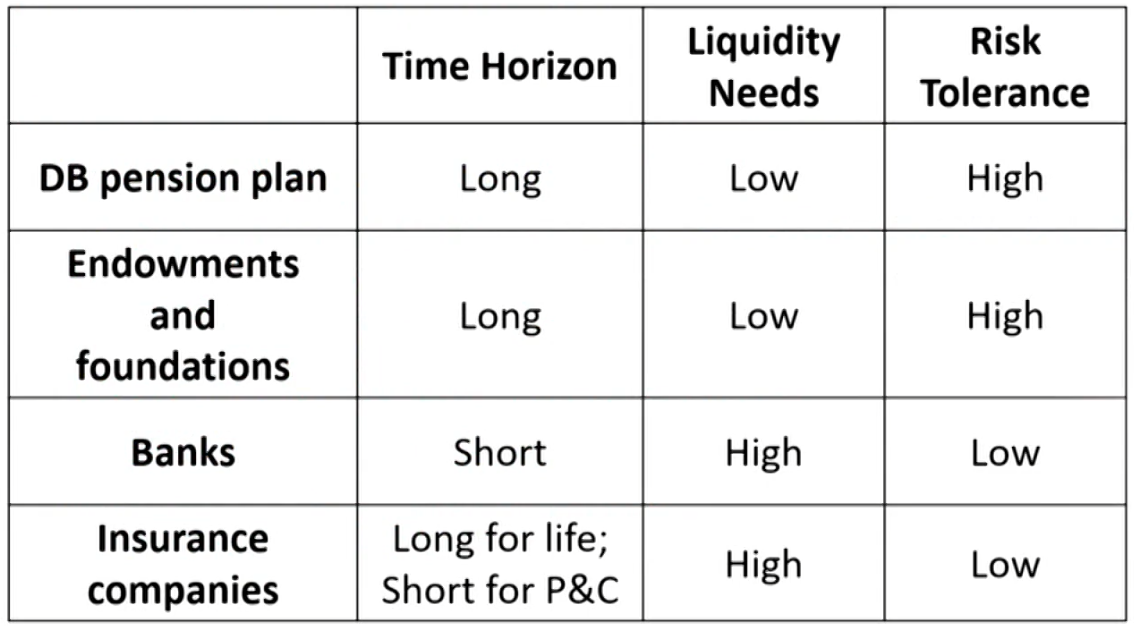

Defined benefit (DB) pension plan

Endowments and foundations

Banks

Insurance companies

Sovereign wealth funds

Defined contribution pension plan

Individuals makes specified contributions to pension plan.

The benefits are not guaranteed, and individuals accept the investment risk and rewards.

Defined benefit pension plan

Employers obligate to pay specified amount to their employees after their retirements.

High need for income

The benefits are defined, and employers accept the investment risk.

Characteristics and needs:

Investment time horizon: typically long

Income needs: varies by employees' age

Liquidity needs: typically low

Risk tolerance: typically high

Endowments & foundations

To maintain the real (inflation-adjusted) capital value of the fund while generating income to fund the objectives of the institution.

Characteristics and needs:

Investment time horizon: the longest(typically perpetual)

Income needs: to meet spending commitments

Liquidity needs: low

Risk tolerance: high

Banks

Accept deposits and extend loans, and earn a return on its reserves that exceeds the rate of interest it pays on its deposits.

Characteristics and needs:

Investment time horizon: short

Income needs: to pay interest on deposits

Liquidity needs: the highest

Risk tolerance: low

Insurance companies

Investing the premiums in a manner to pay the claims.

Characteristics and needs:

Investment time horizon: long for life insurance companies; short for property & Casualty (P&C) insurance companies

Income needs: typically low

Liquidity needs: high

Risk tolerance: low

Summary of characteristics and needs

Pooled Investments

Pooled investments

Mutual funds一起给基金经理管理

Open-end funds

Closed-end funds

Most of investors are investment companies

Exchanged traded funds (ETF)

No capital gain distributions

Separately managed accounts

Hedged funds

No regulation

Buyout funds

Few large investments in private companies

Venture capital funds

Open-end mutual funds

Investors can buy and redeem the mutual fund shares at net asset value (NAV).随时申购赎回,价格为NAV

Number of shares issued would increase as new investments are made, or decrease when withdrawn occur.

Not fully invested as some cash kept for redemption.保留一部分资金应对赎回

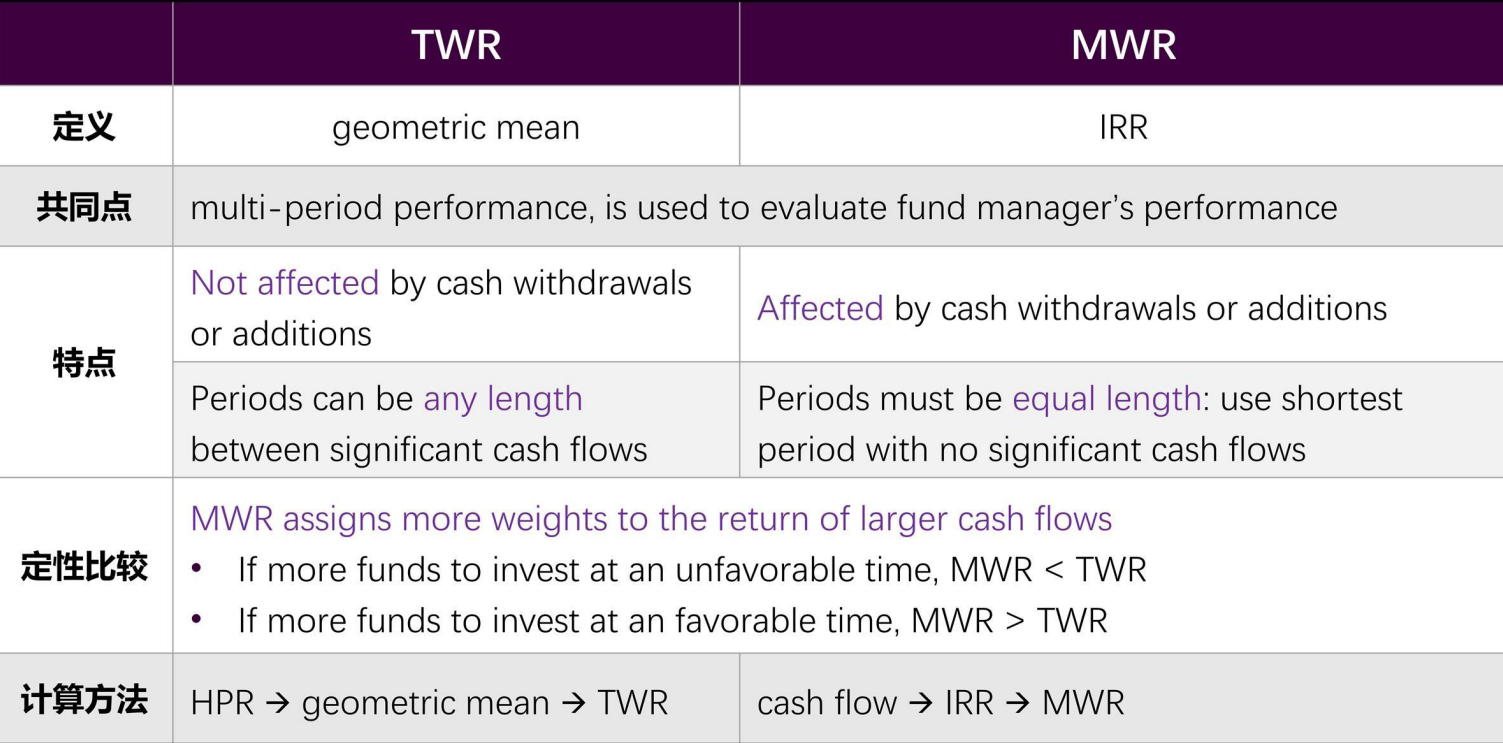

Not affected by cash withdrawals or additions.不受现金流影响

Periods can be any length between significant cash flows.每一期长度可以不一样

Money weighted return:

Affected by cash withdrawals or additions.受现金流影响

Periods must be equal length: use shortest period with no significant cash flows.每一期长度必须不一样

Assign more weights to the return of larger cash flows.受大现金流影响大

If more funds to invest at an unfavorable time, MWR will tend to be depressed熊市小

if more funds to invest at a favorable time, MWR will tend to be elevated.牛市大

Measurements of risk

Population variance & Standard deviation\sigma^2=\frac{\sum_{i=1}^N\left(X_i-\mu\right)^2}{N} \quad \sigma=\sqrt{\frac{\sum_{i=1}^{\mathrm{N}}\left(X_i-\mu\right)^2}{N}}

Sample variance & Standard deviations^2=\frac{\sum_{i=1}^N\left(X_i-\bar{X}\right)^2}{n-1} \quad s=\sqrt{\frac{\sum_{i=1}^N\left(X_i-\bar{X}\right)^2}{n-1}}

Utility Theory

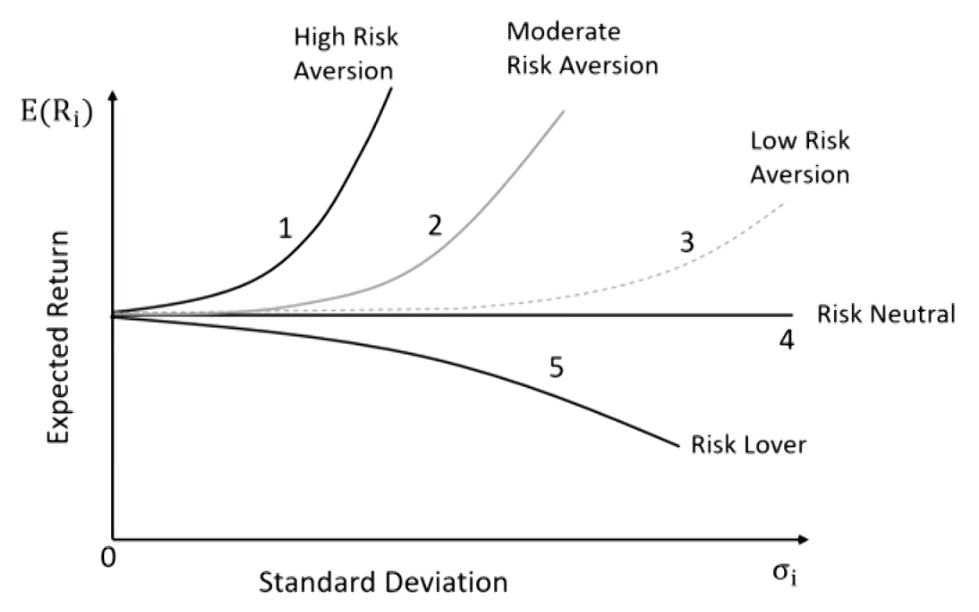

Risk aversion

Risk averse

Investors prefer less risk given certain expected return, and prefer higher expected return given certain risk.

Risk neutral

Investors are indifferent with the risk given certain expected return.

Risk seeking

Investors prefer higher risk given certain expected return.

Utility function

A measure of relative satisfaction that an investor drives from different investment portfolios.

\mathrm{U}=\mathrm{E}(\mathrm{R})-\frac{1}{2} \mathrm{~A} \sigma^2

where:\mathrm{A}=a measure of risk aversion.

A\gt 0, when investor is risk-averse.

A=0, when investor is risk-neutral.

A\lt 0, when investor is risk-seeking.

Utility theory helps us quantify the rankings of the investment choices using risk and return.

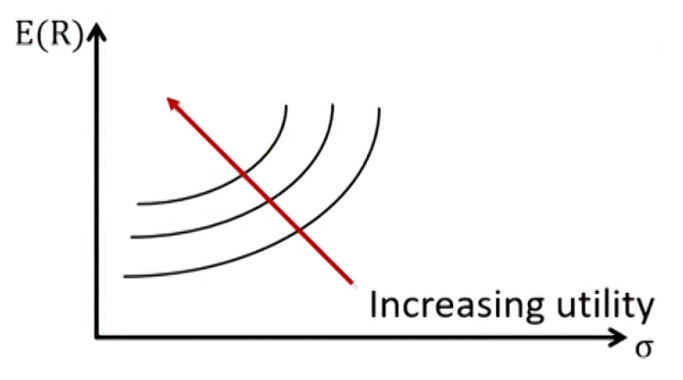

Indifference curve

Plots the combinations of risk-return pairs that an investor would accept to maintain a given level of utility.

Defined by trade-off between expected return and risk.

For risk-averse investors:

The curves slope upwardly and getting steeper.

Higher utility corresponding to a more left or upward indifference curve.

The more risk-averse the investor, the steeper the curve.

Efficient Frontier

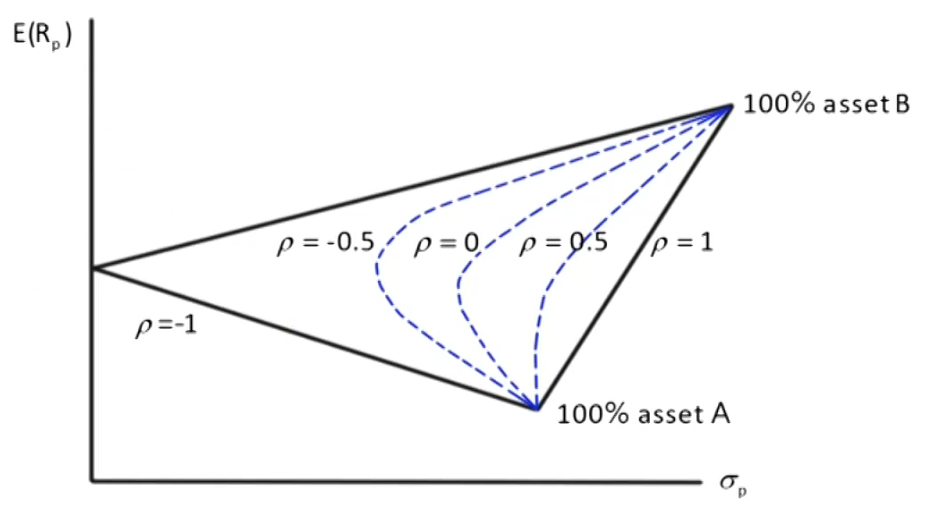

Return of portfolio with two risky assets

Return of portfolio can be measured as the weighted mean of returns of assets in the portfolio.

If \rho\lt 1(less perfectly correlated): \sigma_{\mathfrak{p}}=\sqrt{\mathrm{w}_1^2\sigma_1^2+\mathrm{w}_2^2\sigma_2^2+2\mathrm{w}_1\mathrm{w}_2\rho_{1,2} \sigma_1\sigma_2}\lt \mathrm{w}_1\sigma_1+\mathrm{w}_2\sigma_2

The portfolio risk of investing in assets that are less perfectly correlated is lower than the one with assets that are perfectly correlated。

Portfolio risk decreases as the correlation coefficient between assets within the portfolio decreases.

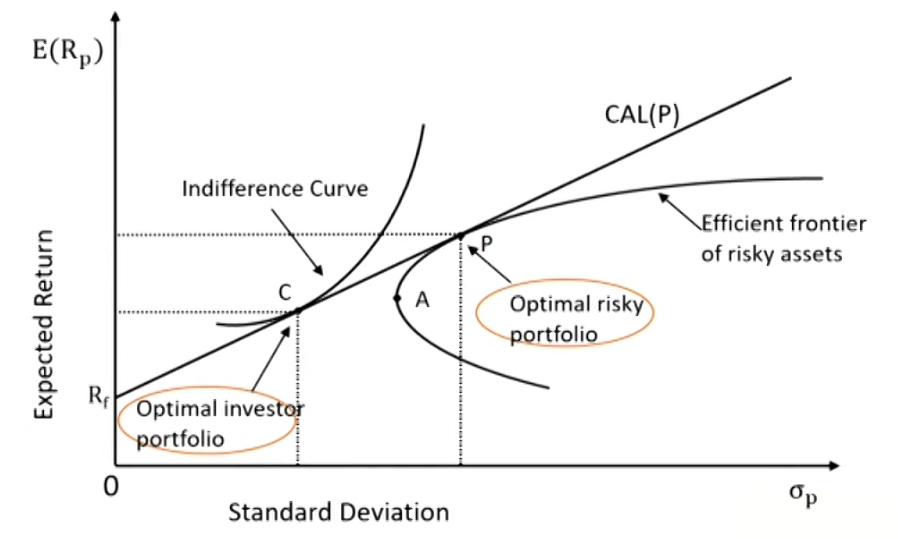

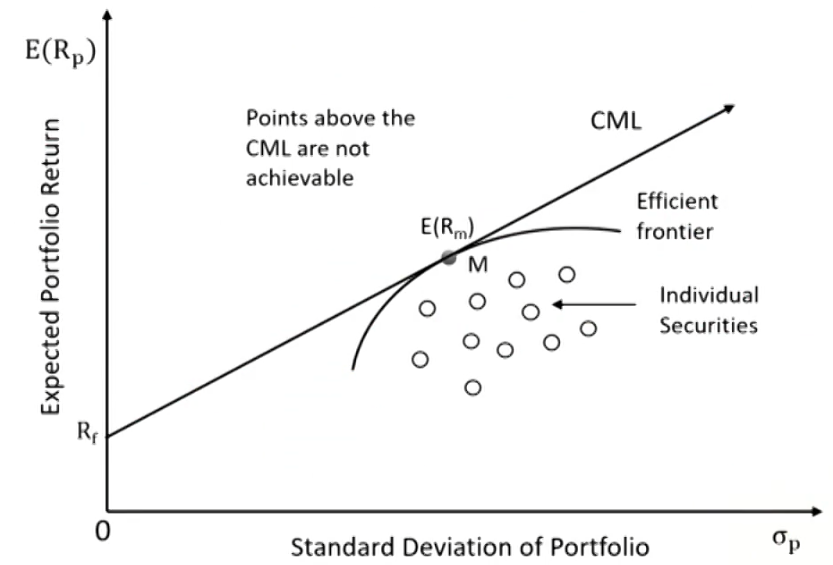

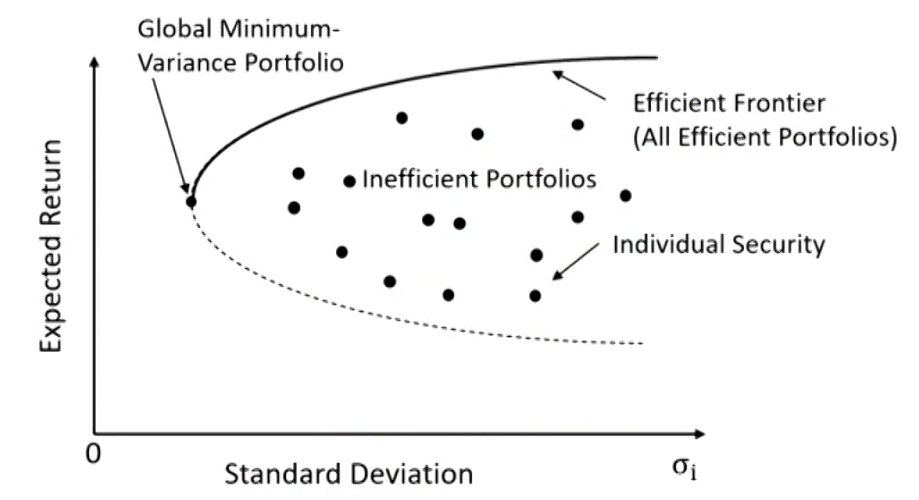

Efficient frontier of risky assets

All attainable portfolios with risky assets:

Minimum-variance frontier of risky assets: the investment portfolios of risky assets that provide minimum variance (the lowest risk) given a certain level of return.包含上下

Global minimum-variance portfolio: the investment portfolio that has the lowest variance on minimum-variance frontier of risky assets.

Efficient frontier of risky assets: the portfolios that not only provide the lowest risk given a certain level of return, but also offer the highest return given certain level of risk.

The investment portfolios on minimum-variance frontier that are above the global minimum-variance portfolio.

Portfolios above efficient frontier is not achievable, and portfolios below efficient frontier is un-efficient.

Also called Markowitz efficient frontier.

Optimal Portfolio Selection

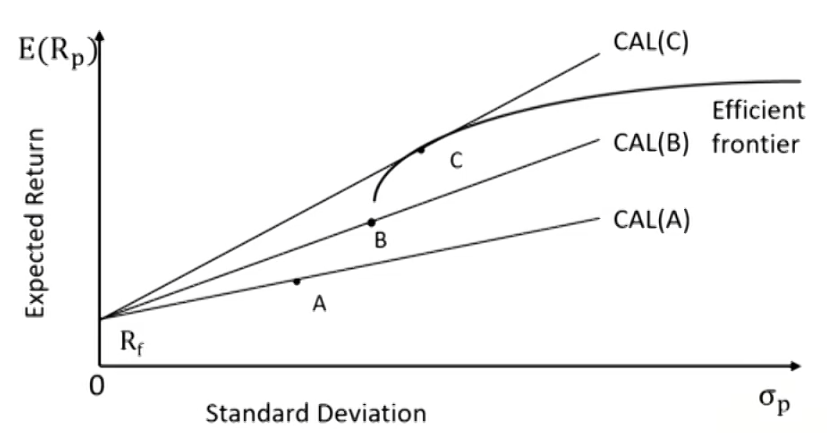

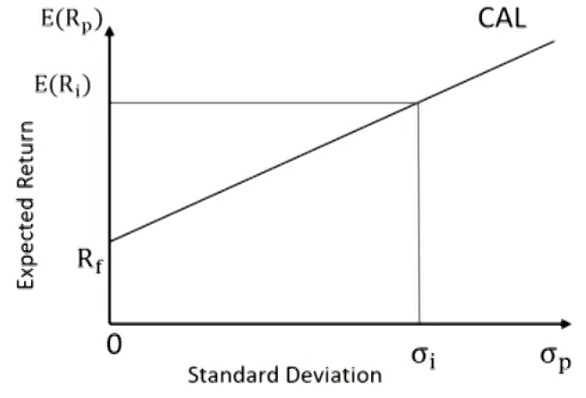

Capital allocation line(CAL)

The portfolios available to an investor through combining the risk-free asset with one risky asset. \begin{aligned} & R_p=w_i R_i+w_{r f} R_{r f} \\ & \sigma_p=w_i \sigma_i \\ & E\left(R_p\right)=R_f+\frac{E\left(R_i\right)-R_f}{\sigma_i} \sigma_p\end{aligned}

Selection among CALs

The CAL with highest Sharpe ratio should be selected.

It provides the highest utility among all CALs.

The optimal CAL is tangent to efficient frontier of risky assets.

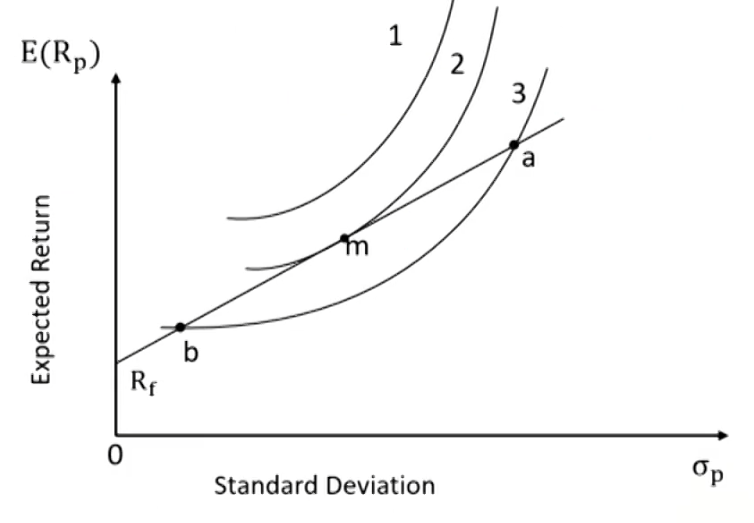

Optimal portfolio along CAL

Investor should choose portfolio "m" to invest as it supplies the most satisfaction (utility).

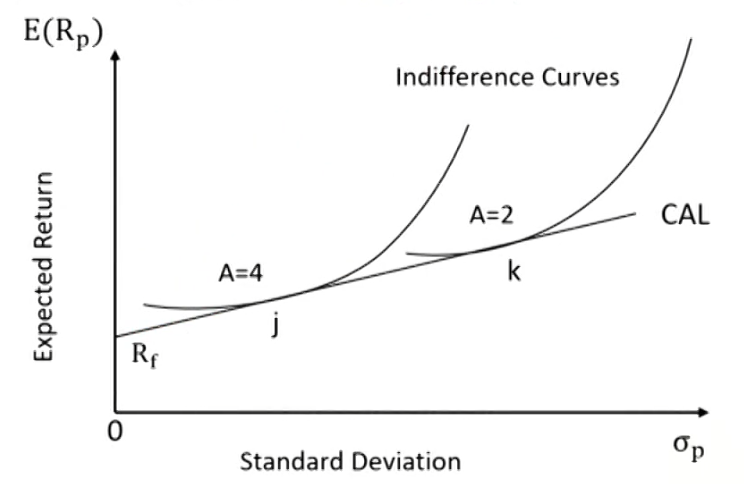

More risk-averse investor (A=4) will select portfolio "I"(less in risky asset), and less risk-averse investor (A=2) will select portfolio "k" (more in risky asset).

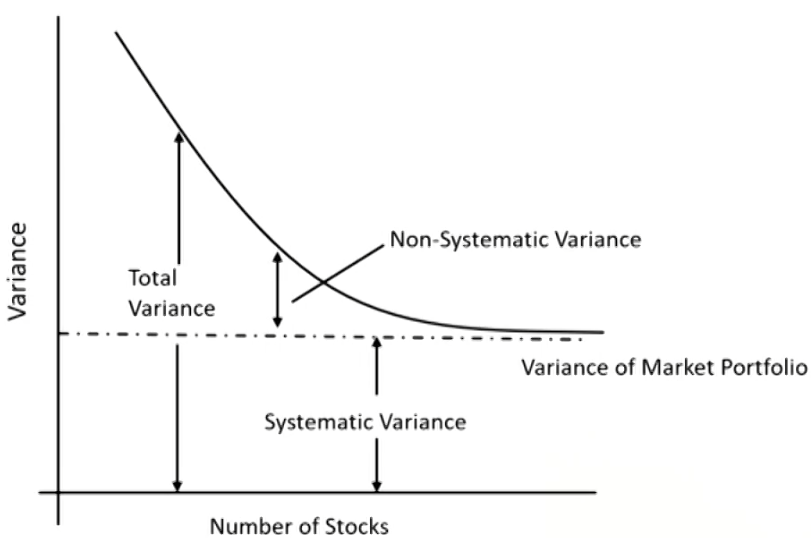

Risk affects the entire market or economy, which cannot be avoided and is inherent in the overall market.

Caused by macro factors: interest rates, GDP growth, supply shocks.

Measured by covariance of asset return and return on the market portfolio, or Beta (β) of the asset.

Investor would be only rewarded for bearing systematic risk.

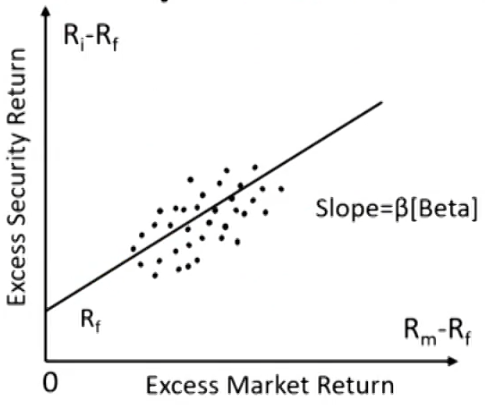

Beta(\boldsymbol{\beta})can be used to measure the systematic risk of an asset, representing how sensitive an asset's return is to the market as a whole。 \begin{aligned}

& \beta_{\mathrm{i}}=\frac{\operatorname{Cov}\left(\mathrm{R}_{\mathrm{i}}, \mathrm{R}_{\mathrm{m}}\right)}{\sigma_{\mathrm{m}}^2}=\frac{\rho_{\mathrm{i}, \mathrm{m}} \sigma_{\mathrm{i}} \sigma_{\mathrm{m}}}{\sigma_{\mathrm{m}}^2}=\rho_{\mathrm{i}, \mathrm{m}} \frac{\sigma_{\mathrm{i}}}{\sigma_{\mathrm{m}}} \\

& \beta_{\mathrm{m}}=\frac{\operatorname{cov}\left(\mathrm{R}_{\mathrm{m},} \mathrm{R}_{\mathrm{m}}\right)}{\sigma_{\mathrm{m}}^2}=\frac{\sigma_{\mathrm{m}}^2}{\sigma_{\mathrm{m}}^2}=1\\

& \beta_{\text {portfolio }}=\sum_{\mathrm{i}=1}^{\mathrm{n}} \mathrm{w}_{\mathrm{i}} \beta_{\mathrm{i}}

\end{aligned}

Unsystematic risk (firm-specific risk)

Risk that can be reduced or eliminated by holding well-diversified portfolios.

Investor would not be rewarded for bearing unsystematic risk as it could be eliminated through diversification.

Systematic risk & Unsystematic risk

Systematic risk would not change while unsystematic risk would decrease as more diversification is made within the portfolio.

Multi-factor Model

\mathrm{E}\left[\mathrm{R}_{\mathrm{i}}\right]-\mathrm{R}_{\mathrm{f}}=\beta_{\mathrm{i},1} \mathrm{E}[Factor1]+\beta_{\mathrm{i},2} \mathrm{E}[Factor2]+\cdots+\beta_{\mathrm{i}, \mathrm{k}} \mathrm{E}[Factor\left.\mathrm{k}\right]

where:\beta_{I, k}: the sensitivity of excess return on risk factor k。

Macroeconomic factors

GDP growth, inflation, consumer confidence

Fundamental factors

earnings, earnings growth, firm size, research expenditures

The expected returns (required return) of assets vary only by their systematic risk as measured by beta (\beta).

Expected return (required return) obtained from the CAPM is used for assets valuation by investors and capital budgeting to determine economic feasibility of projects.

Assumptions of CAPM

Investors are risk averse, utility-maximizing, rational individuals.

Markets are frictionless, including no cost and no taxes.

Investor plan for the same single holding period.

Investor have homogeneous expectations or beliefs.

All investments are infinitely divisible.

Investors are price takers.

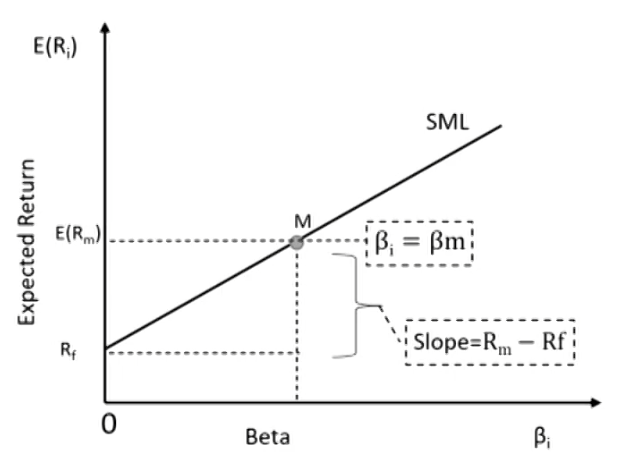

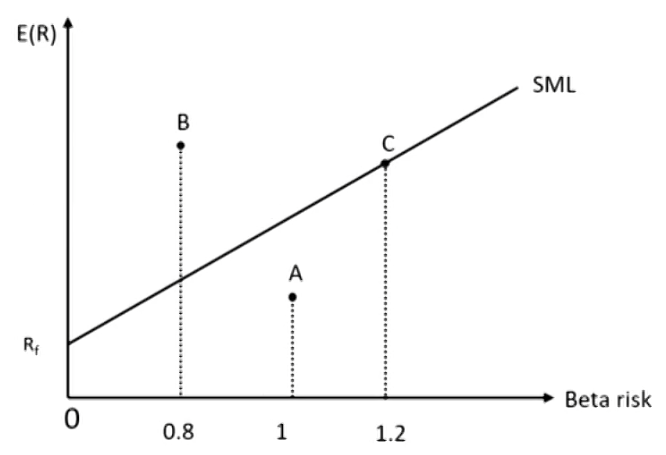

Security market line (SML)

A graphical representation of the CAPM with beta on the x-axis and expected return on the y-axis.

Intercept is Rf, slope is the market risk premium (Rm - Rf).

Any asset or portfolio that are properly priced plots on SML.

Any asset or portfolio that are overpriced plots below SML.

Any asset or portfolio that are underpriced plots above SML.

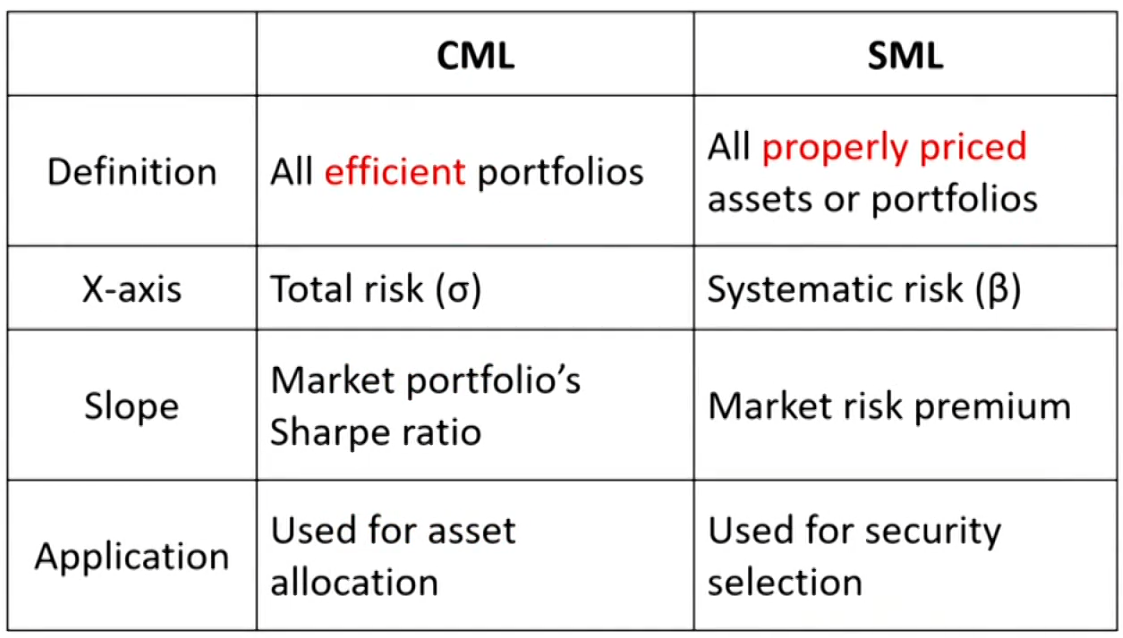

CML VS.SML

Application of CAPM

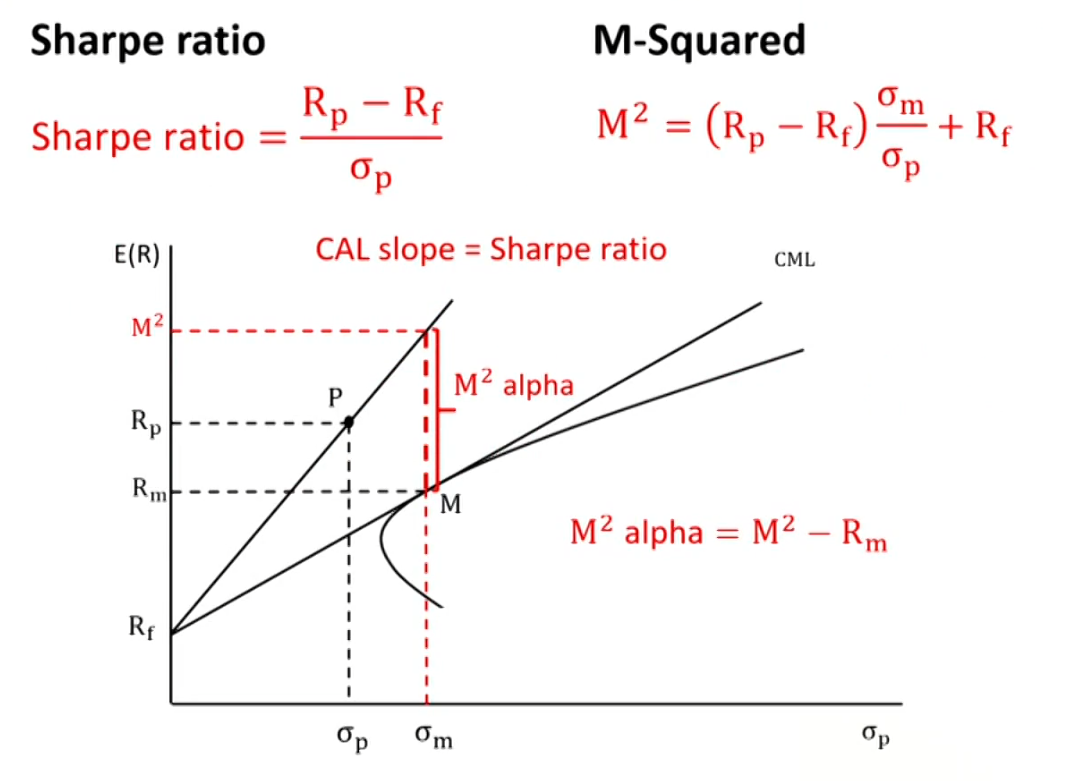

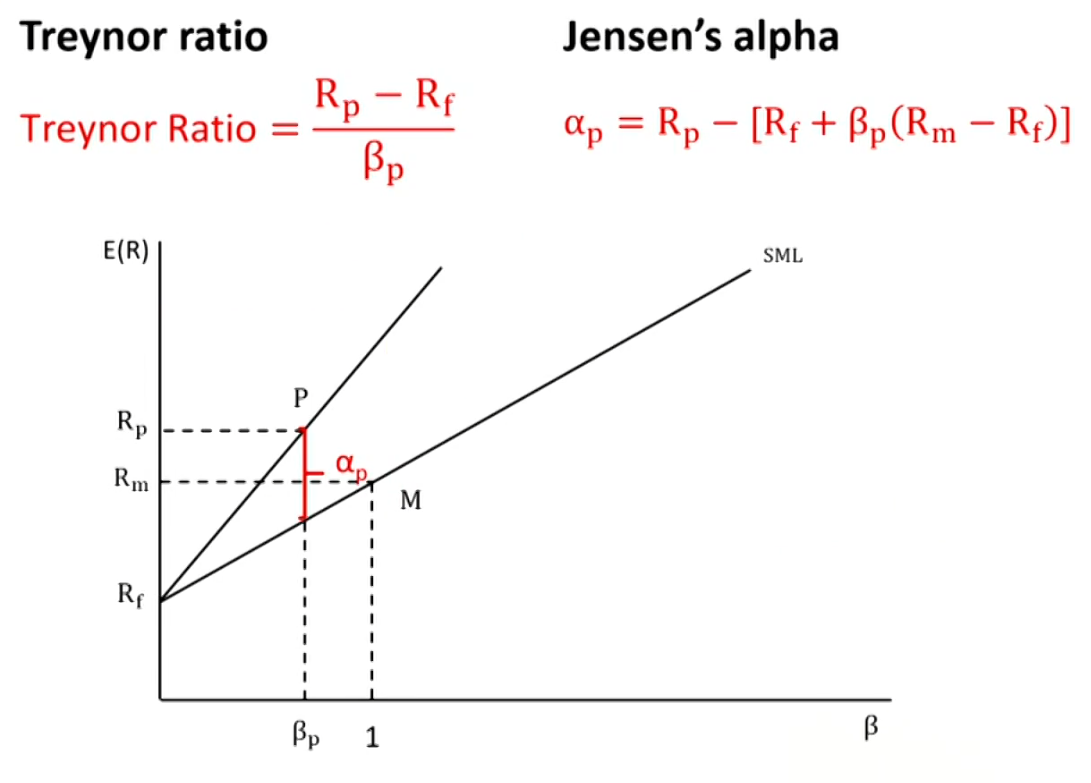

Portfolio performance evaluation

Sharpe ratio

M-Squared adjusts for total risk

Treynor ratio

Jensen's alpha adjusts for systematic risk

Basics of Portfolio Planning and Construction

Portfolio Planning

Major components of investment policy statement (IPS)

Introduction

Describes the client.

Statement of purpose

Statement of duties and responsibilities

Procedures

Steps to update IPS and procedures to respond to contingencies.

如何定期升级和应对特殊事件

Investment objectives

Client's objectives in investing (return & risk)

Investment constraints

The factors constrain the client in the investing

Investment guidelines

Execution policy(e.g., use of leverage and derivatives) and assets that are allowed to invest

Clear statement of client risk tolerance and return requirements.

Imposes investment discipline on both client and manager.

Serves as a guideline to assess the suitability of a particular investment.

Identifies a benchmark portfolio consistent with client preferences.

Return objectives

Specify what return is required by the client.

Absolute return objectives

Relative return objectives有benchmark

Risk objectives

The risk tolerance of the client is specified.

Absolute risk objectives

Relative risk objectives有benchmark

Factors dependent upon:

Psychological factors

Personal factors: age, family situation, existing wealth,insurance coverage, cash reserves, income

Ability to bear risk: depends on investment horizon, insurance,income, wealth, financial responsibilities.

Willingness to bear risk: depends on attitudes and beliefs about investment risk.

If willingness > ability: advisor should go with ability.

If ability > wilingness: educate the investor about investment risk, but do not attempt to change personality/psychological characteristics.

Investment constraints (TTLLU)

Time horizon: the time until the proceeds of the investment will be required.

Tax concerns: is the account taxable,tax-deferred, or tax-exempt.

Liquidity: the potential need for cash.

Legal and regulatory: applies more to institutional investors,but also affects individual investors (e.g., IRA accounts).

Unique needs and preferences: anything that does not fit into the above categories.

Portfolio Construction

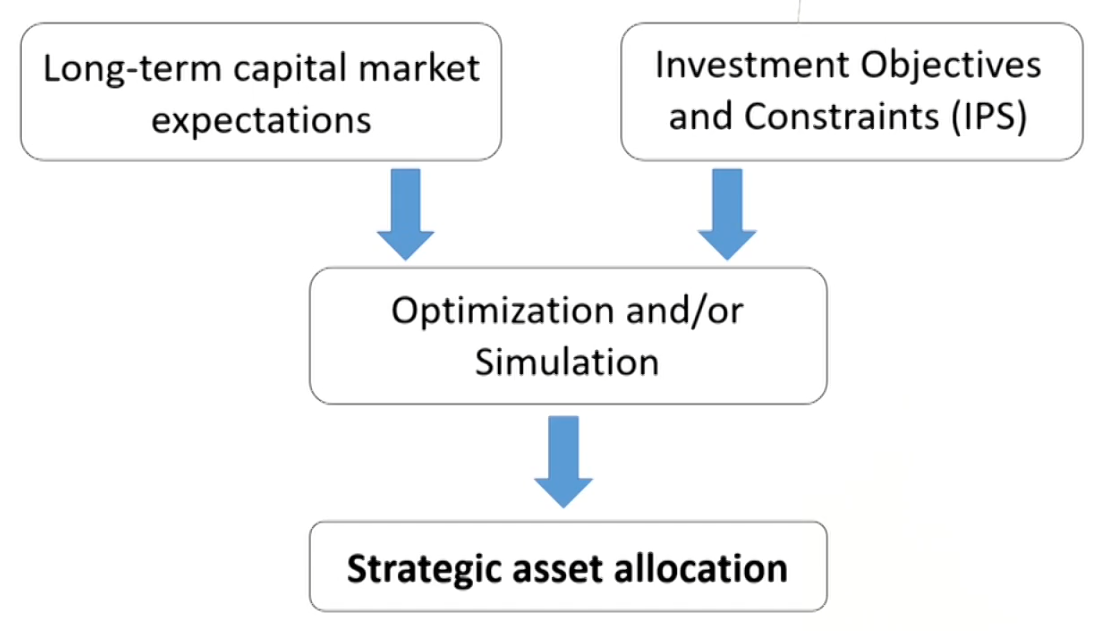

Strategic asset allocation

Specifications of asset classes:

Correlations of returns of assetg within an asset class should be relatively high.

Correlations of returns between asset classes should be low.

Steps of portfolio construction

Use risk, return, and correlations among asset classes to construct an efficient frontier.

Strategic asset allocation(SAA,长期): use objectives and constraints from IPS to select an optimal portfolio.

Correlations of returns of assets within an asset class should be relatively high同一类资产的相关性高

Correlations of returns between asset classes should below不同类的相关性低

Tactical asset allocation (TAA,短期), and security selection as permitted and appropriate.

允许偏离IPS的要求

Security selection and rebalancing.

Risk budgeting: allocates permitted risk to strategic allocation,tactical allocation, and security selection.

ESG considerations

Environmental issues

Carbon emissions, air pollution, biodiversity, etc.

Social issues

Labor standards, human rights, community relations, etc.

Governance issues

Board composition, bribery and corruption, executive compensation, etc.

ESG considerations implementation approaches

Negative screening (exclusionary screening)

Best-in-class

Best-in-class vs. shareholder engagement

Thematic investing

ESG integration

The Behavioral Biases of Individuals

Cognitive Errors

Behavioral biases and categorizations

People often rely on basic judgments and preferences to simplify the situation rather than acting completely rationally.

Behavioral biases come in two forms.

Cognitive errors: faulty cognitive reasoning.

Can be corrected or eliminated through education.

Emotional biases: based on feelings or emotions.

Arise spontaneously无意识的 rather than through conscious effort.

Are harder to correct and should be adapted.

Belief perseverance biases(RICH,固执己见)

Belief perseverance biases is the tendency to cling to one's previously held beliefs irrationally or illogically.固执己见

Conservatism bias

Confirmation bias

Representativeness bias

Illusion of control bias

Hindsight bias

Representativeness bias代表性偏差

Definition: the tendency to classify new information based on past experiences and classifications.

Two types: Base-rate neglect忽略了过去,只看到当下; Sample-size neglect用小样本的结论代替群体

Consequences:

Adopt a forecast based on individual, specific information or a small sample.

Update beliefs using simple classifications rather than deal with complex data.

Illusion of control bias控制错觉偏差

Definition: people tend to believe that they can control or influence outcomes when, in fact, they cannot.感觉自己能影响一切

Consequences:

Inadequately diversify portfolios.

Trade too often.

Construct financial models and forecasts that are overly detailed.

Conservatism bias保守性偏差

Definition: people maintain their prior views or forecasts by inadequately incorporating new, conflicting information.对新信息缺少反应

Consequences:

Maintain or be slow to update a view or a forecast, even when presented with new information.

Maintain a prior belief rather than deal with the mental stress of updating beliefs given complex data.

Confirmation biass选择偏差

Definition: the tendency to notice what confirms prior beliefs and to ignore whatever contradicts them.偏向于符合自己观点的信息,忽略不符合自己认知的信息

Consequences:

Consider only the positive information and therefore hold investments too long.

Develop screening criteria to find what they want to see.

Under-diversified portfolios.

Overly concentrate in the stock of their employer.

Hindsight bias事后诸葛亮

Definition: people tend to believe past events as having been predictable and reasonable to expect.马后炮

Consequences:

Overestimate the degree to which they correctly predicted an investment outcome, which could reinforce an emotional overconfidence.

Overly critical of the performance of others.

Information processing errors(FAMA,处理有误)

Information Processing describing how information may be processed and used irrationally in financial decision making.

Anchoring and adjustment bias

Mental accounting bias

Framing bias

Availability bias

Framing bias框架效应

Definition: people tend to answer a question differently based on the way in which it is asked or framed.同样的事情,表述不同感受不同

Consequences:

Misidentify risk tolerances because of how questions about risk tolerance were framed.

Focus on short-term price fluctuations and trade too often,

Availability bias可得性偏差

Definition: people tend to estimate the probability of an outcome based on how easily information is recalled.唾手可得的信息影响力更大

Consequences:

Limit their investment opportunity set.

Choose an investment based on advertising or the quantity of news coverage.

Fail to diversify.

Mental accounting bias心理账户

Definition: people tend to mentally divide money into "accounts" that influence decisions.对不同来源的钱,风险承受能力不同

Consequences:

Fail to reduce risk by combining assets with low correlations.

Overemphasis on income generating assets, resulting in a lower total return.

Anchoring and adjustment bias锚定效应

Definition: people tend to rely on an initial piece of information to make subsequent estimates and decisions.决策不是客观的,而是围绕已有的东西

Consequences:

Stick too closely to their original estimates when learning new information.

Emotional Biases

Emotional Biases

Emotional biases are harder to correct for than cognitive errors because they originate from/impulsejorintuition

Loss-aversion bias

Overconfidence bias

Self-control bias

Status quo bias

Endowment bias

Regret-aversion bias

loss-aversion bias损失厌恶

Definition: tendency to strongly prefer avoiding losses to achieving gains.面对损失风险偏好

Consequences:

Disposition effect: Hold investments in a loss position longer than justified. Sell investments in a gain position earlier than justified.

Overconfidence bias过度自信

Definition: people demonstrate unwarranted faith in their own abilities.觉得自己什么都行

Intensified when combined with self-attribution bias做对了功劳是自己的,做错了错误是他人的, in which people take too much credit for successes and assign responsibility to others for failures.加剧过度自信

Consequences:

Underestimate risks and overestimate expected returns.

Hold poorly diversified portfolios.

Self-control bias自控

Definition: people fail to act in pursuit of their long-term,overarching goals because of lack of self-discipline.对自己缺乏控制

Consequences:

Save insufficiently for the future.

Borrow excessively to finance present consumption.

Status quo bias懒

Definition: people choose to do nothing instead of making a change.没有执行力

Consequences:

Holding portfolios with inappropriate risk.

Fail to explore other opportunities.

Endowment bias禀赋效应

Definition: people value an asset more when they own it than when they do not.对自己拥有的东西产生更好的印象

Consequences:

Failing to sell an inappropriate asset resulting in inappropriate asset allocation.

Holding things you are familiar with because they provide some intangible sense of comfort

Regret-aversion bias后悔厌恶

Definition: people tend to avoid making decisions out of fear that the decision will turn out poorly.害怕后悔

Consequences:

Be too conservative in their investment choices as a result of poor outcomes in the past.

Engage in herding behavior.

Market Behavior

Defining market anomalies

Anomalies are apparent deviations from the efficient market hypothesis与有效市场相悖, identified by persistent abnormal returns带来持续的超额收益 that differ from zero and are predictable in direction.

Not every deviation is anomalous. Misclassifications tend to stem from three sources:

Choice of asset pricing model模型不同

Statistical issues统计有误

Temporary disequilibria只是短暂异常

Momentum

Future price behavior correlates positively with that of the recent past.价格变化有惯性

Momentum can be partly explained by:

Availability bias,

Hindsight bias.

Regret-aversion

Bubbles and crashes

There are several different types of behavior that are evident during bubbles市场泡沫与破裂

Overconfidence → excessive trading and underestimation of risks.

Confirmation bias,

Self-attribution bias,

Hindsight bias.

Regret aversion bias.

Anchoring bias.

Investment managers incentivized or accountable for short-term performance by current and prospective clients is a potentially explanation

Value stocks

Value stocks are typically with low price-to-earnings ratios, high book-to-market equity. Growth stocks are the opposite. Fama and French found that value stocks historically outperformed growth stock, which could be explained by:价值股比成长股表现好

The halo effect, a company with a good growth record might be seen as a good investment, which is a form of representativeness.聚光灯效应

Overconfidence can also be involved in predicting growth rates, leading growth stocks to be overvalued.过度自信

Introduction to Risk Management

Basics of Risk Management

Risk

Broadly speaking, exposure to uncertainty.

Risk exposure

Actual risk borne by a business or investor.

Risk management

Defines the level of risk to be taken, measures the level of risk being taken, and adjusts the latter toward the former, to maximize the portfolio's value.

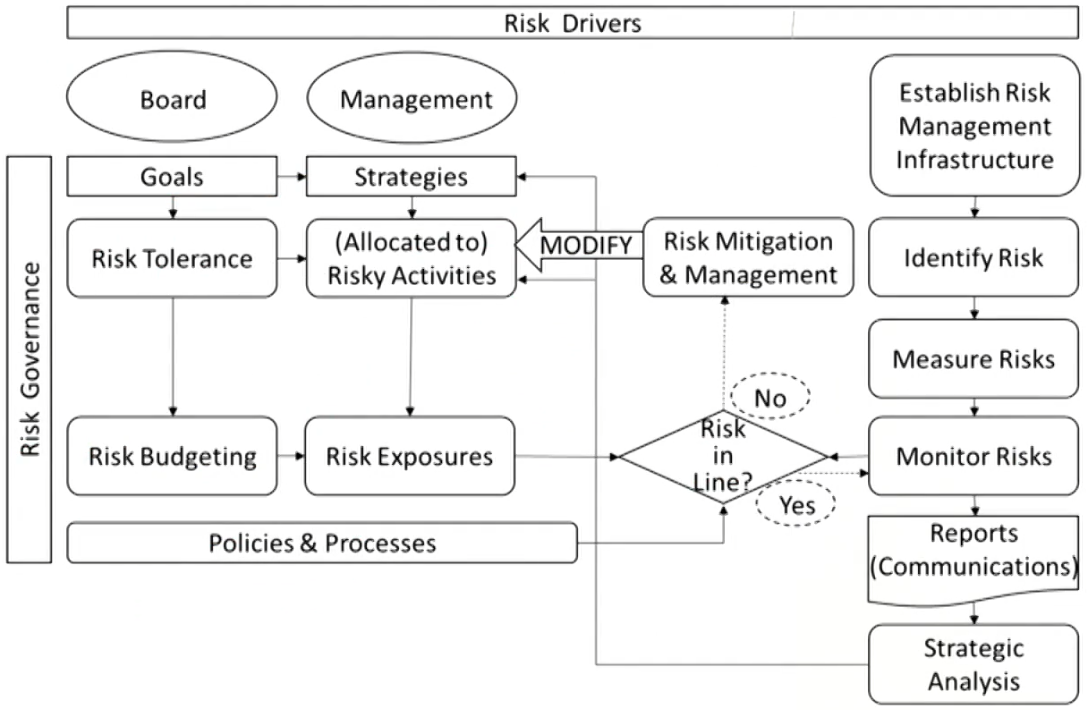

Risk management framework

The infrastructure, process, and analytics needed to support effective risk management in an organization.

Risk governance: the top-down process and guidance that directs risk management activities to the overall enterprise.

Risk identification and measurement

Risk infrastructure: the people and systems required to track risk exposures and perform the quantitative risk analysis to assess the organization's risk profile.

Policies and processes: the extension of risk governance into both the day-to-day operation and decision-making processes of the organization.

Risk monitoring, mitigation, and management

Communication

Strategic analysis and integration

Elements of effective risk governance

Enterprise risk management

Provides an enterprise-view of risk management.Focus risk activities on the entire organization.

Risk tolerance (risk appetite)

Identifies the extent to which the entity is willing to experience losses or fail in meeting its objectives.

Risk budgeting

Quantifies and allocates the tolerable risk by specific metrics.

Effects of risk tolerance on risk management

Serve as the high-level guidance for management in its strategic selection of risks.

Delineates which risks are acceptable, which are unacceptable, and how much risk the overall organization can be exposed to.

Target where it should actively pursue risk and where it should mitigate or modify risk

Role of risk budgeting in risk governance

Guides implementation of the risk tolerance decision at strategic level.

A means of bridging from the high-level governance risk decision to the many management decisions, large and small,that result in the actual risk exposures.

Risk Management Process

Risk management process

Identification of risk

Measurement of risk

Modification of risk

Financial risk

The risks that arise from events occurring in the financial markets.

E.g., changes in prices or interest rates.

Market risk

Risks that arise from movements in interest rates, stock prices, exchange rates, and commodity prices

Credit risk

Risk of loss if one party fails to pay an amount owed on an obligation (e.g., bond, loan, derivative) to another party.

Liquidity risk

Risk of a significant downward valuation adjustment when selling a financial asset.

Non-financial risk

The risks that emanate from outside the financial markets, such as actions within an entity, or from external origins.

E.g., environment, the community, regulators, politicians,suppliers, and customers.

Settlement risk结算风险

Closely related to default risk but deals more with the settling of payments that occur just before a default.

Legal risk法律风险

The risk of being sued over a transaction or for that matter,anything an entity does or fails to do.

Model risk用错模型

The risk of a valuation error from improperly using a model.

Tail risk极端事件发生

More events in the tail of the distribution than would be expected by probability models.

Operational risk操作风险

Risk that results from failure in internal procedures, as well as from some special external events.

Solvency risk清偿风险

Risk that the entity does not survive because it runs out of cash, even though it might otherwise be solvent.

Compliance risk合规风险

Risks that deal with the matter of conforming to policies,laws, rules, and regulations.

Regulatory risk.

Accounting risk.

Tax risk.

Interactions of risks

Risks do not usually arise independently, but generally interact with one another, a problem that is even more critical in stressed market conditions.

A measure of the minimum amount of loss expected for a given period at a given level of probability.

Extreme value theory (EVT)

Scenario analysis and stress testing

Measurement of credit risk

Credit rating (Moody's, Fitch, S&P)

Solvency ratios偿付比率 (e.g., current ratio)

Profitability ratios盈利指标(e.g., ROA, ROE)

Leverage measures杠杆(e.g., debt-to-asset ratio)

Credit VaR信用VaR值, probability of default, expected loss given default,and the probability of a credit rating change

Ex-ante risk cost (e.g., CDS, put options, exotic options,insurance contracts)

Methods of risk modification

Risk prevention and avoidance完全避免,不做了

Risk acceptance保留部分: self-insurance and diversification处置掉非系统风险

Risk transfer买保险

Risk shifting对冲

Factor considered in choosing the methods

Trade-off between costs and benefits

Technical Analysis

Basics of Technical Analysis

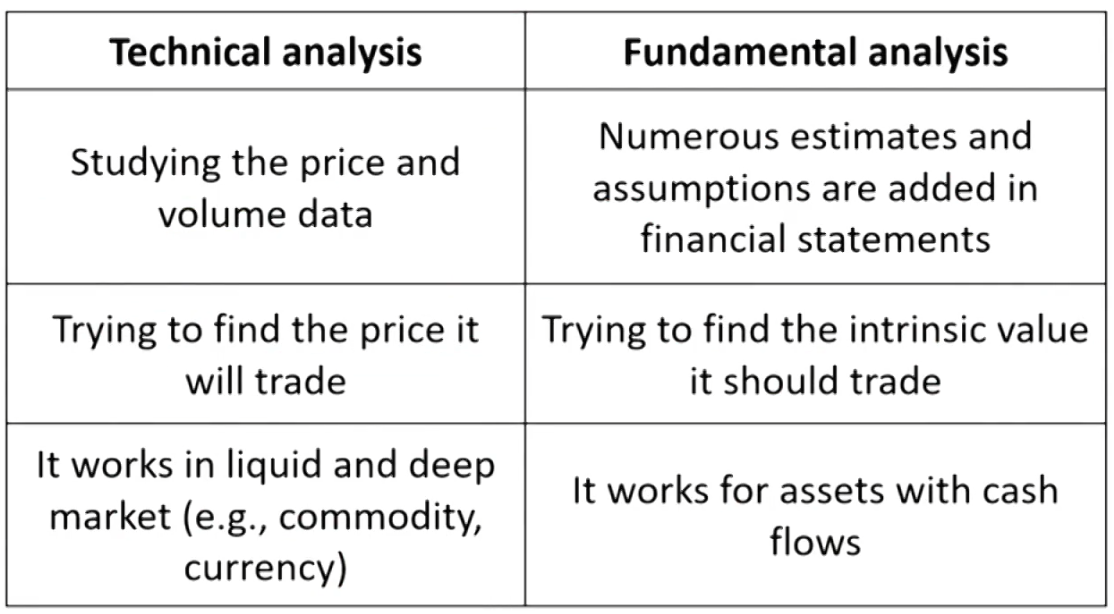

Technical analysis

Analyzed using price and volume data分析价格和量.

Prices are determined by supply and demand.

Past price action can be used to forecast future prices movement with charts and other technical tools.

Principles and assumptions

The market discounts everything.

Market price already reflects all known factors impacting a financial instrument.

Prices move in trends and countertrends.

Price action is repetitive, and certain patterns tend to reoccur.

Technical analysis and behavioral finance

Technical analysis is the study of collective investor psychology and thus has a direct connection with behavioral finance.基于共识

Technicians believe that:

Trades determine volume and price.

Buying and selling activities may be driven by motivations that are not rational.

Market trends and patterns reflect irrational human behavior.技术分析考虑到了非理性,认为市场无效

Patterns and Indicators

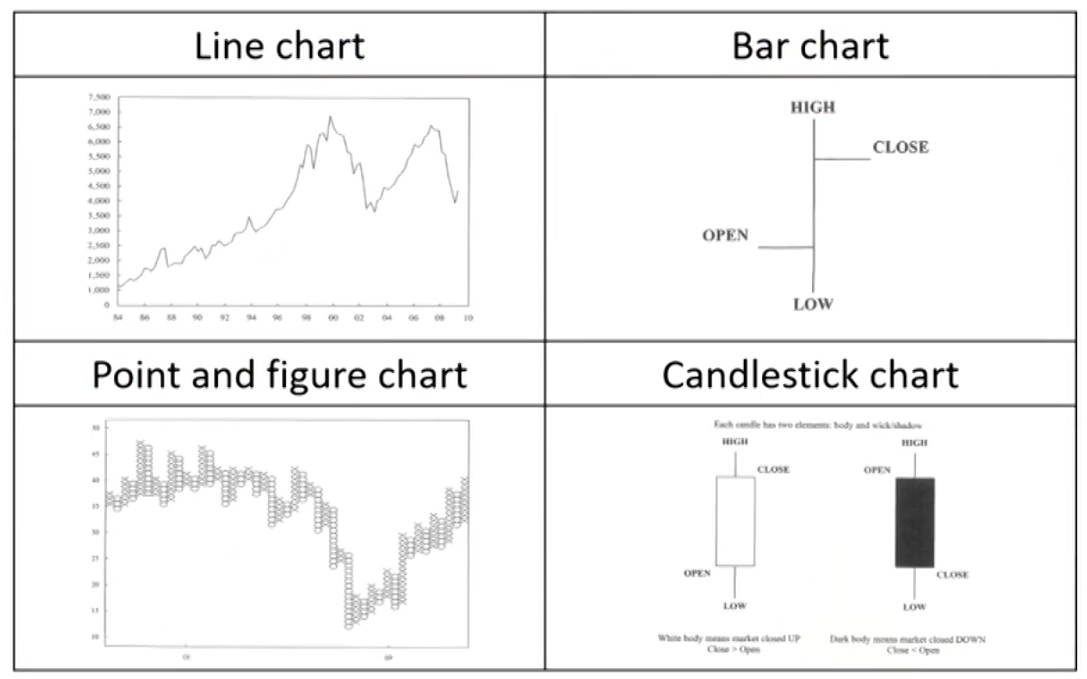

Type of charts

Patterns of charts

Trend趋势类

Uptrend: the price goes to higher highs and higher lows.

Downtrend: the price goes to lower lows and lower highs.

Support line

A low price range in which buying activity is sufficient to stop the decline in price.

Resistance line

A price range in which selling activity is sufficient to stop the rise in price.

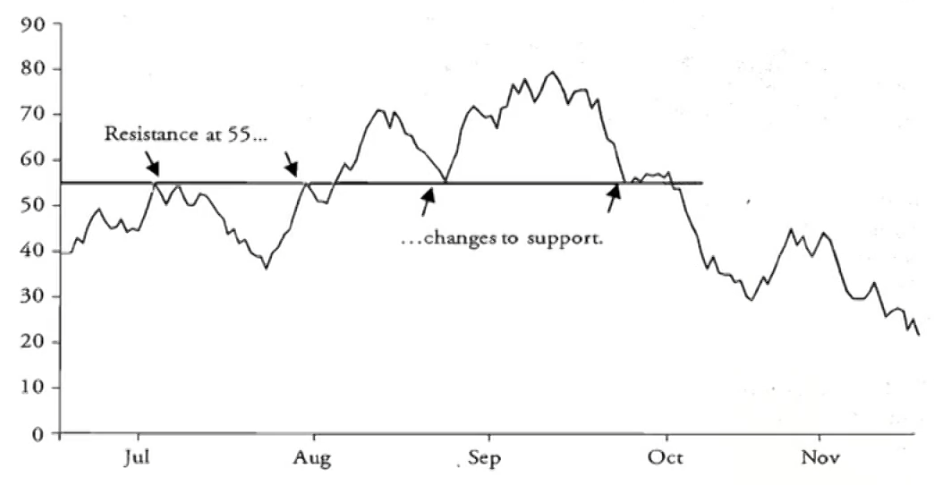

Change in polarity支撑变阻力,阻力变支撑

Once support level is breached, it becomes resistance level.

Once resistance level is breached, it becomes support level.

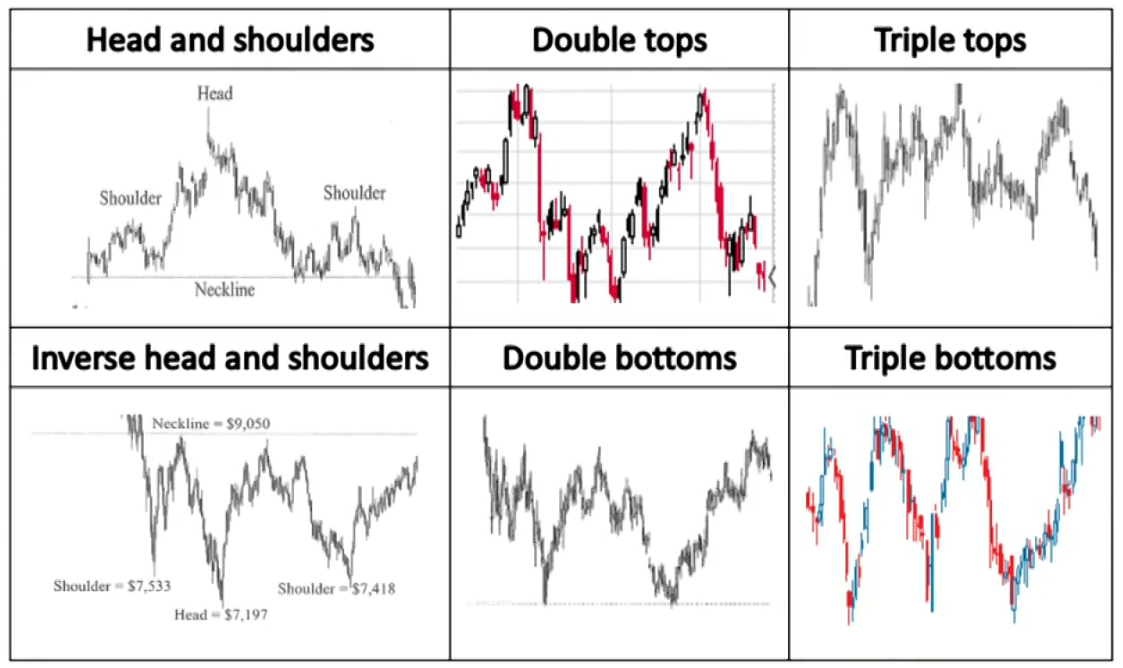

reverse patterns逆转类

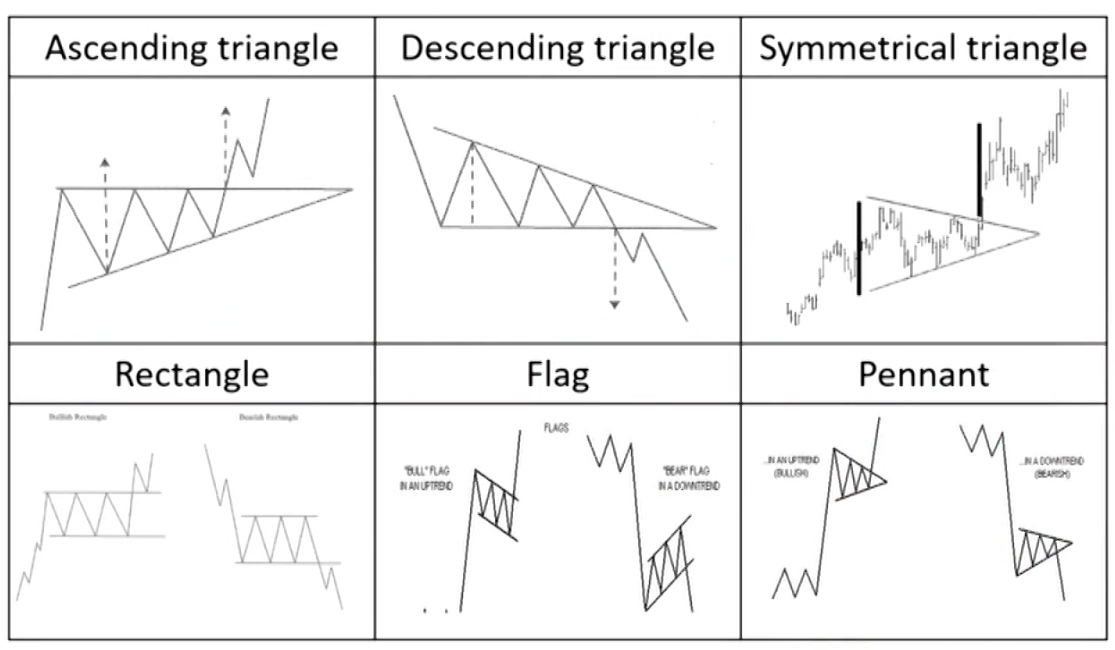

continuing patterns中继类

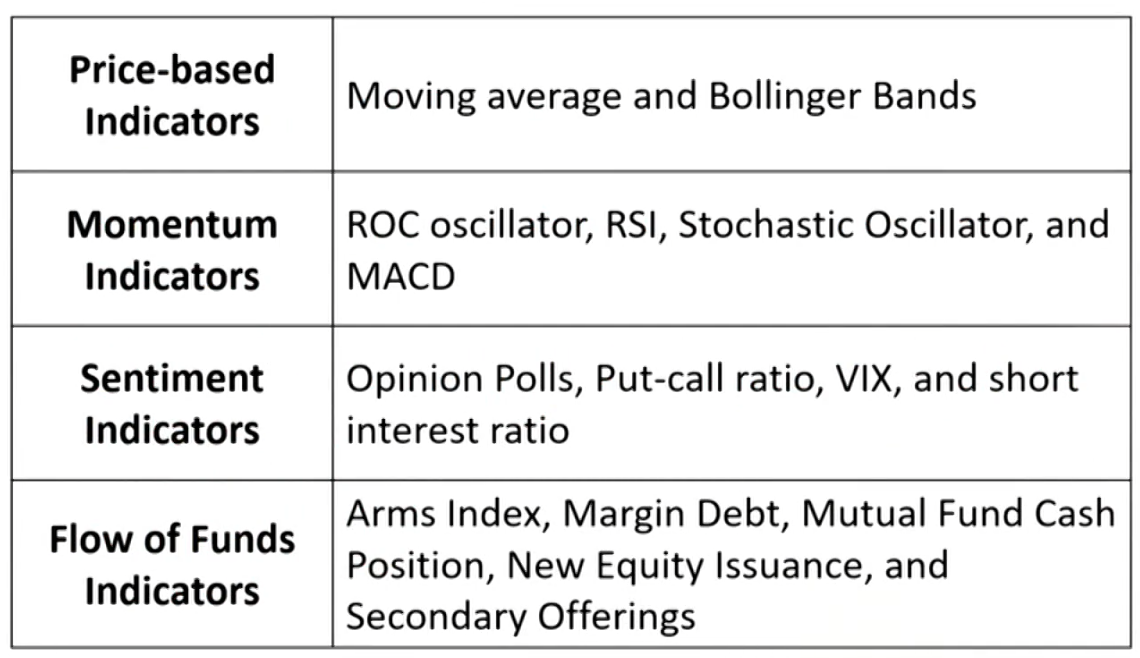

Type of technical analysis indicators

Cycle analysis周期理论

Kondratieff wave: 54-year

18-year cycle

Decennial cycle:10 years

Presidential cycle: 4 years

Elliott wave theory波浪理论

Up trends and down trends

Wave sizes conform to Fibonacci sequence

Inter-market Analysis

Inter-market analysis

Inter-market analysis is based on the principle that all markets are interrelated and influence each other.

Involves the use of relative strength analysis for different groups of securities to make allocation decisions.

E.g., stocks versus bonds, sectors in an economy, and securities from different countries.

Top-down approach

Start by analyzing global benchmarks, such as MSCl and FTSE. The relative performance of major indexes will reveal important investment themes for investors with a long-term focus.

Bottom-up approach

A bottom-up investing approach focuses on the analysis of individual stocks. A thorough technical analysis of individual stocks will reveal investment themes in different sectors and industries.

The role of the technical analyst

A technical analyst can serve a supporting role in a team of investors.

The key value-added input would be in the form of timing of the purchase or sale of that security.

Technical analyst will typically not be directly involved in position sizing decisions.

Fintech in Investment Management

Basics of Fintech

Fintech

Technological innovation in the design and delivery of financial services and products.

Analysis of large datasets (Big data).

Analytical tools(AI and Machine learning).

Automated advice (Robo-advisers).

Automated trading (Algorithms trading).

Financial record keeping(DLT).

Big Data

Traditional data: stock exchanges, financial statements,economic indicators.

Individuals: social media posts, internet search logs, etc.

Business: normal course of doing business.

Sensors: satellites, geolocation, Internet of Things, other sensors.

Big Data characteristics

Volume: many millions, or even billions, of data points.

Velocity: real-time or near-real-time.

Variety: structured data(e.g. SQL tables), semi-structured data

(e.g. HTML), and unstructured data(e.g.videos).

Big Data challenges

Quality, volume, and appropriateness of the data.

Unstructured data are more often qualitative.

Artificial intelligence and machine learning techniques have emerged.

Artificial intelligence (AI)

Enable the development of computer systems that exhibit cognitive and decision-making ability comparable or superior to that of human beings.

Neural networks (Since the 1980s): based on brain learns and processes information to detect abnormal charges or claims in credit card fraud detection systems.

Machine learning (ML)

Able to "learn" how to complete tasks, improving their performance over time with experience.

ML involves splitting the dataset into training dataset,validation dataset and test dataset.

ML still requires human judgement in understanding data and selecting the appropriate techniques for data analysis.

Overfitting may lead to prediction errors and incorrect output forecasts.

Types of machine learning

Supervised learning.

Inputs and outputs are labeled, or identified, for the algorithm.

Unsupervised learning.

Only data from which the algorithm seeks to describe the data and their structure.

Deep learning (or deep learning nets).

Often with many hidden layers, to perform multistage, non-linear data processing to identify patterns.

Fintech Application

Text analytics

Use of computer programs to analyze and derive meaning typically from large, unstructured text- or voice-based datasets to help identify future performance, such as consumer sentiment or economic trend.

Natural language processing (NLP) is a field of research at the intersection of computer science, artificial intelligence, and linguistics that focuses on developing computer programs to analyze and interpret human language.

NLP is an application of text analytics

Robo-Advisory services

Used on automated asset allocation, trade execution, portfolio optimization, tax-loss harvesting, and rebalancing.

Robo-advice start with an investor questionnaire, but it do not incorporate the full range of available information into their recommendation.

Most robo-advisers follow a passive investment approach.

Types of wealth management services

Fully Automated Digital Wealth Managers

Adviser-assisted Digital Wealth Managers

Risk analysis

Big Data may provide insights into real-time and changing market circumstances to help identify weakening market conditions and adverse trends in advance.

Stress testing, risk assessment, and scenario analysis.

ML help validate data quality by identify questionable data,potential errors, and data outliers before integration with traditional data for use in risk models and in risk management applications.

Algorithmic trading

It's the way to price the order and the most appropriate trading venue to route for execution

High speed of execution, anonymity, and lower transaction costs

High-frequency trading (HFT) algorithms decide what to buy or sell and where to execute on the basis of real-time prices and market conditions, seeking to earn a profit from intraday market mispricing.

Distributed Ledger Technology(DLT)

Create, exchange, and track ownership of financial assets on a peer-to-peer basis.

Blockchain is a type of DLT in which information, such as changes in ownership, is recorded sequentially within blocks that are then linked or "chained" together and secured using cryptographic methods.

Permissionless networks vs. permissioned networks

Applications of DLT

Cryptocurrencies

A digital currency, allows near-real-time transactions between parties without an intermediary (bank).

Initial coin offering (ICO)

Issue digital tokens to investors for purchasing future products or services being developed by the issuer.

Tokenization

Used on physical assets. Transactions can be improved by decentralized, paper-based records and multiple parties.

Post-Trading clearing and settlement

Provides near-real-time trade verification, reduced the complexity, time and costs for processing transactions.

Compliance

Allow regulators and firms to maintain near-real-time review over transactions and compliance-related processes.

Could help uncover fraudulent activity and reduce compliance costs associated with known-your-customer and anti-money-laundering regulations.

\begin{aligned} & R_p=w_i R_i+w_{r f} R_{r f} \\ & \sigma_p=w_i \sigma_i \\ & E\left(R_p\right)=R_f+\frac{E\left(R_i\right)-R_f}{\sigma_i} \sigma_p\end{aligned}

\begin{aligned} & R_p=w_i R_i+w_{r f} R_{r f} \\ & \sigma_p=w_i \sigma_i \\ & E\left(R_p\right)=R_f+\frac{E\left(R_i\right)-R_f}{\sigma_i} \sigma_p\end{aligned}