Physical asset: Soft commodity农产品等, Hard commodity能源、金属等;

Other: interest rate, credit, weather, longevity, other derivatives, etc.

Derivative usually transform (not simply pass through) the performance of the underlying asset before paying it out in the derivatives transaction.

A derivative contract is a legal agreement between counterparties with a specific maturity.

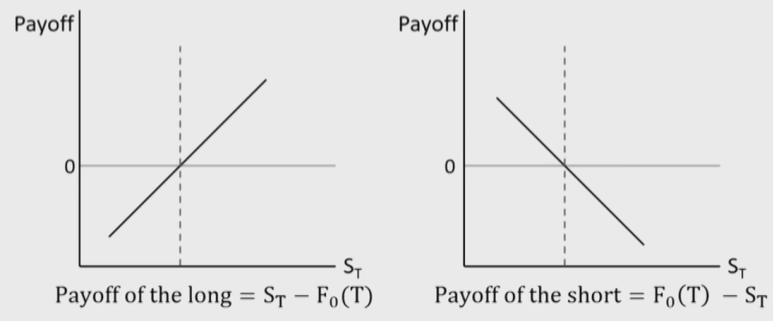

The long: buyer, holder

The short: seller, writer

Forward commitment远期协议,双务合约: Forward, futures, and swap都是义务方

Contracts entered into at one point in time that require both parties to engage in a transaction at a later point in time (the expiration) on terms agreed upon at the start.

Contingent claim或有索求权: Option一方义务一方权利

Derivatives in which the outcome or payoff is dependent on the outcome or payoff of an underlying asset.

Derivative markets expand the set of opportunities available to market participants.

Benefit from a decline in the value of the underlying.

Portfolio diversification.

Offset the financial market exposure. (Hedge)

Create large exposures with a relatively small cash outlay.

Derivatives typically have lower transaction costs and are often more liquid.

Purpose of Issuer

Issuers, investors, and financial intermediaries use derivative instruments to meet their financial objectives.

Non-financial corporate issuers often hedge risks to their assets,liabilities, and earnings.套期保值

Cash flow hedges.应对未来现金流的不确定性

Fair value hedge.应对产品未来价格波动

Net investment hedges.应对汇率波动

Any derivative purchased or sold must be marked to market through the income statement via earnings.

Unless it is embedded in an asset or liability or qualifies for hedge accounting.

In order to qualify for this treatment, the features of a derivative must closely match those of the underlying transaction.

OTC derivatives are preferred.

Purpose of Investor

Investors use derivatives to replicate a cash market strategy,hedge a fund's value against adverse movements in underlyings,or modify or add exposures.改变风险敞口

Less focused than issuers on hedge accounting treatment.

Exchange-traded derivatives are more frequently used.

Forward Commitment and Contingent Claim Features and Instruments

Forward

An over-the-counter derivative contract in which two parties agree that one party, the buyer, will purchase an underlying asset from the other party, the seller, at a later date at a fixed price they agree on when the contract is signed.

In addition to the (forward) price, the two parties also agree on several other matters, such as the identity and the quantity of the underlying.

The long hopes the price of the underlying will rise above the forward price, Fo(T), whereas the short hopes the price of the underlying will fall below the forward price.

Forward contracts can be settled in two ways:

Delivery of the underlying asset实物交割

Exchange of cash现金结算: non-deliverable forwards(NDFs), cash-settled forwards, or contracts for differences

Forward contracts can be structured to create a perfect hedge,providing an assurance that the underlying asset can be bought or sold at a price known when the contract is initiated.

Dealer: a dealer creates a derivative contract and will quote a price to take a long or short position;

A.k.a market maker or financial intermediary.

End user: an end user is typically a corporation or institution seeking to transfer an existing risk.

Equity index forward股指期货

An equity index contract payoff is the notional amount times the percentage difference between the forward index and the actual index value at settlement

Futures

Futures

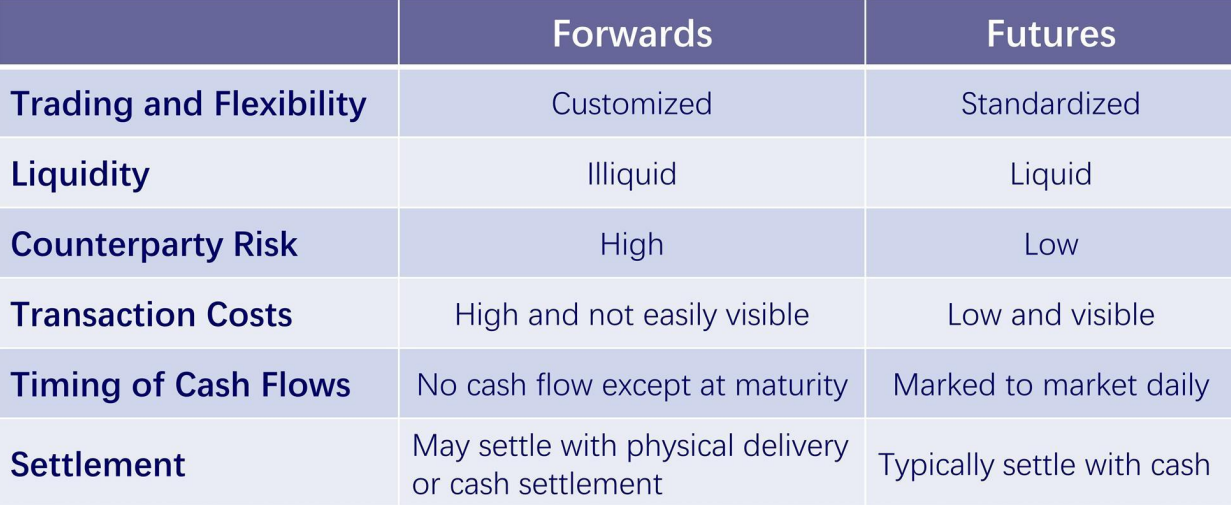

Futures contracts are specialized forward contracts that have been standardized and trade on a futures exchange.

Futures contracts have specific underlying assets, times to expiration, delivery and settlement conditions, and quantities.

The exchange offers a facility in the form of a physical location and/or an electronic system as well as liquidity provided by authorized market makers.

Futures price: the agree-upon price, like forward price.

Price limit: a provision limiting price changes, establish a band relative to the previous day's settlement price, within which all trades must occur.有涨跌停

Limit up/limit down: trading stops if trading price is above/below the upper/lower band.

Locked limit: when market hits limits and trading stops.

Mark-to-market: daily settlement of gains and losses to margin account according to the settlement price.

Settlement price: an average of the final futures trades of the day.不是收盘价

Initial margin: both parties deposit a required minimum sum of money when the contract is initiated.

Maintenance margin: the amount of money that must maintain in the margin account after the trade is initiated.

Always significantly lower than the initial margin.

Margin call: a request to deposit enough funds to bring the margin account balance up to the initial margin.要追加到初始保证金

The amount required is referred to as variation margin.

There are significant differences between futures margin accounts and equity margin accounts:

A futures margin is simply an amount of money put into an account that covers possible future losses, and there is no formal loan created as in equity markets.

For equity margin account, an investor deposits part of the cost of the stock and borrows the remainder at a rate of interest.

Offset/close-out平仓: a party re-enters the market at a later date but before expiration and engages in the opposite transaction

Open interest合约数量: the number of outstanding contracts at any given time.

Each contract counted in the open interest has a long and a corresponding short.

Forward vs. Futures

Forward contracts realize the full gain or loss at expiration,whereas futures contracts realize the gain or loss in parts on a day-to-day basis.

The time value of money makes these not equivalent, but the differences tend to be small.

In forward contract, with the entire payoff made at expiration, a loss by one party can be large enough to trigger a default.

Swap

Swap

An over-the-counter derivative contract in which two parties agree to exchange a series of cash flows whereby one party pays a variable series that will be determined by an underlying asset or rate and the other party pays either (1) a variable series determined by a different underlying asset or rate or (2) a fixed series.

A swap is a series of (off-market期初价值不为0) forwards.总和才为0

Characteristics of swap contracts:

Custom instruments;

Not traded in any organized secondary market;

Largely unregulated;

Default risk is a concern;

Most participants are large institutions;

Private agreements;

Difficult to alter or terminate.

Interest rate swap

Fixed for floating (plain vanilla)

Floating for floating

Equity swap

Currency swap

Plain Vanilla interest rate swap

Notional amount is not exchanged at the beginning or end of the swap (both loans are in same currency and amount);

On settlement dates, interest payments are netted;

Only the difference is paid by the party owing the greater amount.

Floating rate payments are typically made in arrears使用上一期的利率.

Payment is made at end of period based on beginning-of-period market reference rate.

Option

A derivative contract in which one party, the buyer, pays a sum of money to the other party, the seller or writer, and receives the right to either buy or sell an underlying asset at a fixed price either on a specific expiration date or at any time prior to the expiration date.

An option is a right, but not an obligation.

Default in options is possible only from the short to the long.

Option premium: payment to seller from buyer

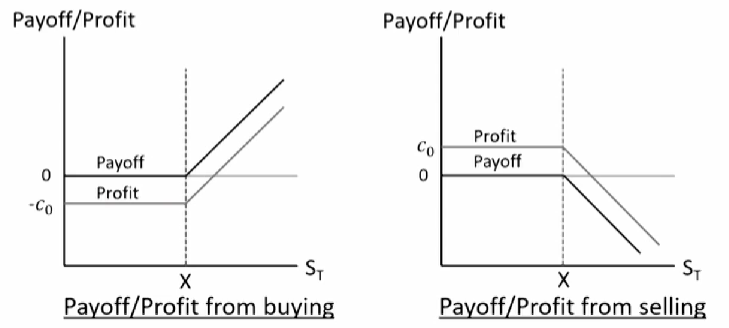

Call option: right to buy

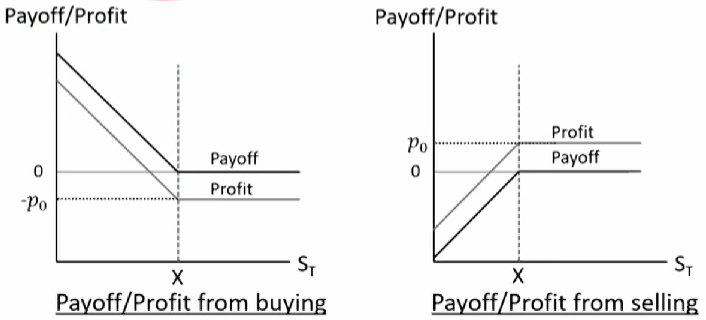

Put option: right to sell

Exercise price/strike price : the fixed price at which the underlying asset can be purchased

American option and European option

American option: exercisable at or prior to expiration

European option: exercisable only at expiration

无派息的call:提前行权会提早支付现金,最后持有资产,因此美式不会提前行权,此时欧式美式价格一样

有派息的call:派息足够大,能抵消提前支付现金的时间亏损时会提前行权,此时美式价格更大

put:提前行权会提早收到现金,最后持有资产,因此可能提前行权,此时美式价格更大

Moneyness (X: exercise price;S_t: spot price at timet)不考虑期权费

In the money赚钱

Call:S_t\gt X

Put:X\gt S_t

At the money S_t=X

Out of the money亏钱

Call:S_t\lt X

Put:X\lt S_t

Payoff不考虑期权费 \left(c_T\right) and profit考虑期权费 \left(\prod\right) from a call option at expiration

From buying: c_T=\operatorname{Max}\left(0, \mathrm{~S}_{\mathrm{T}}-\mathrm{X}\right) ; \Pi=\operatorname{Max}\left(0, \mathrm{~S}_{\mathrm{T}}-X\right)-c_0

From selling: -\mathrm{c}_{\mathrm{T}}=-\operatorname{Max}\left(0, \mathrm{~S}_{\mathrm{T}}-\mathrm{X}\right) ; \Pi=-\operatorname{Max}\left(0, \mathrm{~S}_{\mathrm{T}}-\mathrm{X}\right)+\mathrm{c}_0

Payoff \left(p_T\right) and profit \left(\prod\right) from a put option at expiration

From buying: \mathrm{p}_{\mathrm{T}}=\operatorname{Max}\left(0, X-S_{\mathrm{T}}\right) ; \Pi=\operatorname{Max}\left(0, X-S_{\mathrm{T}}\right)-\mathrm{p}_0

From selling: -\mathrm{p}_{\mathrm{T}}=-\operatorname{Max}\left(0, \mathrm{X}-\mathrm{S}_{\mathrm{T}}\right) ; \Pi=-\operatorname{Max}\left(0, \mathrm{X}-\mathrm{S}_{\mathrm{T}}\right)+\mathrm{p}_0

Credit Derivatives

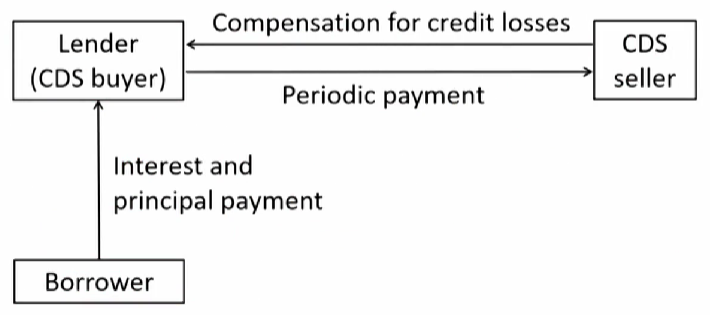

Credit default swap

Derivative contracts between two parties, a credit protection buyer and a credit protection seller, in which the latter provides protection to the former against a specific credit loss.

Credit default swap(CDS): the buyer makes a series of cash payments to the seller and receives a promise of compensation for credit losses resulting from the default of a third party.

CDS is essentially an insurance contract against default.

Other credit derivatives

Total return swap全收益互换

Credit-linked note(CLN)买bond+卖CDS

Credit spread option

Arbitrage, Replication and the cost of carry in Princing derivatives

Arbitrage

Law of one price: assets that produce identical future cash flows regardless of future events should have the same price.现金流相同的产品价格相同

Arbitrage is a type of transaction undertaken when two assets or portfolios produce identical results but sell for different prices.

Riskless with zero investment.

Trader will exploit the arbitrage opportunity quickly (buy low and sell high), then make the prices converge.

A derivative-related arbitrage opportunity arises when an asset with a known future price does not trade at the present value(PV) of its future price.

The appropriate discount rate is the risk-free rate.

4. No arbitrage pricing构造无风险资产组合,反求衍生品价格

Discount the expected payoff of the derivative at the risk-free rate

The price of a derivative can then be inferred from the characteristics of the underlying of the derivative, and the risk-free rate

Replication复制

A asset's cash flow stream may be recreated using a comination of other assets.

An asset and a hedging position of derivative on the asset can be combined to produce a position equivalent to a risk-free asset.

Asset - Derivative = Risk-free asset

Asset - Risk-free asset = Derivative

Derivative + Risk-free asset = Asset

Carring costs and carring benefits

Many assets have additional costs or benefits of ownership that must be reflected in the forward commitment price in order to prevent riskless arbitrage opportunities.

No arbitrage pricing

F_0(T)=\left[S_0-P V_0(I)+P V_0(C)\right](1+r)^T

F_0(T)=S_0e^{(r+c-i) T}

Opportunity cost (r)

Risk-free interest rate

Other costs of ownership(C, c)

Storage, transportation, insurance, and spoilage costs.

Benefits of ownership (I, i)

Dividend, interest, rent, convenience yield, etc.

Convenience yield: nonmonetary advantage of holding the asset

Foward vs. Spot price

Opportunity and Other Cost = Benefit

F(T) = S

Opportunity and Other Cost >Benefit

F(T) > S(Contango远期升水)

Opportunity and Other Cost < Benefit

F(T) < S(Backwardation远期贴水)

Pricing and Valuation of Forward Contracts and for an Underlying with Varying Maturities

Pricing and Valuation of Forward

Price of forward, futures, and swap

The fixed price or rate at which the underlying will be purchased at a later date.

Generally may not change as the (expected) price of the underlying asset changes.

Value of forward, futures, and swap

The difference of "with the position" from "without the position"

May increase or decrease as the (expected) price of the underlying asset changes.

At initiation

The forward contract at initiation has zero value.

Neither party to a forward transaction pays to enter the contract at initiation. V_0(T)=0

The forward price must be set so its value at initiation is zero.

In the financial world, we generally define value as the value to the long position.

At time t < T, the value of a forward contract is the spot price of the asset minus the present value of the forward price, and minus the net cost of carry.

Benefits will decrease forward price at initiation, and decrease the value of forward contract during its life.

Including dividend, interest, rent, convenience yield, etc.

Costs will increase forward price at initiation, and increase the value of forward contract during its life.

Including storage cost, maintenance cost, etc.

FRA

Forward contracts in which the underlying is an interest rate (e.g. MRR) are called forward rate agreements, or FRAs.

Long position借钱方 can be viewed as the obligation to take a (hypothetical) loan at the contract rate (i.e., borrow at the fixed rate); gains when reference rate increase.

Short position贷钱方 can be viewed as the obligation to make a (hypothetical) loan at the contract rate (i.e., lend at the contract rate); gains when reference rate decrease.

Lock the interest rate or hedge the risk of borrowing or lending at some future date.

One party will pay the other party the difference (based on notional value) between the interest rate specified in the FRA and the market interest rate at contract settlement.

The notation of FRA is typically "axb FRA"

a is the number of months until the contract expires

b is the number of months until the underlying loan is settled

FX forward contract: sale of one currency and purchase of the other on a future date at a forward exchange rate (F_{0,f/d}).

Long (short) position means purchasing (selling) the domestic currency and selling (purchasing) the foreign currency.

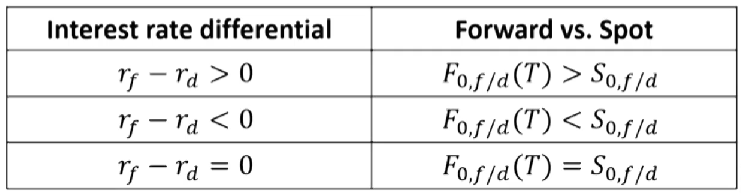

F_{0, f / d}(T)=S_{0, f / d} \times e^{\left(r_f-r_d\right) T}

r_f is the risk-free rate of the foreign currency

r_d is the risk-free rate of the domestic currency

The spot versus forward FX price relationship is determined by the risk-free interest rate differential.远期汇率变化取决于利率差

Valuation of FX forward

At any given time t, the MTM value of the Fx forward is the difference between the current spot FX price (S_{t,f/d}) and the present value of the forward price discounted by the current difference in risk-free rates \left(r_f-r_d\right) for the remaining period through maturity

V_t(T)=S_{t, f / d}-F_{0, f / d}(T) \times e^{-\left(r_f-r_d\right)(T-t)}

Pricing and Valuation of Futures Contracts

Pricing of Futures

Many of the pricing and valuation principles associated with forward commitments are common to both forward and futures contracts.

Futures realize the gain or loss in parts on a day-to-day basis,while forwards realize the full gain or loss at expiration

The forward contract price remains fixed until the contract matures.

Futures contract prices fluctuate daily based upon market changes.

The cumulative realized gain or loss is similar.

The time value of money makes these not equivalent.

Futures price will be higher than forward price when interest rate and futures price are positively correlated, and will be lower when they are negatively correlated.

A positive correlation between interest rate and futures price means that (for a long position) daily settlement provides funds (excess margin) when rates are high and they can earn more interest, and daily settlement requires funds (margin call) when rates are low and they only ask for less interest.

This is so called convexity bias.

Interest rate futures

Interest rate futures trade on a price basis

f_{A, B-A}=100-\left(100\times M R R_{A, B-A}\right)

f_{A, B-A} is the futures price for a market reference rate.

f_{3m,3m}=98 means M R R_{3m,3m}=2\%

This (100 - yield) price convention results in an inverse price/yield relationship.

A long futures position gains when reference rate decrease

A short futures position gains when reference rate increase

Futures contract basis point value(BPV)

BPV = Notional Principal x 0.01% x Period

Example: A futures contract for three-month MRR with a$1,000,000 notional principal

BPV =$1,000,000 x 0.01% x 90/360 =$25

Pricing and Valuation of Swap

Pricing and valuation of swap

As with forward contract, the price of a swap is the fixed price specified in the swap contract (the contract price) and the value depends on how expected future price change over time;

At initiation, a swap has zero value;

An increase in expected future price will produce a positive value for the fixed-price payer, and a decrease in expected future price will produce a negative value.

Pricing and valuation of swap

A swap is a series of forwards, each created at swap price.

The value of a swap equals the present value of all remaining future swap settlements.

Swap vs. forward

At initiation, the value of each one of the series forwards is not zero.

Off-market forward: forward contract created with a contract price that gives it a non-zero value at initiation.

A swap consist of some off-market forwards with positive present value and some off-market forwards with negative present values, so that the sum of their present values equals zero.

Interest rate swap

In a simple (plain vanilla) interest rate swap, one party pays a floating rate and the other pays a fixed rate on a notional principal amount.

An increase in expected future rate will increase the value for the fixed-rate payer, and vise versa.

At each payment date, a net payment is made from one party to the other.

For fixed rate payer: \text{Net payment}_t=(M R R_{t-1}-\text{Swap rate}) \times N P \times Period

An interest rate swap is equivalent to a series of (off-market)FRA, each with a forward rate equal to the swap fixed rate

The fixed-rate payer is equivalent to being long a floating-rate bond and short a fixed-rate bond

For fixed-rate payer (floating-rate receiver): V_t=P V_{\text {Floating-rate bond }}-PV_{\text {Fixed-rate bond }}

For fixed-rate receiver (floating-rate payer): V_t=P V_{\text {Fixed-rate bond }}-P V_{\text {Floating-rate bond }}

Due to better liquidity, active fixed-income portfolio managers often use swaps rather than underlying securities to adjust their interest rate exposure

An interest rate swap is equivalent to a series of (off-market)FRA, each with a forward rate equal to the swap fixed rate.

Different FRA fixed rates usually exist for different times to maturity.

Recall: \left(1+\mathrm{Z}_{\mathrm{B}}\right)^{\mathrm{B}}=\left(1+\mathrm{Z}_{\mathrm{A}}\right)^{\mathrm{A}} \times\left(1+I F R_{A, B-A}\right)^{\mathrm{B}-\mathrm{A}}

In contrast, a standard interest rate swap has a constant fixed rate over its life.

The swap rate should equates the present value of all future expected floating cash flows to the present value of fixed cash flows.

Moneyness refers to whether an option is in the money or out of the money:

If immediate exercise would generate a positive payoff, the option is in the money(ITM)

If immediate exercise would result in a loss (negative payoff),the option is out of the money(OTM).

If immediate exercise will generate neither a gain nor loss,the option is at the money (ATM).

Call option

In the money: S > X;

Out of the money: S < X;

At the money: S = X.

Put option

In the money: S < X;

Out of the money: S > X;

At the money: S = X.

Exercise value (intrinsic value)

The option contract's value if the option were exercisable at time t.立即行权的收益

The exercise value at time t incorporating the time value of money is the difference between the spot price (St) and the present value of the exercise price (PV(X)).

Long forward = long underlying + short risk free asset

Short forward = long risk free asset + short underlying

For option, exercise are uncertain.

Option replicating transaction should be adjusted for probability of exercise.

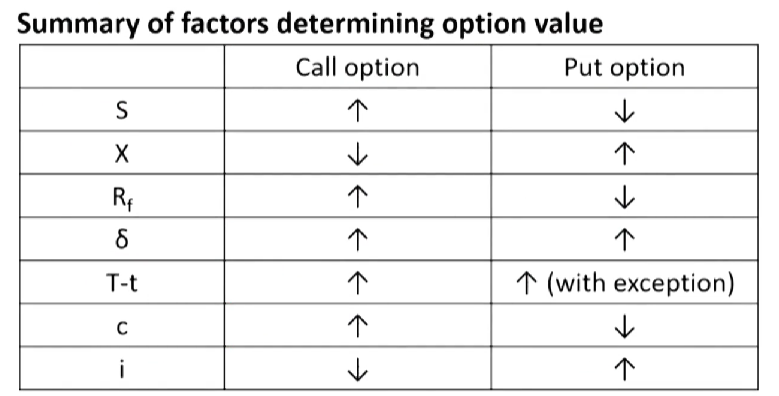

Factors that Determine Option Value

Price of the underlying asset (St)

For call option, a higher St will increase its value;

For put option, a higher St will decrease its value

The exercise price (X)

For call option, a higher X will decrease its value;

For put option, a higher X will increase its value.

The risk-free rate of interest (Rf)

For call option, a higher Rf will increase its value;

For put option, a higher Rf, will decrease its value.

Volatility of the underlying price (δ)

A higher δ will increase the value of both call and put options.

Time to expiration (T-t)

For call option and most put option, a longer(T-t) will increase the time value and then increase its value;

For some European put options, a longer (T-t) are more likely to decrease its value when:

The deeper a put option is in the money;股价只会上升

The higher the risk-free rate;不能提前行权取出钱投资

Costs (c) and benefits (i) of holding the asset

For call option, a higher cost (c) will increase its value and a higher benefit (i) will decrease its value;

For put option, a higher cost (c) will decrease its value and a higher benefit (i) will increase its value.

Reason: cost will generally increase the price of the underlying asset, and benefit will generally decrease the price of the underlying asset.

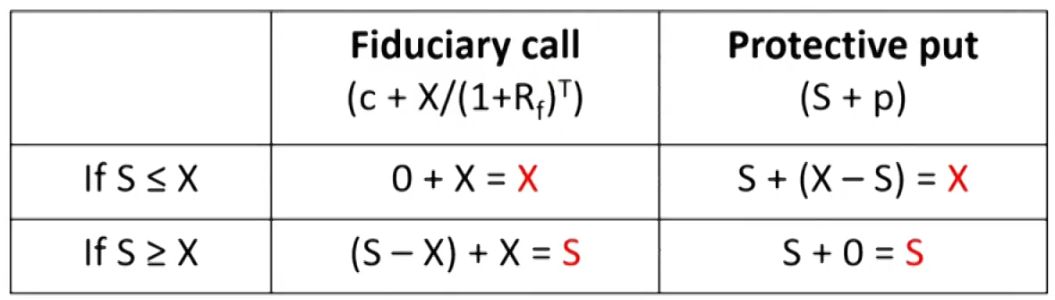

Combination of a European call option with exercise price of X and a pure-discount, riskless bond with face value of X.

Protective put (\mathbf{S}+\mathbf{p})

A share of stock together with a put option on the stock with exercise price of X.

Note: the call and put must be European-style (c, p) with same exercise price (X) and time to expiration (T). Also, the maturity of the bond should be the same (T).

Payoff at expiration

In either case, the payoff on a fiduciary call is the same as the payoff on a protective put, so:

If S_0+p_0\gt c_0+\mathrm{X} /\left(1+\mathrm{R}_{\mathrm{f}}\right)^{\mathrm{T}}

Selling the put and the underlying and purchasing the call and the risk-free asset at initiation.

If S_0+p_0\lt c_0+\mathrm{X} /\left(1+\mathrm{R}_{\mathrm{f}}\right)^{\mathrm{T}}

Purchasing the put and the underlying and selling the call and the risk-free asset at initiation.

Replication

The put-call parity can be rearranged to create synthetic equivalencies.

Synthetic call: c=S+p-X /\left(1+R_f\right)^T

Synthetic put: p=c+X /\left(1+R_f\right)^T-S

Synthetic stock: S=c+X /\left(1+R_f\right)^T-p

Synthetic bond: X /\left(1+R_f\right)^T=S+p-c

Put-call forward parity

Put-call-forward parity is derived with a forward contract (forward price:\mathrm{F}_0(\mathrm{~T})) rather than the underlying asset itself.

Substituting \mathrm{F}_0(\mathrm{~T}) /\left(1+\mathrm{R}_{\mathrm{f}}\right)^{\mathrm{T}} for \mathrm{S}_0 in put-call parity gives us the put-call-forward parity: \mathrm{F}_0(\mathrm{~T}) /\left(1+\mathrm{R}_{\mathrm{f}}\right)^{\mathrm{T}}+\mathrm{p}=\mathrm{c}+\mathrm{X} /\left(1+\mathrm{R}_{\mathrm{f}}\right)^{\mathrm{T}}

Or: \left[\mathrm{F}_0(\mathrm{~T})-\mathrm{X}\right] /\left(1+\mathrm{R}_{\mathrm{f}}\right)^{\mathrm{T}}=\mathrm{c}-\mathrm{p}

Option replication using put call parity

Put-call parity application

Put-call parity can be used to model the value of a firm's equity holder and debt holder.

The company defaults when the value of its assets falls below the default barrier (i.e., the liability).

It assumes limited liability and equity values are non-negative.

Equity option analogy: holding the company's equity is economically equivalent to owning a European call option on the company's assets (A) with strike price K and maturity T (maturity of debt) \mathrm{V}_{\text {risky debt }}=\mathrm{V}_{\text {risk-free debt }}-\mathrm{V}_{\text {put option }}

At maturity:

If A > K(Solvency), exercise the call option and realize a value of (A-K).

If A < K(Insolvency), do not exercise the call option and the value is 0.

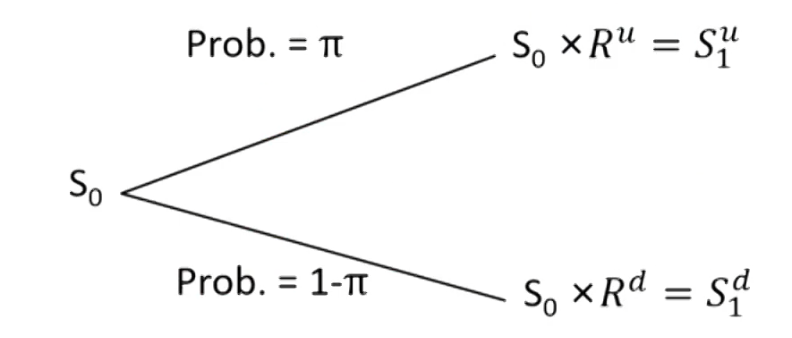

Valuing a Derivative Using a One-Period Binomial Model

Binomial Model

One-period binomial model

Binomial model is based on the idea that, over the next period, some value will change to one of two possible values.

To construct a binomial model, we need to know the beginning asset value \left(\mathrm{S}_0\right), the size of the two possible changes \left(R^u, R^d\right), and the probabilities of each of these changes occurring (\pi,1-\pi).

R^u=S_1^u / S_0\gt 1

R^d=S_1^d / S_0\lt 1

\pi=\left[\left(1+\mathrm{r}_{\mathrm{f}}\right)^t-R^d\right] /\left(R^u-R^d\right), risk-neutral probability of an up-move;

1-\pi, risk-neutral probability of an down-move.

With one-period binomial model, the value of an option on stock can be calculated as:

Step 1: Calculate the payoff of the option at maturity in both the up-move and down-move states;

Step 2: Calculate the expected value of the option in one period as the probability-weighted average of the payoffs in each state;

Step 3: Discount this expected value back to today at the risk-free rate.

Risk neutrality

An option's value is not affected by actual (real-world) probabilities of underlying price increases or decreases.

The risk-neutral probabilities are determined solely by the up and down gross returns.

This no-arbitrage derivative value established separately from investor views on risk is referred to as risk-neutral pricing.

Option hedge ratio

The proportion of the underlying that will offset the risk associated with an option.

For call option:

h_c=\frac{c_1^u-c_1^d}{S_1^u-S_1^d}

short h_c underlying to hedge a call

For put option:

h_p=\frac{p_1^u-p_1^d}{S_1^u-S_1^d}

short h_p underlying to hedge a put

Valuing a derivative using binomial model

One-period binomial model

Hedged portfolio: long an option + short h underlying.

V_0=c_0-h \times S_0

The hedged portfolio should have the same value in up-move scenario and down-move scenario.