Categories,Characteristics, and Compensation Structures of Altermative Investments

Categories and Characteristics

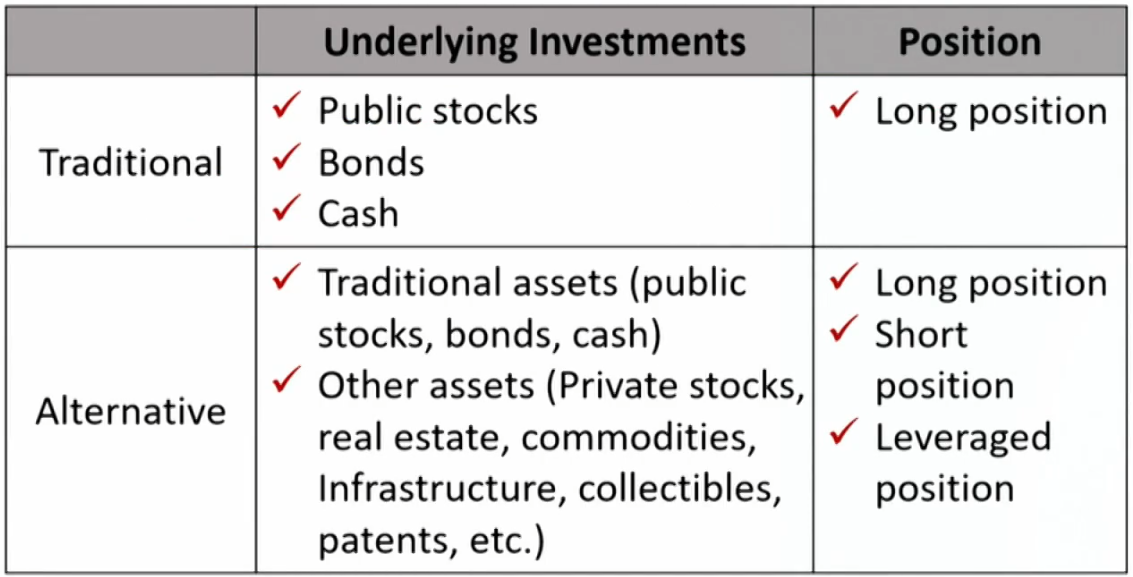

Definition of alternative investment

Characteristics of alternative

- Diversifying power: returns that are uncorrelated with or only slightly correlated with traditional investments.另类投资与其它投资关联度低,从而降低系统性风险

- Can be correlated in periods of financial crisis.

- Higher expected returns

- Illiquidity: the investment trades infrequently.交易少

- Inefficiency: market prices cannot reflect all availableinformation due to relatively low degree of competition.市场不有效

- Opportunities of arbitrage and superior risk-adjusted return

- Narrow specialization of the investment managers专业性高.

- Less regulation and less transparency than traditional investments透明度低

- Limited reliable historical risk and return data.数据少

- Unique legal and tax considerations.税少

- Higher fees, often including performance or incentive fees管理费高

- Concentrated portfolios.另类投资本身很集中

- Restrictions on redemptions (i.e., "lockups" and "gates"")难赎回

Market participants

- Endowments, pension funds, Sovereign wealth funds, and family offices.

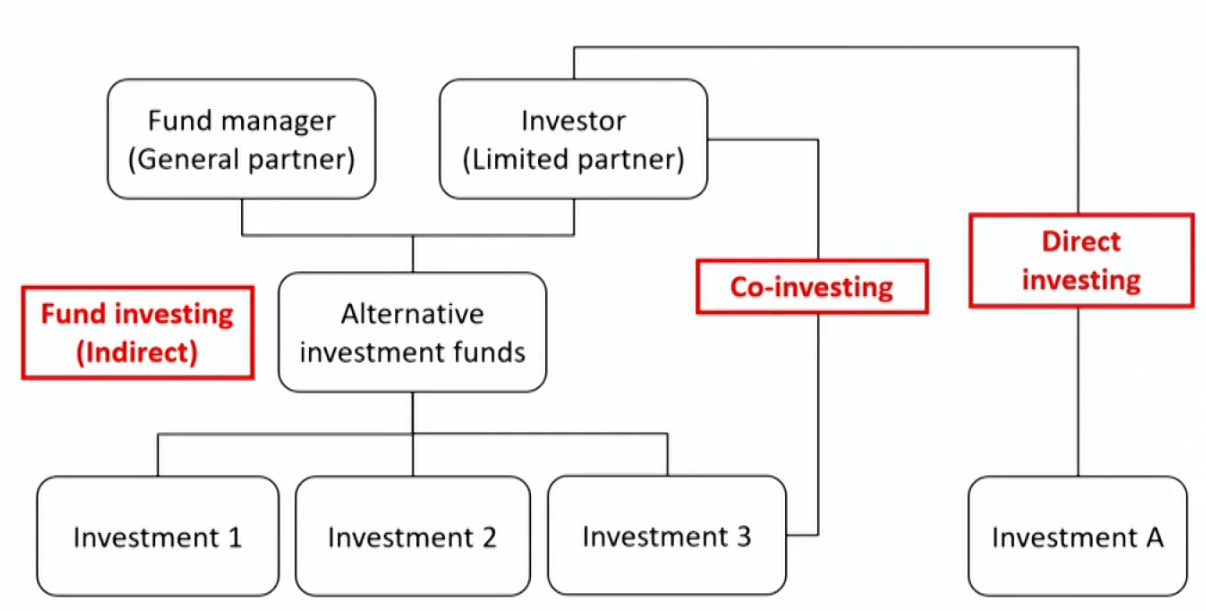

Investment Method

Three methods for alternative investments

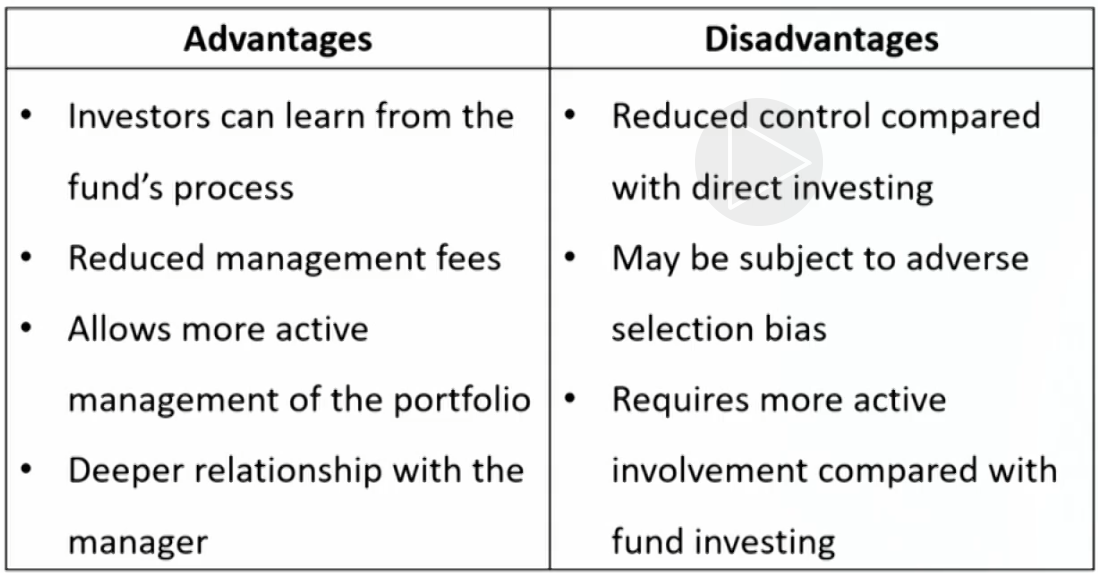

- Fund investing间接投资(GP, LP):Indirect method. Investor contributes capital to a fund,and the fund identifies, selects, and makes investments on the investor's behalf.

- Investment decisions are limited to either investing in the fund or not.

- Fund investors are typically unable to affect the fund's underlying investments.

- Investment decisions are limited to either investing in the fund or not.

- Co-investing两种都有:The investor invests in assets indirectly through the fund but also possesses rights (known as co-investment rights) to invest directly in the same assets.

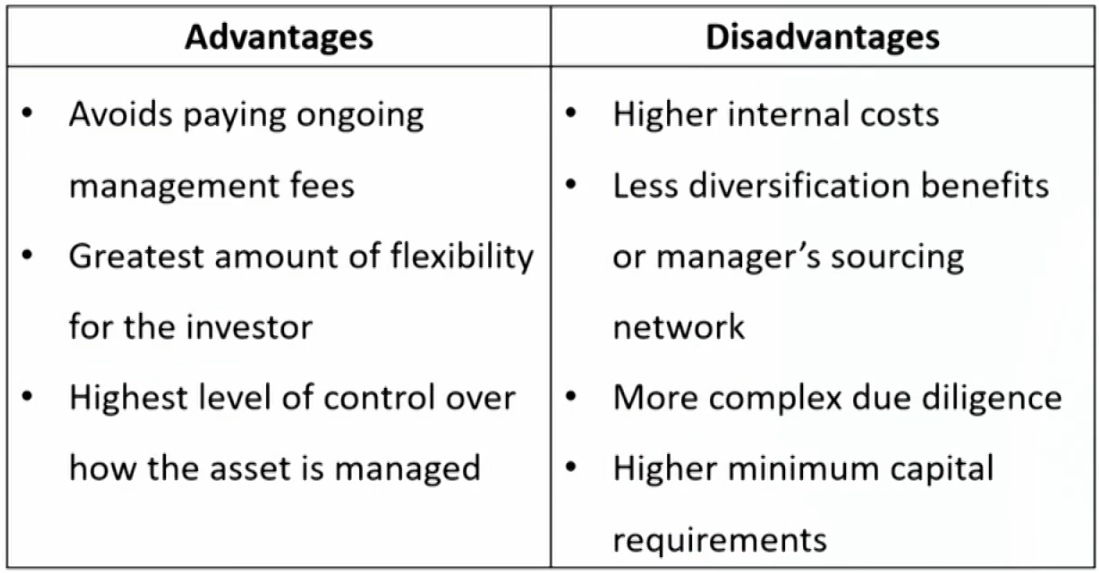

- Direct investing自己直接投:An investor makes a direct investment in an asse without the use of an intermediary.

- Great flexibility and control when it comes to choosing their investments, selecting their preferred methods of financing, and planning their approach.

- Typically reserved for larger and more sophisticated专业 investors.

Due diligence of three methods

- Direct investing: the focus of the due diligence is the company itself, at a very detailed level.

- Fund investing: the investor is responsible for conducting due diligence on the fund manager.

- Co-investing: the investor will conduct direct due diligence on the portfolio company with the support of the manager.

Fund investing strucutre

- General partner(GP, manager): runs the fund and bears unlimited liability for anything that might go wrong.

- Limited partners (LP, investors): are outside investors who own a fractional interest in the partnership based on the amount of their initial investment.

- Play passive roles and are not involved with the management of the fund.

- There exists a principal/agent problem between GP and LPs.

Key partnership documents

- Limited partnership agreements (LPAs)合伙协议

- A legal document that outlines the rules of the partnership and establishes the framework that ultimately guides the fund's operations.

- May be dense with provisions and clauses.

- Side letters

- Exist ouside the LPA.

- E.g. , notice requirements in the event of litigation.

Compensation and Fees

Compensation structures

- Management fee

- Also known as base fee.

- Typically ranging from 1% to 2% of AUM(hedge fund)交的钱 or committed capital (PE fund)承诺交的钱.

- Performance fee

- calculated on profits net of management fees基础是管理费外 or on profits independent of management fees基础包括管理费

- Also known as incentive fee or carried interest.

- Typically 20% of excess returns

- Hurdle rate超过约定回报率才有激励费: a return level that LPs must receive before GP begin to receive incentive fees.

- Hard hurdle rate超过门槛的部分: the GP earns fees on annual returns in excess of the hurdle rate.

- Soft hurdle rate超过之前的部分: the fee is calculated on the entire annual gross return as long as the set hurdle is exceeded.

Usually has a catch-up provision.

- High water mark水位不断上升: reflects the highest value used to calculate an incentive fee.

- The incentive fees are only paid when assets under management are above the highest value (net of fees) previously recorded.

- Protects clients from paying twice for the same performance.

- Waterfall of PE: a provision that specifies how distributions from a fund will be split and how the payouts will be prioritized.如何给不同类别的合伙人分钱

- Deal-by-deal (or American) waterfalls: performance fees are collected on a per-deal basis每完成应该项目就分配一次. GPs get paid before LPs receive their initial investment on the entire fund.利好GP

- Whole-of-fund (or European) waterfalls: GP does not participate in any profits until the LPs receive their initial investment and the hurdle rate has been met.LP拿够后才到GP,利好LP

- Clawback provision of PE: right of LPs to reclaim overdistributed performance fee.利好LP

- Are usually activated when a GP exits successful deals early on but incurs losses on deals later in the fund's life.即使不再是GP合伙人,也要为任期内错误决策付出代价,归还酬金给LP

- Is only as good as the creditworthiness of the GP.

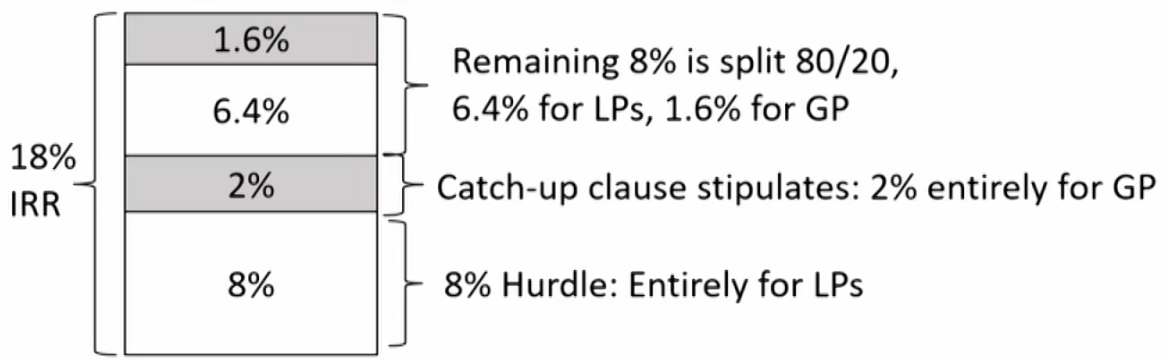

- Catch-up clause of PE: allows fund managers to earn incentive fee on all profits, given hurdle rate has been achieved.利好GP

- Profits are distributed only to the limited partners until the hurdle rate is reached.超过hard hurdle rate部分优先全给GP,直到与hard hurdle rate下的收益达到约定百分比,之后就按百分比分成

- Additional profits are split, with 100% going to the fund manager until the fund manager receives an incentive fee on all of the profits.

Custom fee arrangements

- “2 and 20” and “1 and 10” are common, but variations exist.

- Fees based on liquidity terms and asset size.

- Longer lockups are generally associated with lower fees.锁定期长的手续费低

- Discount fees for larger investors or for placement agents.

- Founders' shares entitle investors to a lower fee structure.越早投入手续费越低

- Either/or fees: managers agree either to charge a 1% management fee or to receive a 30% incentive fee above the hurdle, whichever is greater.管理费和激励费只受高的

Different Alternative Investments

Hedge funds对冲基金

Characteristics of hedge funds

- Private placement offering

- Limited number of investors and large initial investments.

- Lighter regulatory compliance burden

- Light investment restrictions

- Creatively selects investments in different geographic regions

- Leverage is often used

- Generally takes both long and short positions

- Generate high returns (absolute or risk adjusted basis)

- Management fees and incentive fees

- Lockup periods: Investors may be required to keep their money in the hedge fund for a certain period before they are allowed to redeem shares.

- Soft lockup: an expensive redemption fee is charged.

- Notice periods: investors may be required to give notice,typically 30-90 days, of their intent to redeem.赎回要提前通知

- The goal of hedge fund redemption restrictions is typically to increase hedge fund manager flexibility.

Categories of hedge funds

- Hedge funds are typically classified by strategy.

- Equity hedge strategies

- Event-driven strategies

- Relative value strategies

- Macro strategies

- Hedge fund categorization is important to allow investors to review aggregate performance data, select strategies, and select appropriate performance benchmarks.

Forms of hedge fund investments

- Individual hedge fund

- Extensive due diligence, high minimum invesmtnet.

- Funds of hedge funds母基金

- Diversification

- Able to negotiate better redemption terms

- Making hedge funds accessible to smaller investors

- Expertise in conducting due diligence on hedge funds尽职调查简单

- Drawbacks: more complex(higher) fees structures

Risk and return of hedge fund investments

- Self-reporting and survivorship bias

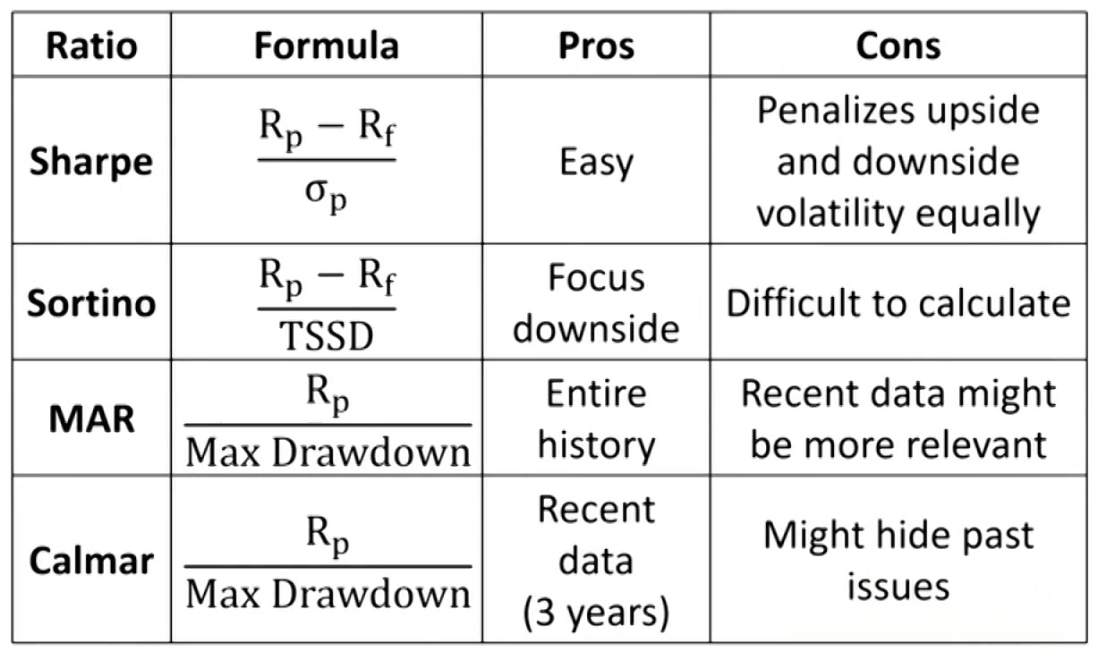

- Higher returns and lower volatility. → Higher Sharpe ratio.

- Asymmetric distribution of returns

- Higher downside deviation. → Lower Sortino ratio

- Drawdown: cumulative negative returns in a certain period.

- Risk diversification properties

- First came to prominence with the dot-com bubble.

- Expanded it further through direct allocations after 2008.

- Using market prices or quotes for valuation

- Common approach: the average quote, (bid + ask) / 2平均计价

- Conservative approach: bid prices for long position and ask prices for short position最差情况计价

- Valuation in highly illiquid or non-traded investments缺少流动性导致的偏差

- "Mark-to-model" basis模型不准确

- Returns maybe smoothed or overstated价格被平滑

- Volatility of returns understated低估波动性

Equity hedge strategies权益对冲策略

- Focus on public equity markets and take long and short positions in equity and equity derivative securities.

- Generally use a "bottom-up" security-specific approach.

- Main types:

- Market neutral对冲风险

- Fundamental L/S growth成长性基本面分析

- Fundamental value价值基本面分析

- Short biased做空有问题的公司

- Sector specific

- Market neutral

- Long positions in undervalued securities and short positions in overvalued securities.

- Maintains a net position that is neutral with respect to market risk and other risk factors (size, value, industry, etc).

Portfolio beta is close to zero. - Require the application of leverage.

- Are generally stable, low-return portfolios but are exposed to occasional spurts of volatility.

- Fundamental L/S growth

- Use fundamental analysis to identify companies expected to exhibit high growth and capital appreciation.

- Take long positions in these companies while short companies under downward pressure.

- Portfolios tend to end up long biased.

- Fundamental value

- Use fundamental analysis to identify companies deemed undervalued.

- Takes long positions in these companies and sometimes hedges the portfolio by shorting index ETFs or more growth- oriented companies deemed overvalued.

- Portfolios tend to end up long biased, value biased, and small-cap biased.

- Short biased

- Focus on shorting overvalued equity securities (against limited or no long-side exposures).

- Can be useful in terms of weathering periods of market stress.

- Have a difficult time overall posting meaningful long-term returns.

- Sector specific

- Exploit manager expertise in a particular sector and use quantitative (technical) and fundamental analysis to identify opportunities.

- The more complex a sector or the more opaqueness in accounting practices, the more value sector-specific managers bring.

Event-driven strategies事件驱动策略

- Event-driven strategies seek to profit from defined catalyst events, such as an acquisition or restructuring.

- Is based on bottom-up security-specific analysis.

- Tend to be long biased.

- Main types:

- Merger arbitrage购买要合并的公司

- Distressed/restructuring认为有利好事件

- Special situations有标志性事件

- Activist成为股东控制公司

- Merger arbitrage

- Long the stock of the company being acquired and short the stock of the acquiring company when the merger or acquisition is announced

- The primary risk in merger arbitrage is that the announced combination fails to occur and the deal spread re-widens to pre-merger levels.

- Moderate expected return → application of leverage.

- Distressed/restructuring

- Focus on securities of companies either in or perceived to be near bankruptcy.

- Purchase fixed-income securities trading at a significant discount to par.

- Or purchase the so-called fulcrum debt instrument expected to convert into new equity upon restructuring.

- Special situations

- Focus on opportunities to buy equity of companies engaged in restructuring activities other than mergers, acquisitions,or bankruptcy.

- Activist

- Secure sufficient equity holdings to allow them to influence corporate policies or direction.

- Try to create business catalysts, moving the investment towards a desired outcome

Relative value strategies相对价值策略

- Seek to profit from a pricing discrepancy between related securities based on an unusual short-term relationship,expecting the discrepancy will be resolved over time.

- Main types

- Convertible bond arbitrage

- Fixed income

- Volatility

- Multi-strategy

- Convertible bond arbitrage

- A market-neutral investment strategy seeks to exploit a perceived mispricing between a convertible bond and its component parts.

- The classic convertible bond arbitrage trade is to purchase a convertible bond that is believed to be undervalued and to hedge its risk using a short position in the underlying equity.

- Fixed income(general)

- Focus on the relative value within the fixed-income markets,with an emphasis on sovereign debt and sometimes the relative pricing of investment-grade corporate debt.

- Strategies may incorporate long-short trades between two different issuers, between corporate and government issuers, between different parts of the same issuer's capital structure, or between different parts of an issuer's yield curve.

- Fixed income (high yield)

- Focus on the relative value of various higher-yielding securities, including ABS, MBS, and high-yield loans and bonds

- Opaque mark-to-market pricing and illiquidity issues are significant considerations.

- Volatility

- Typically use options to go long or short market volatility.

- A short-volatility strategy involves selling options to earn the premiums and benefit from calm markets.

It can experience significant losses during unexpected periods of market stress. - A long-volatility strategy tends to suffer the cost of small premiums in anticipation of larger market moves.

- Multi-strategy

- Trade relative value within and across asset classes or instruments.

Looks for any available investment opportunities. - The goal is to initially deploy (and later redeploy) capital efficiently and quickly across various strategy areas as conditions change.

- Trade relative value within and across asset classes or instruments.

Macro and CTA strategies宏观策略

- Macro strategies

- Emphasize a top-down approach to identify economic trends.

- Use long and short positions to profit from a view on overall market direction because it is influenced by major economic trends and events.

- Generally benefit most from periods of higher volatility.

- Managed futures funds (Commodity trading advisers, CTA)

- Making diversified directional investments primarily in the futures markets on the basis of technical and fundamental strategies.

- May include investments in a variety of futures, including commodities, equities, fixed income, and foreign exchange.

Diversification benefits has diminished. - Mean-reverting markets is unfavorable.

Private capital私募

Overview of private capital

- Private capital is the broad term for funding provided to companies that is sourced neither from the public markets,nor from traditional institutional providers.

- Comprising private equity私募股权投资 and private debt私募债权投资.

- Comprising private equity私募股权投资 and private debt私募债权投资.

Diversification benefits of private capital

- Investments in private capital funds can add a moderate diversification benefit to a portfolio of publicly traded stocks and bonds.

- Correlations with public market indexes vary from 0.47 to 0.75.

- Private equity investments may offer vintage diversification.

- Private debt investments, which offer more options than bonds can also serve diversification goals.

Categories of Private Equity Invests私募股权投资

- Private equity (PE): investment in privately owned companies or in public companies with the intent to take them private.投资私有公司或者最终使其私有化

- Portfolio companies: the companies owned by private equity funds.

- Primary private equity strategies

- Certainty around valuation increases as the portfolio company matures and moves into later-stage financing.对于不同时期的公司采用不同手段

- Certainty around valuation increases as the portfolio company matures and moves into later-stage financing.对于不同时期的公司采用不同手段

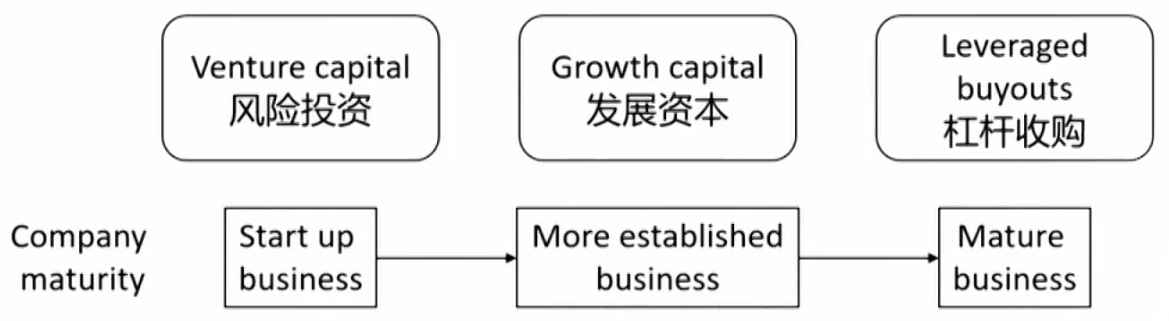

Venture capital

- Venture capital(VC) entails investing in or providing financing to private companies with high growth potential.对成长公司提供风险投资

- Typically start-ups or young companies.

- Higher expected returns with higher risks

- Venture capitalists are active investors directly involved with their portfolio companies.

- May also provide financing in the form of debt (commonly,convertible debt).

- Formative stage

- Pre-seed capital, or angel investing, is capital provided at the idea stage对idea投资. The amount of financing at this stage is typically small and sourced from friends and family.

- Seed stage generally supports product development and marketing efforts. The first stage at which VC funds invest.验证可行性

- Early stage, or start-up stage financing goes to companies moving toward operation but before commercial production and sales.开始少量生产

- Later stage financing(expansion VC) is provided after commercial production and sales have begun but before an IPO takes place.开始量产,准备上市

Support initial growth, a major expansion, product improvements, or a major marketing campaign.

Management selling control of the company to VC. - Mezzanine stage financing is provided to prepare to go public.上市准备时期

It represents the bridge financing.

Growth capital

- Growth capital: the firm takes a less-than-controlling interest in more mature companies looking for capital to expand or restructure operations, enter new markets, or finance major acquisitions.

- A.k.a. growth equity or minority equity investing.

Leveraged Buyouts

- Leveraged Buyouts arise when private equity firms establish buyout funds to acquire public companies or established private companies, with a significant percentage of the purchase price financed through debt.

- The target company's assets typically serve as collateral for the debt, and the target company's cash flows are expected to be sufficient to service the debt.

- A highly leveraged transaction.

- Tpyes of LBO

- Management buyouts(管理层收购): the current management team is involved in the acquisition.

- Management buy-ins(管理层换购): an external management team acquires a company and replaces the existing management team.

- The returns of LBO depend greatly on the use of leverage

- LBO investments enjoy more certainty than VC investments.

Exit Strategies

- Trade sale: the sale of a company to a strategic buyer, such as a competitor.股票卖给战略投资者或竞争者

- Pros: immediate cash, higher price (synergies), fast and simple, lower costs and transparency than IPO.

- Cons: possible management opposition, limited potential buyers, lower attractiveness to employees.

- Initial public offering (IPO): the portfolio company sells its shares to public investors.通过上市盈利

- Pros: highest price, management approval, publicity, futur upside potential.潜在收益最大

- Cons: higher cost, long lead times, market risk, disclosure requirements, a potential lockup period, IPOthreshold.

- Special purpose acquisition company(SPAC): a shell company via an IPO through which sponsors raise a blind pool of cash aimed for merger or acquisition with private firms.

- Pros: extended time for disclosure, lower volatility of share pricing, flexibiltiy, high-profile and seasoned sponsors.

- Cons: capital risk due to potential redemptions, stockholder overhang after merger, spread between the announced and true equity value because of the dilution.

- Recapitalization: a company issues debt to fund a dividend distribution to equity holders.发行债券以特别红利的形式发给自己

- Not a true exit strategy.

- Secondary sales: sale to another PE or other investors.股票卖给下一家PE或投资者

- Write-off/Liquidation: liquidates the portfolio company before moving on to other projects.破产清算

Risk and return of private equity

- Investors require a higher return for accepting the higher risk,including illiquidity and leverage risks.

- Private equity return indexes rely on self-reporting and are subject to survivorship bias, backfill bias数据是他们说的,不一定准

- This typically leads to an overstatement of returns.投资数据不客观

- Failure to mark to market will understate measures of volatility and correlations with other investments.低估波动性和相关系数

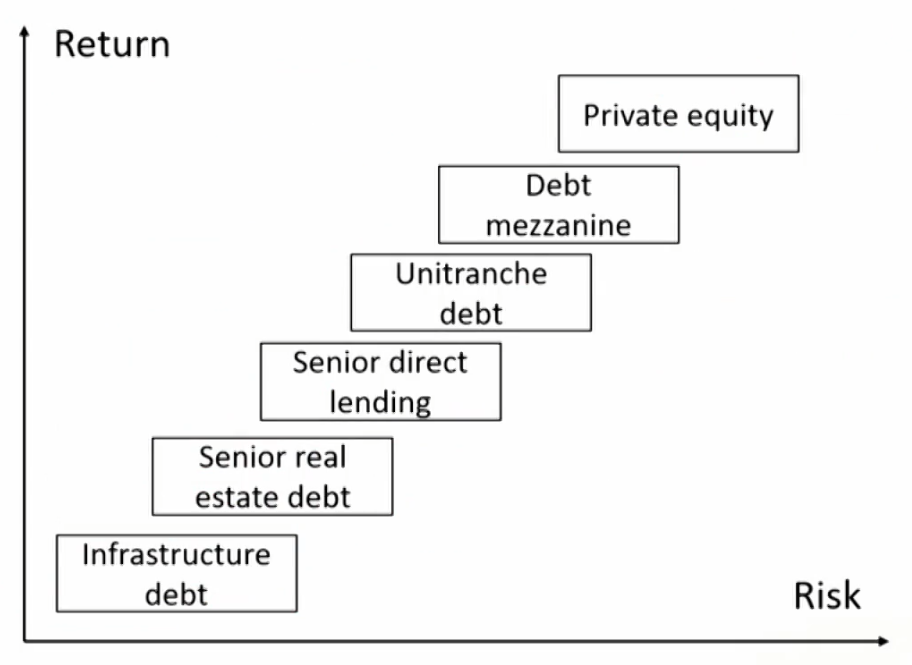

Categories of private debt私募债权投资

- Direct lending放贷给对方

- Providing capital directly to borrowers.

- Smaller number of investors than traditioanl debt.

- Usually higher interest rates to mid-market companies.

- Venture debt放贷给初创企业

- Provided to start-up or early-stage companies that may be generating little or negative cash flow.

- Lack of substantial assets for pledging as debt collateral.

- Mezzanine debt风险最高的债权投资,仅次于股权投资

- Private debt that is subordinated to senior secured debt but is senior to equity in the borrower's capital structure.

- Investors commonly demand higher interest rates and may require options for equity participation.

- Distressed debt放贷给困境中的企业

- Buying the debt of mature companies with financial difficulty expecting companies may restructure and revive.

- Collateralized loan obligations (CLO)

- It pools several loans and then divides that pool into various tranches.

- Unitranche debt单一层级债

- consists of a hybrid or blended loan structure combining different tranches of secured and unsecured debt into a single loan with a single, blended interest rate.

- Real estate debt or infrastructure debt放贷给公司做基础设施建设

- Specialty loans

Risk and return of private debt

- Investors in private debt could realize higher returns from the illiquidity premium.

- Overall, investing in private debt is riskier than investing in traditional bonds.

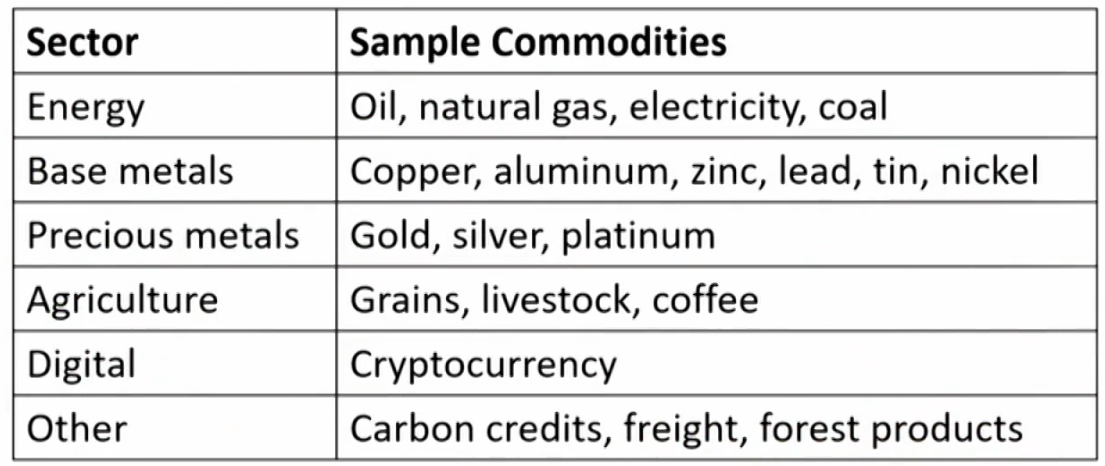

Commodities大宗商品

Characteristics of commodities

- Investment returns are based on changes in price rather than income stream such as interest, dividends or rent.收益主要来源于价差,不是票息类

- Holding physical commodities incurs transportation and storage costs.

- Trading in physical commodities is primarily limited to a smaller group of entities in the physical supply chain.

- Most commodity investors do not trade actual physical commodities but, rather, trade commodity derivatives.主要使用衍生工具

- The relative importance, amount, and price of individual commodities evolve with society's preferences and needs.

Forms of Commodity Investments

- Direct investment

- Derivatives

- Exchange-traded products(ETPs, either funds or notes)

- Commodity Trading Advisors (CTAs)

- Funds specializing in specific commodity sectors

Characteristics of commodities investment

- Benefit of commodity investment

- Real hedge against inflation risk应对通货膨胀

- Effective for portfolio diversification because of low correlation with other investment returns与其它投资关联度低,适合加入组合分散化风险

- Risk of commodity investment

- Commodity spot prices are a function of supply and demand供给导致价格波动大

- Demand levels are influenced by global manufacturing dynamics and economic growth.需求变动大

- Producers cannot alter commodity supply quickly because extended lead times are needed to affect production levels.供给调整满,跟不上需求

Commodity index

- To be transparent, investable, and replicable, commodity indexes typically set their prices based on futures contracts rather than underlying commodities.

- Different commodity indexes are composed of different commodities and index weights.

- Overall, low correlation with other asset classes.

- Effective for portfolio diversification

Commodity futures pricing

- Futures price ≈ FV of Spot price + FV of Storage costs - FV of Convenience yield

- Commodity futures price often do not adhere to a strict cost-of-carry relationship.

- Commodity futures price often do not adhere to a strict cost-of-carry relationship.

- Futures prices may be different from spot prices

- Contango: futures prices are higher than the spot price, the commodity forward curve is upward sloping.期货价格大于现货价格

Occurs when there is little or no convenience yield. - Backwardation: futures prices are lower than the spot price,the commodity forward curve is downward sloping现货价格大于期货价格

Occurs when the convenience yield is high.

- Contango: futures prices are higher than the spot price, the commodity forward curve is upward sloping.期货价格大于现货价格

Timberland and farmland林地农地

Characteristics of timberland and farmland

- Timberland

- Typically trading in larger units of land.体量大

- Flexibility: harvesting more trees when timber prices are up and delaying harvests when prices are down.灵活度更大,想砍就砍

- Return driver: biological growth; changes in spot prices and futures prices of cut wood; changes in the price of the underlying land.

- Farmland

- Typically trading in much smaller sizes体量小

- Provide a hedge against inflation.对抗通胀

- Little flexibility: farm products must be harvested when ripe.灵活度低,受农时影响

- Return driver: harvest quantities; commodity prices (e.g.,the price of corn); and land price changes.

Risk of farmland investment

- Value comes not just from the harvest but also from the offset to human activity比如失火.

2. Low liquidity买卖流动性差 - High risk of negative cash flow because fixed costs are relatively high(the land must be cared for and crops need fertilizer, seed, and so on)初期投资大,现金回笼慢

- Revenue is highly variable based on the weather.价格受天气影响大

- World trade and growing foreign agricultural competition result in declines of crop prices受国际贸易影响

Real Estate房地产

Categories

- Owner-occupied market

- Residential: single-family homes and multi-family units.

- Commercial: office buildings, retail shopping centers, and warehouses.

- Rental properties

- Lease contract: landlord/lessor and tenant/lessee

- Title/deed represents real estate property ownership covering building and land-use rights.

Forms of real estate investment

Characteristics of Real Estate

- Benifit

- Income generation and capital appreciation可以卖也可以收租

- Fixed rents may lessen cash flow impact放贷现金流稳定

- Diversification benefits和其他投资相关性低

- Inflation hedge if rents can be adjusted quickly for inflation.应对通货膨胀

- Risks

- Property value risk价格受经济影响

- Managment risk

- Construction delays and cost overruns建造花费时间,超预算

- Leverage risk高杠杆

Especially with higher loan-to-value ratio

Real estate index

- Appraisal index评估指数,砖家各抒己见

- Subjective, understate volatility主观,低估波动性

- Repeat sales (transaction-based) index基于交易数据

- Sample selection bias和样本选择有关

- REIT index信托基金指数

- Use the prices of publicly traded shares of REITs to construct the indices

- More frequently traded, more reliable is the index有活跃交易

Differences with other asset classes

- Large required capital investment → difficult too diversified

- Transaction costs are high → Illiquidity

- Diversity, as no two properties are identical

- Necessarily fixed location

- Price discovery in the private market is opaque

- Transaction activity may be limited in certain markets

- No investable index

- Typically requires professional operational management

Direct real estate investing

- Direct private investing involves purchasing a property and originating debt for one's own account.

- Advantages: control, taxes.

- Disadvantage: extensive time required to manage, need for local market expertise, large capital requirements,concentrated position.

- Many investors prefer to hire advisers or managers to manage the their direct real estate investment in a separate account.

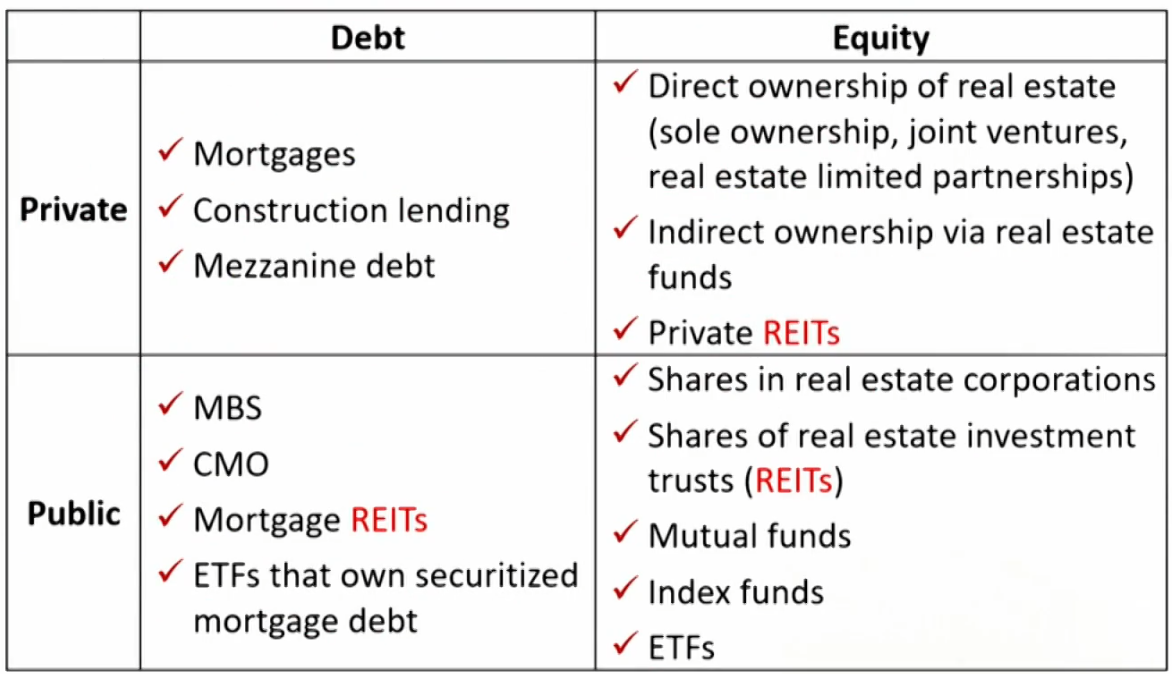

Indirect realestate investing

- Indirect investing provides access to the underlying real estate assets through a variety of pooled investment vehicles.

- Intermediaries facilitate the raising and pooling of capital and the creation of investable structures.

- Types of indirect real estate investing

- Mortgages: whole loans or MBS.

- Private fund investing

- REITs

Private fund investing

- Most private real estate funds are structured as infinite-life open-end funds.

- Core real estate strategies: characterized by well-leased,high-quality institutional real estate in the best markets.

- Core-plus strategies will also accept slightly higher risks derived from non-core markets.

- Finite-life closed-end funds are more commonly used to seek higher returns.

- Value-add investments may require modest redevelopment or upgrades, the leasing of vacant space, or repositioning the underlying properties to earn a higher return.

- Opportunistic investing accepts the much higher risks of development, major redevelopment, repurposing of assets,taking on large vacancies, and speculating on significant improvement in market conditions.

Real estate investment trusts (REITs)

- REITs are tax-advantaged entities that own, operate, and develop income-producing real estate property.

- Are not taxed at the corporate level.

Above 90% of taxable net rental income are distributed. - Most REITs are listed on stock exchanges.

Greater liquidity, lower trading costs, and better transparency.

- Are not taxed at the corporate level.

- Mortgage RElTs v.s.Equity RElTs

Infrastructure基础设施

Overview

- The assets are capital intensive大资本 and long lived收寿命长 for public use.

- Increasing use of public-private partnerships(PPPs)民间出大头: long- term contractual relationship between the public sector and the private sector.

- Investors may lease the assets back to the government, sell newly constructed assets to the government, or hold and operate the assets

Characteristics

- Strategically important战略性

- Monopolistic and regulated垄断性

- Stable long-term cash flows现金流稳定

- Significant capital investment初期投入大

- Long operational lives使用寿命长

- Defined risks风险各异

- Highly leveraged financial structure高杠杆

Categories by underlying assets

- Economic infrastructure assets support economic activity.

- Transportation assets高速、飞机场等

- Information and communication technology(ICT) assets基站等

- Utility and energy assets能源

- Social infrastructure assets are directed toward human activities.

- Educational, health care, social housing, and correctional facilities.

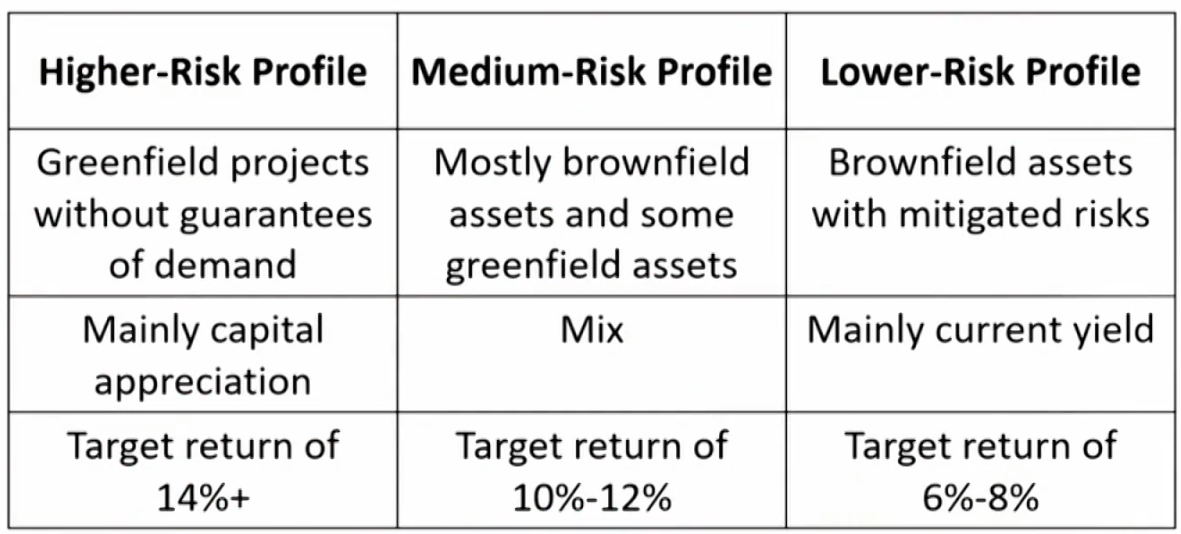

Categories by Stage of development

- Brownfield investment: investing in existing infrastructure assets.已经建了一部分

- Privatize or lease out government assets, sell and lease back.

- Less risky with lower expected return.

- predictable cash flows

- Greenfield investment: investing in infrastructure assets that are to be constructed.从零开始,要先除草

- Lease or sell to the government or to hold and operate.

- More risky with higher expected return.

Forms of Infrastructure Investments

- Direct investment

- Provides control and the opportunity to capture full value.

- Large investment, concentration and liquidity risks.

- Indirect investment

- Funds, ETFs, company shares

- Master Limited Partnerships (MLPs) trade on exchanges and are similar to REITs.

Generally distribute most free cash flow to their investors

Risk of infrastructure

- Demand risk → take-or-pay arrangements

- Operational risk → reputable and experienced operators

- Construction risk → fixed-price date-certain contracts

- Financial risk → derivatives

- Regulatory risk → clear PPP agreement or due diligence

- Political risk → political risk insurance

- Currency risk → adjustment mechanisms

- Tax/profit repatriation risks → adjustment mechanisms

Return of infrastructure

1.Returns depend on investment type.

Performance Calculation and Appraisal of Alternative Investments

Issues in Performance Appraisal

Challenges of performance appraisal

- Limited transparency

- Low portfolio liquidity

- High leverage and use of derivatives

- High product complexity

- Mark-to-market issues, especially for specialized products

- Limited redemption availability

- Difficulty in manager selection and diversification

- High fees, which can have a non-trivial impact on performance

Common approaches to performance appraisal

PE and real estate performance evaluation

- Private equity and real estate involve large initial capital outlays with capital inflows occurring much later in the investment cycle.

- Net cash position shows J-curve effect.

- Shorter-term risk metrics are highly inappropriate.

- As a general rule, the best way to evaluate such investments is the IRR of the respective cash flows.

- Multiple of invested capital (MOIC)/money multiple

- MOIC =(Realized value of investment + Unrealized value of investment)/(Total amount of invested capital)。

- Quartile ranking depicts manager's performance against a cohort of peer investment vehicles constructed with similar investment attributes and vintage year.

- Cap rate: the net operating income divided by the market valuel of the property.

Hedge fund performance evaluation

- Leverage has the effect of magnifying gains and losses.

- Hedge funds leverage their portfolios by using derivatives or borrowing capital from prime brokers.

- The hedge fund deposits cash or other collateral into a margin account with the prime broker.

- An inability to meet margin calls can force the hedge fund to liquidate the losing position, leadign to further losses.

- Illiquidity (Mark to market problem)

- Little chance of liquidating all the shares at quoted price.

- Funds may differ in which price or quote they use.

A more conservative and accurate approach is to use bid prices for long positions and ask prices for short positions. - Highly illiquid or even non-traded investments may have no reliable market values, it becomes necessary to estimate values. (Mark to model valuation)

- Investor redemptions may require the hedge fund manager to liquidate some positions at disadvantageous prices, while also incurring transaction costs.

- Ability to demand a long lockup depends on reputation.

- Ideally, redemption terms should be designed to match the expected liquidity of the assets being invested in.

- Funds of hedge funds may offer more redemption flexibility.