Prevent undercapitalized financial firms from exploiting their investors by making excessively risky investments.

Ensure that long-term liabilities are funded.

Characteristics of a well functioning financial system

Complete markets有完善的交易功能: instruments available to serve the purposes of people/entities.

Operational efficient低手续费: low transaction costs.

Informationally efficient公开透明: security prices reflect their fundamental values(intrinsic values).

Allocationally efficient资源配置有效: resources go where they are most valuable.

Financial intermediaries市场中介

Financial intermediaries I 撮合交易

Brokers经纪商 help clients buy and sell securities by finding counterparties.代替你交易

Block大宗 brokers provide brokerage service to large traders.

Investment banks provide advice to corporate clients and help them arrange transactions.

Exchanges交易所 provide places where traders can arrange their trades.They have regulatory authorities.

Alternative trading systems (ATSs/ECNs/MTFs) serve the same trading function as exchanges but have no regulatory authority类似交易所促成交易

Many ATSs are known as dark pools because they do not display the orders that their clients send to them.

Financial intermediaries II 有库存

Dealers交易商 trade by buying for or selling from their own inventory, move liquidity through time for market.和你交易

Broker-dealer have a conflict of interest with respect to how they fill their customers' orders.

Primary dealers are dealers with whom central banks trade when conducting monetary policy.

Securitizers buy assets, place them in a pool, then sell securities that represent ownership of the pool.证券化

Depository institutions include commercial banks, savings and loan banks, credit unions, and similar institutions that raise funds from depositors and other investors and lend it to borrowers.

Insurance companies help people and companies offset risks that concern them. Credit default swaps are also insurance contracts. Fraud, moral hazard, and adverse selection often plague insurance markets.

Arbitrageurs buy and sell identical or similar instruments at different prices in different markets. They move liquidity through markets.

Financial intermediaries III 第三方

Settlement and Custodial services help their customers settle their trades and ensure that the resulting positions are not stolen or pledged more than once as collateral.

Clearinghouses清算所 arrange for final settlement of trades. In futures markets, they guarantee contract performance.

Custodians托管方 hold securities on behalf of their clients. These services, which are often offered by banks, help prevent the loss of securities through fraud, oversight, or natural disaster.代理你打理资金

Classification of market

Based on delivery date

Spot markets(现货市场) is the market where deliver happens now.

Futures markets(期货市场) is the market where deliver happens sometime in the future.

Based on maturity

Money markets(货币市场) trade debt instruments maturing in one year or less.

Capital markets(资本市场) trade instruments of longer duration

Based on position and underlying

Traditional markets long public debts and equities and pooled investment vehicles.

Alternative markets include hedge funds, private equity,commodities, real estate securities, collectibles, etc.

Based on capital flow

Primary market is the market where newly issued securities are sold by issuers to investors.

Secondary market is the market where investors trade to each other.

Primary Markets and Secondary Market

Primary Markets

Public offering

IPO (initial public offerings): first-time issues by firms whose shares are not currently publicly traded. The investment bank then lines up subscribers who will buy the security. Investment bankers call this process book building簿记.

In an underwritten offering(包销), the investment bank guarantees the sale of the entire issue.

In a best effort offering(代销), the investment bank acts only as broker, and is not obligated to buy the unsold portion if the issue is undersubscribed.

Seasoned offerings(secondary issues 增发新股):new shares issued by firms whose shares are already trading in the marketplace.IPO后想要继续发行

Private placement(私下配售/定向增发): corporations sell securities directly to a small group of qualified investors.

Shelf registration(上架注册/暂搁注册): corporations sell new issues of seasoned securities directly into the secondary market when they need capital, and when the market is favorable.先上报审批大量债券,需要钱时再安需求发行部分

Dividend reinvestment plan (DRPs): allow shareholders to reinvest their dividends in newly issued shares.股息直接再买入股票

Rights offering(配股): shareholders are given the rights to buy new shares at a discount to the current market price.股东可以打折买股票

Secondary Market

Classified by trading session

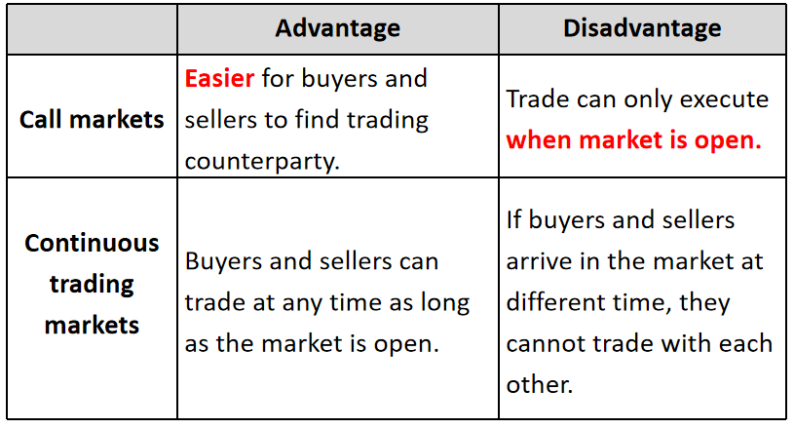

Call market(集合竞价市场)

Trades can be arranged only when the market is called at a particular time and place.结束时集中撮合成开盘价/收盘价

All buy and sell orders are gathered, a single price is chosen to maximize the total volume of trade.撮合成交最大的价格

Continuous market(连续市场)

Trades are arranged and executed anytime when the market is open.

Classified by execution mechanism

Quote-driven markets(报价驱动市场)直接找做市商买

Also known as price-driven markets, dealer markets, or over-the-counter(OTC) markets, customers trade at the prices quoted by dealers.

Brokered markets(经纪人市场)让代理人帮我买

Brokers arrange trades among their clients.

This service is valuable when a client has a unique or illiquid instrument for which finding a buyer or a seller willing to trade is difficult.(E.g. Block trade).很难交易才去找代理人帮忙

Order-driven markets(订单驱动市场)

Order matching rules: establish an order precedence hierarchy Price priority价格优先: the highest priced buy orders and the lowest priced sell orders are traded first. Display precedence展示优先: displayed quantities at a given price have precedence over undisplayed quantities. Time precedence时间优先: earliest arriving orders with the sam display status at a given price are traded first.

Trading pricing rules: determine the price after orders are created using order matching rules. Uniform pricing rule: all trades are executed at the same price that maximizes the trading volume.如集合竞价 Discriminatory pricing rule: the limit price of the order that first arrived is the trade price.如连续竞价 Derivative pricing rule: prices are derived from other market.

Classification of assets

Based on underlying characteristic

Securities

Fixed income

Bills, notes, bonds

Commercial paper商业票据, certificate of deposit大额存单, repurchase agreements(repos)回购协议

Convertible debts

Equities

Common shares, preferred shares, warrants

Public securities: are traded on exchanges or through securities dealers and are subject to regulatory oversight.

Private securities: are not traded in public markets which are often illiquid and not subject to regulation.

Other assets

Currency

Primary reserve currencies(the US dollar and the euro)

Secondary currencies(the British pound, the Japanese yen, the Swiss franc)

Commodities

Precious metals, energy products, industrial metals, agricultural products, and carbon credits.

Real Assets

Real estate, airplanes, machinery, or lumber stands

Real estate investment trusts (REITs) and master limited partnerships (MLPs)

Positions

Long and short position

A position((头寸)in an asset is the quantity of the instrument that an entity or a people owns or owes.

Long positions(多头头寸)benefit from an appreciation in the prices of the assets or contracts owned.

Examples: purchase stocks/bonds/calls/futures/forwards, sell or write puts.

Short positions(空头头寸)benefit from a decrease in the prices of the assets or contracts sold.

Examples: sell short, purchase puts, sell or write calls/futures/forwards.

Short Selling融券卖空

Investor borrows stock and sells it.

need margin需要向出借人交保证金

Repurchases the stock and returns it to the lender (covers the short position).

Short seller's profit (loss) is the original selling price minus the repurchase price (interest, commissions).

Unlike a long position, the potential gains on a short position are limited to no more than 100 percent whereas the potential losses are unlimited

Payments-in-lieu (向出借人支付借用期间的股利): short sellers pay the securit'lenders all dividends or interest that they otherwise would have received had they not lent their securities.

Short sellers must deposit the proceeds(卖掉借来的产品的收益) of the short sale with the security lenders as collateral. 一般由代理机构管理卖出股票的收益

Short rebate rate: Security lenders invest the collateral in short-term securities and may return a portion of interest earned to the short sellers.来自代理机构的返点

Short rebate rate is the difference between interest rate from investing collateral and implicit loan fees(融券成本).

The implicit loan fees are affected by the availability of the security, the investment risk of collateral and the default short sellers.

The short rebate rate may be very small or even negative

Leveraged Position杠杆融资

Buy on margin (保证金交易): investors buy securities by borrowing some of the purchase price.部分资金来自借款

The borrowed loan is called the margin loan/borrowed fund(借来的钱,保证金贷款), the interest rate is called money rate(保证金贷款利率)

Buyer's equity自有资金 is the portion of the security price that belongs to the buyer.

Financial leverage ratio财务杠杆率,放大倍数 = value of the position / buyer's equity

Initial margin requirement(初始保证金): the minimum fractio of the purchase price that must be buyer's equity.

Maintenance margin requirement(维持保证金): the minimum amount of equity in buyer's position,

Margin call(追加保证金): if the value of the equity falls below the maintenance margin requirement, the buyer will receive a request for additional equity, or the position will be liquidated

Bid price is the price at which a dealer or various other proprietary traders is willing to buy a security.

The best bid is the highest bid in the market.

Ask/offer price is the price at which a dealer or various other proprietary traders is willing to sell a security.

The best ask/offer is the lowest ask/offer in the market.

Bid-ask spread is the difference between bid and ask price

Bid-ask spreads are an implicit cost of trading.

Execution Instructions执行指令

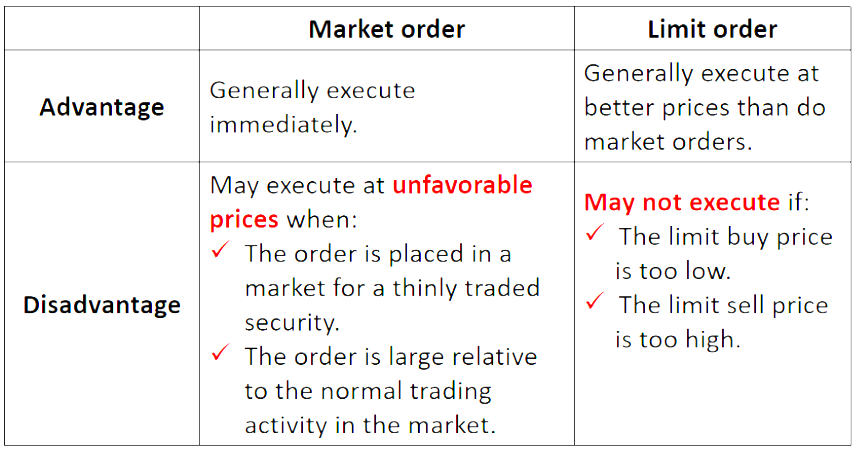

Market orders(市价指令) instruct the broker to buy or sell immediately at the best current price.

Limit orders (限价指令) instruct the broker to obtain the best price immediately available, but in no case accept a price highe than a specified limit price when buying or accept a price lower than a specified limit price when selling.确定一个底线价格,结果不会更差

A limit buy/sell order is aggressively priced when the limit price is high/low relative to the market prices.

Marketable limit orders: at least part of the order can trade immediately.确保部分可以立即执行

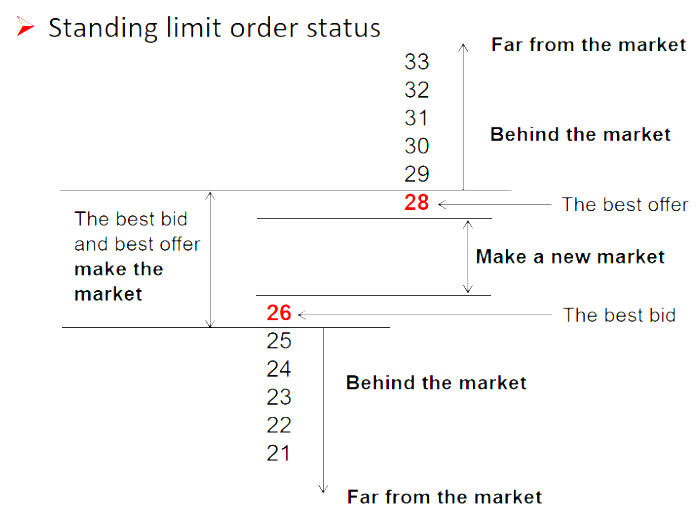

Standing limit order status

Make the market: a limit buy order placed at best bid, or a limit sell order placed at best ask.和最价相同,但比前人后成交

Make a new market: a limit buy/sell order placed between the best bid and the best ask.比最价高一些,排在第一

Behind the market: a limit buy order placed below the best bid, or a limit sell order placed above the best ask.比最价低一些,排在第二

Far from the market: a limit buy order placed considerably below the best bid, or a limit sell order placed considerably above the best ask.比最价低,排在后面

Take the market: a limit buy order placed at current best ask,or a limit sell order placed at current best bid.接收对手方的价格,可任意立即成交

All-or-nothing(AON) orders can only trade if the entire sizes can be traded.要么全部成交要么等

Hidden orders(隐藏指令) are exposed only to broker/exchange.只有经纪人和交易所知道

Iceberg orders(冰山指令) expose only the display size, the rest of the orders is hidden from the public始终只向公众显示部分数量,直到全部成交

Validity Instructions时效指令

Immediate-or-cancel (fill-or-kill IOC/FOK) orders cancel immediately if they cannot be filled in part or in whole.要么全部成交要么取消

Day orders(当日有效指令) expire if unfilled by the end of the trading day.

Good-till-cancelled(GTC) orders are valid until the orders are cancelled.一直有效除非撤单

Good-on-close orders can only be filled at the close of trading.只在收盘有效,收盘价当成交价

Good-on-open orders can only be filled at the open of trading.只在开盘有效,开盘价当成交价

Stop orders(止损指令) cannot be filled until the stop price condition has been satisfied.达到特定价格,order才可以生效

For a stop sell order通过卖出止损, the execution is suspended until a trade occurs at or below the specified stop price. Stop loss on long position触发后卖出股票

For a stop buy order通过买入止损, the execution is suspended until a trade occurs at or above the specified stop price. Stop loss on short position触发后买入股票

Can be set as market confirmation price for traders.

Stop orders reinforce market momentum追涨杀跌

Clearing Instructions清算指令

Clearing instructions tell brokers and exchanges how to arrange final settlement of trades.

These instructions indicate what entity is responsible for clearing and settling the trade. For retail trades, that entity is the customer's broker. For institutional trades, that entity may be a custodian or another broker

Security Market Indexes

Index and Index Return

Definition of security market indices

A security market index represents a given security market,market segment, or asset class.

proxies for specific asset classes in asset allocation models

basis for new investment products

benchmark for evaluating portfolio performance

不能用来measure risk

The individual securities included in a security index are known as constituent securities(成分证券).

Index return and value concepts

A price return index(价格回报指数) reflects only the prices of constituent securities.只考虑股价变动带来的的收益

A total return index(总回报指数) reflects not only the prices of the constituent securities but also the reinvestment of all incomes received since inception.考虑再投资和股利的收益

As time passes, the value of the total return index will exceed the value of the price index.

The divisor is a number initially chosen at inception so that the index has a convenient initial value, such as 1000.

Index return

The value of a price return index is calculated as: V_{P R I}=\frac{\sum_{i=1}^N n_i P_i}{D}

Where: \mathrm{V}_{\mathrm{PRI}}=The value of the price return index; n_i=The number of units of constituent security i held in the index portfolio \mathrm{N}=The number of constituent securities in the index; P_i=The unit price of constituent security i; D=The value of the divisor.

Calculation of single-period price returns P R_I=\frac{V_{P R I1}-V_{P R I0}}{V_{P R I0}}

Where: \mathrm{PR}_1=the price return of the index portfolio; V_{P R I1}=the value of the price return index at the end of the period; \mathrm{V}_{P R I0}=the value of the price return index at the beginning of the period P R_I=w_1P R_1+w_2P R_2+\cdots+w_N P R_N

Where: \mathrm{PR}_1=the price return of constituent security i; \mathrm{W}_{\mathrm{i}}=The weight of security i; \mathrm{N}=The number of securities in the index.

Calculation of single-period total returns T R_I=\frac{V_{P R I1}-V_{P R I0}+I n c_I}{V_{P R I0}}

Where: \mathrm{PR}_1=the price return of the index portfolio; \mathrm{V}_{\mathrm{PRI1}}=the value of the price return index at the end of the period; V_{\text {PRIO }}=the value of the price return index at the beginning of the period. Inc_1=The total income from all securities in the index. T R_I=w_1T R_1+w_2T R_2+\cdots+w_N T R_N

Where: \mathrm{TR}_1=the total return of constituent security i; W_i=The weight of security i; \mathrm{N}=The number of securities in the index.

Calculation of index values over multiple time periods V_{P R I T}=V_{P R I0}\left(1+P R_{I1}\right)\left(1+P R_{I2}\right) \ldots\left(1+P R_{I T}\right)

Where: \mathrm{V}_{\mathrm{PRI0}}=The value of the price return index at inception; \mathrm{V}_{\mathrm{PRIT}}=The value of the price return index at time T; \mathrm{PR}_{\mathrm{IT}}=The price return on the index over period\mathrm{t}, \mathrm{t}=1,2, \ldots . \mathrm{T}. V_{P R I T}=V_{P R I0}\left(1+T R_{I1}\right)\left(1+T R_{I2}\right) \ldots\left(1+T R_{I T}\right)

Where: \mathrm{V}_{\mathrm{PRI0}}=The value of the total return index at inception; \mathrm{V}_{\mathrm{PRIT}}=The value of the total return index at time T; \mathrm{TR}_{\mathrm{IT}}=The total return on the index over period\mathrm{t}, \mathrm{t}=1,2, \ldots . \mathrm{T}.

Index Types

Uses of security market indices

Gauges仪表盘 of market sentiment敏感度

Proxies for measuring and modeling returns, systematic risk, and risk-adjusted performance.反映系统性风险

Proxies for asset classes(如股票,大宗商品) in asset allocation models.

Benchmarks for actively managed portfolios.主动管理

Model portfolios for such investment products as index funds and ETFs.被动管理

Different index types

Equity indices

Fixed-income indices

Alternative investment indices

Equity index

Broad market indices总体市场指数 represent an entire equity market.

Shanghai Stock Exchange Composite综合 Index(SSE),The Russell 3000.

Multi-market indices多市场指数 comprise indices from different countries.

MSCI International Equity Indices.

Fundamental weighting基本面加权 in multi-market indices weight the securities within each country by market capitalization and weight each country in proportion to its relative GDP.

Sector indices板块指数 represent different economic sectors.

Style indices风格指数 represent securities classified according to market capitalization, value, growth, etc.如大市值、成长类

Fixed-income index

Broad universe数量多

Fixed-income securities can be classified along many dimensions: issuer, maturity, currency, credit quality, etc.

High turnover成分更新快

Securities mature.

Dealer markets场外多 and illiquidity缺少流动性

Index providers rely on dealers for prices or must estimate the prices by themselves.

Difficult to replicate fixed-income index

Least likely constructed beacuse of coupon

Alternative investment indices

Real estate indices房地产指数

Categorized as appraisal indices按估值, repeat sales indices根据实际交易,偏向活跃交易, and REIT indices根据基金.

Commodity indices大宗商品指数

Consist of futures contracts on commodities.

Potential Problem: The performance of commodity indices can be quite different from their underlying commodities.期货指数与现货的差异

Hedge fund indices对冲基金指数

Reflect returns on hedge funds.

Index providers rely on the voluntary cooperation of hedge funds.可能报喜不报忧

May have survivorship bias幸存者偏差.

Index construction and management指数编制

Index construction steps

Index weighting

Which target market should the index represent?

Which securities should be selected from that target market?

How much weight should be allocated to each security in the index?

When should the index be rebalanced?

When should the security selection and weighting decision be re-examine?

Reconstitute and rebalance

Price weighting价格加权

The index value is the arithmetic average of security prices

It's simply done by buying an equal number of shares of each security in the index.相当于每个成分股都买相同份数

Advantage is its simplicity.

Disadvantage

Highly priced securities have a greater influence on index value.偏向于高价格成分股

When a stock split occurs, the divisor is adjusted so that the index value is maintained unchanged.拆股会对指数产生影响,需要调整divisor

Market-capitalization weighting市值加权指数

The weight is determined by dividing a stock's market capitalization by the total market capitalization of the index.

买入的股份数比例等于现实股份数比例

加权计算成分股的涨跌幅,乘以初始值就是当前指数

Advantage is that constituent stock's weight equals to its actual market fraction.

Disadvantage

Firms with larger market capitalizations have a greater influence on the index's value偏向于高市值成分股

momentum tilt疯涨的市值不仅拉偏指数,并且权重变大,拉偏效应更加明显

Float-adjusted market-cap weighting(流通市场加权)

The weight is determined by adjusting its market capitalization for its market float, which is the number of shares available to the investing public.只考虑自由流通的股票

E.g., Excluding shares held by controlling shareholders,strategic investors.排除大股东

Further reduce the number of shares by excluding shares not available to foreign investors.更进一步,只考虑本国外国都能投资的部分

Equal weighting等权重加权

Each constituent security has an equal weight. The index is matched by investing equal dollar amount in each stock.

权重加在投资金额,每个股票买同样的净额

成分股涨跌幅的平均值就是指数的变动幅度

Index return is the arithmetic mean of HpRs on index stocks.

Advantage is its simplicity.

Disadvantage

Small-cap bias: small-cap stocks are over-presented because it is over-weighted and has greater volatility.偏向于小市值成分股

Requiring frequent rebalance as prices change.成分股涨跌导致金额不再等权重,需要调整持仓使得再次等金额

Fundamentally weighting基本面加权

This method uses measures of a company's size that are independent of its security price to determine the weight on each constituent security.

These measures include book value,cash flow, revenues, earnings, dividends, and number of employees.根据基本面计算权重

It leads to indexes that have a "value" tilt.偏向于价值股

It leads to indexes that have a contrarian effect.可能有反转效应,表现变好却导致权重下降

Rebalancing再平衡 and Reconstitution重建

Rebalancing refers to adjusting the weights of the constituent securities in the index.调整成分股权重

Price-weighted indexes are not rebalanced because the weight of each constituent security is determined by its price.不用再平衡

For market-capitalization-weighted indexes, rebalancing is less of a concern because the indexes largely rebalance themselves.少量再平衡

Market-capitalization weights are only adjusted to reflect mergers, acquisitions, liquidations, and other corporate actions between rebalancing dates.

Equal-weighted indexes requires most frequent rebalancing频繁再平衡

Reconstitution refers to the process of changing the constituent securities in an index.调整成分股

Constituent securities that no longer meet the criteria are replaced with securities that meet the criteria.剔除

Reflect changes in the target market (bankruptcies, de-listings,mergers, acquisitions, etc.).

Reconstitution is part of the rebalancing cycle.是再平衡的特例

Market Efficiency

Market Efficiency Concepts

Efficient market hypothesis

Market efficiency concepts

Three forms of market efficiency

Implications of market efficiency

Informationally efficient market

A market in which asset prices reflect new information quickly and rationally

A passive investment strategy is preferred to an active investment strategy due to lower costs.主动管理无效

Prices react only to the "unexpected" information.只有未预期的信息会影响价格

Market value vs. intrinsic value

Market value is the price at which an asset can currently be bought or sold.

Intrinsic value (内在价值) is the value if investors had a complete understanding of asset's investment characteristics.

In an efficient market, market prices accurately reflect intrinsic values.不会出现高估或低估

Factors affecting a market's efficiency

Market participants

The larger the number of participants, the more efficient the market.

Information availability

Limits to trading

Limits to trading, such as arbitrage, short selling, will impede market efficiency.

Transaction costs and information-acquisition costs

Regulatory restrictions on insiders trading contribute to market efficiency

Transaction costs and information-acquisition costs

Transaction costs交易成本: "efficient" should be viewed as efficient within the bounds of transaction costs. These bounds of arbitrage are relatively narrow in highly liquid markets, such as the market for Us Treasury bills, but could be wide in illiquid markets.

Information-acquisition costs获得信息的成本: in equilibrium, if markets are efficient, returns net of such expenses are just fair returns for the risk incurred. The modern perspective views a market as inefficient if, after deducting such costs, active investing can earn superior returns

Roles for portfolio manager in efficient markets

Establish portfolio risk/return objectives组合投资

Portfolio diversification分散化

Implement asset allocation based on risk/return objectives

Tax minimization

Types of information

Past market information

All historical price and trading volume information

Public information

E.g., Financial statement data (earnings, dividends, changes in management, etc.), financial market data (opening and closing prices, shares traded, etc.)

Private information

Information that has not been disseminated to the marketplace

Three forms of market efficiency

Weak form efficient market

Semi-strong form efficient market

Strong forms of market efficiency

Weak-form efficient market hypothesis

Securities prices reflect all historical prices and trading volumes information.

Investors cannot consistently earn abnormal profit using technical analysis.技术分析无效

Technical analysis (技术分析) involves the analysis of historical trading information in an attempt to identify recurring patterns that can be used to guide investment decisions.

Semi-strong form efficient market

Securities prices accurately and quickly reflect all publicly known and available information.

The semi-strong form encompasses the weak form.

Investors cannot consistently earn abnormal profits using fundamental analysis.基本面分析无效

Fundamental analysis(基本面分析) is the examination of publicly available information and the formulation of forecasts to estimate the intrinsic value of assets.

Strong form efficient market

Securities prices fully reflect both public and private information.

Strong form encompasses semi-strong and weak form.

Insiders cannot consistently earn abnormal returns from trading on private information.内幕交易无效

Market Anomaly市场异象

A market anomaly may be present if a change in the price of an asset or security cannot directly be linked to current relevant information known in the market or to the release of new information into the market.

Market anomalies, if persistent, are exceptions to the notion of market efficiency.

In the widespread search for discovering profitable anomalies,many findings could simply be the product of a process called data mining, also known as data snooping.

Most researchers conclude that observed anomalies are not violations of market efficiency but, rather, are the result of statistical methodologies used to detect the anomalies. As a result, if the methodologies are corrected, most of these anomalies disappear.

On average, the markets are efficient. In other words, investors face challenges when they attempt to translate statistical anomalies into economic profits.

Time-series anomalies

January effect/turn-of-the-year effect: stock returns in January are significantly higher compared to the rest of the months of the year.一月表现好

This may be due to "tax-loss selling" and "window dressing"

Turn-of-the-month effect: returns tend to be higher on the last trading day of month and the first three trading days of next month.月初月末表现好

Day-of-the-week effect: the average Monday return is negative and lower than the average returns for the other four days.周一表现差

Weekend effect: returns on weekends tend to be lower than returns on weekdays.周五表现差

Holiday effect: returns on stocks in the day prior to market holidays tend to be higher than other days.长假前表现好

Momentum and overreaction anomalies

Momentum: securities that have experienced high returns in the short term tend to continue to generate higher returns in subsequent periods价格变动有惯性

Overreaction effect: stock prices will be inflated (depressed) for those companies releasing good (bad) information价格变动总是过度

Can be explained by loss aversion

Cross-sectional anomalies

Size effect: small-cap stocks tend to outperform large-cap stocks on a risk-adjusted basis.小市值表现好

Value effect: value stocks, which are generally referred to as stocks with below-average P/E ratios and P/B ratios, have consistently outperformed growth stocks.价值股表现好

Other anomalies

Closed-end fund discounts: closed-end funds generally trade at a discount from their net asset value (NAV).封闭基金成交价往往会打折

Earnings surprise: slow adjustment of prices for unexpected earnings(earnings surprise).反映过慢

Initial public offerings (IPOs): investors able to buy IPO shares at their offering prices may earn abnormal profits刚刚IPO的股票表现好

Behavioral Finance

Behavioral finance attempts to explain why individuals make the decisions that they do, whether these decisions are rational or irrational.The focus of much of the work in this area is on the behavioral biases that affect investment decisions.

The behavior of individuals, in particular their behavioral biases,has been offered as a possible explanation for a number of pricing anomalies.

Market efficiency and asset-pricing models do not require that each individual is rational-rather, only that the market is rational.只要市场却理性就是有效市场,不论个人是否理性

If individuals deviate from rationality, other individuals are assumed to observe this deviation and respond accordingly.These responses move the market toward efficiency.

If this does not occur in practice, it may be possible to explain some market anomalies referencing observed behaviors and behavioral biases

Behavioral Biases

Loss aversion(厌恶损失): dislike losses more than they like comparable gains. This can explain the overreaction anomaly.

Risk aversion(风险厌恶) refers to the tendency of people to dislike risk and to require higher expected returns to compensate for exposure to additional risk.

Overconfidence(过度自信): place too much emphasis on their ability to process and interpret information about a security, which leads to mispricing.

Information cascades(信息瀑布): transmission of information from those acting first and whose decisions influence others.被信息左右

This behavior is consistent with rationality.

Herding behavior(羊群效应): trading occurs in clusters and is not necessarily driven by information.

Representativeness bias(代表性偏差): assess new information and probabilities of outcomes based on similarity to the current state or to a familiar classification.

Mental accounting(心理账户): keep track of the gains and losses for different investments in separate mental accounts and treat those accounts differently.

Conservatism(固守己见):Investors tend to be slow to react to new information and continue to maintain their prior views or forecasts.

Narrow framing(狭隘效应): focus on issues in isolation and respond to the issues based on how the issues are posed.同一件事,不同表达产生的情感不同

Overview of Equity Securities

Domestic Equity Securities

Characteristics of common shares普通股

Represent an ownership interest in a company.

Share in the operating performance of the company.

Have a residual claim on company's net assets in liquidation.

The payments of dividend are not contractually obligation.可以不付股利

Participate in the governance process through voting rights.投票权

Proxy voting: allows a designated party to vote on the shareholders' behalf.代理投票

Companies can issue different classes不同级别 of common shares, with each class offering different ownership rights.同股不同权

Statutory voting(法定投票): each share represents one vote.

Cumulative voting(累计投票): total voting rights are based on the number of shares owned multiplied by the number of board directors being elected. Shareholders can direct their total voting rights to specific candidates.可以让中小股东合作

Common shares with embedded options

Callable common shares(可赎回普通股): give the issuing company the option (or right), but not the obligation, to buy back shares from investors at a predetermined call price.允许公司低价回购自己的股票

Putable common shares(可卖回普通股): give investors the option (or right) to sell their shares back to the issuing company at a predetermined put price.允许投资者高价卖出自己的股票给公司

Preference share优先股

Preference shares rank above common shares with respect to the payment of dividends and the distribution of the company's net assets upon liquidation.

Characteristics

Similar to debt securities:

The dividends are fixed.

Do not have voting rights.

Do not share in the operating performance of the company.

Similar to common shares:

Preference shares can be perpetual永久的.

Dividends are not contractual obligations.不是强制性发股利

Can be callable or putable.

Cumulative preference shares(可累计优先股): the unpaid dividends in the prior periods accrue over time and must be paid in full before dividends on common shares can be paid.可以累积股利一次性付清

Participating preference shares(参与优先股) entitle the shareholders to receive the standard preferred dividends plus the opportunity to receive an additional dividend if the company's profits exceed a pre-specified level可以参与普通股的股利分配

Convertible preference shares(可转优先股) entitle shareholders to convert their shares into a specified number of common shares.可以转化为普通股

Earn a higher dividend.

Share in the profits of the company.

Benefit from a rise in common shares' price through the conversion.

Have less price volatility than underlying common shares.

Private securities私募股权

Characteristic of private securities

No active secondary markets.非上市公司

Less transparent than public securities.

Greater ability to focus on long-term prospects because there is no public pressure for short-term results

Lower reporting costs.

Potentially greater return for investors once the firm goes public.

Types of private securities investment

Venture capital investments风险投资 provide financing to companies that are in the early stages of development and require additional capital for expansion.

Leveraged buyout(LBO杠杆收购): investors use debt to purchase all of the outstanding common shares of a firm.

Private investment in public equity(PIPE): a public company quickly sell ownership position to private investors.找特定投资者折价出售股票

Non-Domestic Equity Securities

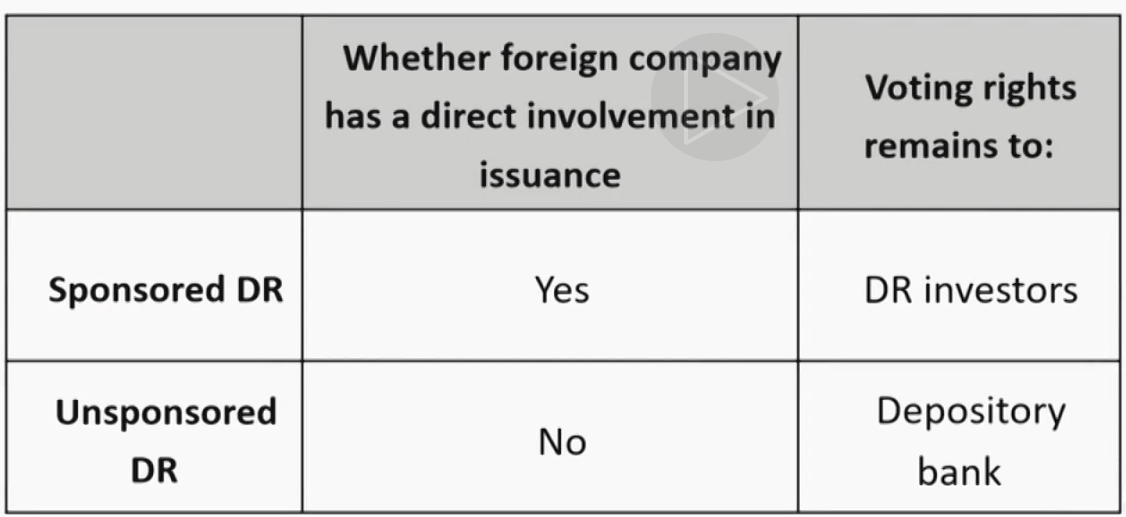

Depository receipts(DRs)(存托凭证): Represent ownership in a foreign company. The price of each DR is affected by factors affecting the price of the underlying shares.存有外国股票的存折,相当于帮你买外国股票,能够享受分红

Sponsored DR(参与型存托凭证): Foreign company has a direct involvement in the issuance新股发行. Investors have the same rights as the direct owners of the common shares.外国公司参与,投资者有投票权

Unsponsored DR(非参与型存托凭证):Foreign company has no involvement with the issuance. Investors have right to receive dividends, but no voting rights, which is held by the issuer of DRs.外国公司不参与,投资者没有投票权

Global depositary receipts(GDRs) are issued outside of the company's home country and outside of the United States.在全球都可以买外国公司股票 Global registered shares are common shares that are traded on different stock exchanges around the world in different currencies.有各种货币的版本

American depository receipts(ADRs) is a Us dollar-denominated security that trades like a common share on Us exchange.在美国买外国公司股票

Basket of listed depository receipts is an exchange-traded fund that represents a portfolio of depository receipts.

Risk and Use of Equity Securities

Risk of equity securities

Equity returns: price change, dividend, and foreign exchange gains (losses) in the case of foreign investments.

Equity risk

Preference shares are less risky than common shares.

Putable shares are less risky than callable or non-callable shares.

Cumulative/participating preference shares are less risky than non-cumulative/non-participating preference shares.

Use of equity securities

To make acquisitions.

To provide option-based incentives to employees.

To finance their operating activities (buy long-lived assets, R&D,etc.).

Market value and book value

Book value of equity = total assets minus total liabilities.

Market value of equity is the stock trading price times number of shares outstanding.

Book value and market value are rarely equal.

Management actions can directly affect the book value, but they can only indirectly affect the market value.

Return on equity

Return on equity (ROE) is used by investors to determine whether the management is efficiently using the equity capital to generate profits.

Both formulas are appropriate to use as long as they are applied consistently.

R O E_t=\frac{N I_t}{\left(B V E_t+B V E_{t-1}\right) \div2} \quad R O E_t=\frac{N I_t}{B V E_{t-1}}

One reason ROE can increase is if net income decreases at a slower rate than shareholders' equity, which is not a positive sign.

ROE can increase if the company issues debt and then uses the proceeds to repurchase some of its outstanding shares. This action will increase the company's leverage and make its equity riskier.

Cost of equity

When a company raises capital by issuing equity, the cost it incurs is called the cost of equity.

Difficult to estimate

The company's cost of equity is often used as a proxy for the investors' minimum required rate of return.

Two models commonly used to estimate cost of equity: the dividend discount model (DDM), and the capital asset pricing model(CAPM).

Introduction to Industry and Company Analysis

Industy Classification

Uses of industry analysis

Understanding a company's business environment.

Identifying active equity investment opportunities.投资机会

Portfolio performance attribution.业绩归因

Industry classification approaches

Product or services supplied按照服务分类

An industry is defined as a group of companies offering similar products or services.

Usually has three layers:

Sector(板块)

Industry(行业)

Company(公司)

E.g.Health Care-Pharmaceutical-GlaxoSmithKline

Representative Sectors

Basic Materials and Processing基础原物料

Industrial/Producer Durables耐用品

Consumer Discretionary非必需品

e.g. automobile

Real Estate房地产

Consumer Staples必需品

e.g. personal care

Technology科技

Energy能源

Telecommunications电信

Financial Services金融服务业

Utilities基础设施

Health Care生命健康

Business-cycle sensitivities按照对经济周期敏感度分类

Companies are grouped on the basis of their relative sensitivity to the business cycle.

Cyclical company顺周期: profits are strongly correlated with the business cycle.(housing, autos,etc.)

Non-cyclical company逆周期: profits are independent of the business cycle. Defensive防御性公司: Basic goods and services with relatively stable demand.(food, health care, etc.) Growth高成长公司: Demand is so strong that the firm is largely unaffected by business cycle.(telecom, cloud computing, etc.)

Limitations

Placement of companies in one of the two groups is arbitrary不一定有周期. Severe recessions may affect all companies.可能遇到大萧条

Different countries frequently progress through the various stages of the business cycle at different times.不同地区的周期不同

Statistical similarities按照统计特征分类

The grouping is based on the correlations of past securities' returns.根据相关系数

Limitations

Often result in non-intuitive不符合直觉 groups of companies.

The composition may vary by time and region.

No guarantee that past correlations will continue in the future.

Carry the inherent dangers of all statistical methods.

Commercial industry classification system

Global Industry Classification Standards (GICS),4 levels, 157 sub-industries, 68 industries, 24 industry groups, and11 sectors

Russell Global Sectors (RGS),3 levels, 9 sectors, 33 subsectors, and 157 industries

Industry Classification Benchmark(ICB), etc. 4 levels,10 industries, 19 supersectors, 41 sectors, and 114 subsectors.

Governmental classification system

Including the International Standard Industrial Classification (ISIC),

Statistical Classification of Economic Activities in the European Community(NACE),

Australian and New Zealand Standard Industrial Classification(ANZSIC),

North American Industry Classification System (NAICS).

Strengths and weaknesses of current system

Information disclosure

The government system do not disclose information about specific business or company.

Commercial system is more transparent.

Update frequency

The government system updated quite infrequently, usually updated only every five years.

Commercial system update more frequently.

Company distinguish

Government system do not distinguish between small and large,for-profit and not-for-profit, and private and public business.

Commercial system distinguishes between small and big companies, include only for-profit public traded companies.

Narrowest classification unit assigned to a company generally cannot be assumed to be fundamentally comparable.

Peer group

Consist of companies engaged in similar business activities whose economics and valuation are influenced by closely related factors.

Often provide a starting point to construct

Steps in constructing a peer group

Examine commercial classification system for identifying companies in the same industry.

Review the subject company's annual report for specific competitors.

Review industry publications to identify comparable companies.

Confirm that companies have similar business activities, demand drivers, cost structure drivers, availability of capital.

Industry Analysis

External factors

Macroeconomic influence: GDP, interest rates, the availability of credit, inflation, etc.

Technological influence: new technologies create new or improved products that can radically change an industry.

Demographic influences: changes in population size, the distributions of age and gender, etc.

Governmental influences: tax, regulations.

Social influences: how people work, spend their money, enjoy their leisure time, etc.

Porter's model

Rivalry竞争 among existing competitors

Threat of new entrants

Threat of substitute products

Bargaining power of buyers

Bargaining power of suppliers

Evaluate the threat of new entrants and the level of competition in an industry

Barriers to entry进入壁垒

Barriers to entry are determined by capital requirements,intellectual capital, regulation, etc.

Industries with low barriers to entry is likely to be competitive,and often have little pricing power.

High barriers to entry do not guarantee pricing power when:

Price is a large component of customers' purchase decision.

Companies have high barriers to exit, which means they are prone to overcapacity.退出门槛高,及时进入门槛低也缺少定价权

Barriers to entry can change over time.

Industry concentration行业集中度

Fragmental industries tend to be highly price competitive.

Concentrated industries do not guarantee pricing power.

Relative market shares have a greater impact on pricing power than absolute market shares.相对市场份额更重要

Market share stability市场稳定性

Market share stability is influenced by barriers to entry,frequency of new product introductions, product differentiation

Stable market shares typically indicate less competitive industries. Unstable market shares often indicate highly competitive industries with limited pricing power.

Industry capacity产能

Under-capacity leads to more pricing power as demand exceeds supply

Over-capacity leads to price cutting and a competitive environment as supply exceeds demand.

Capacity is fixed in the short term and variable in the long term.

Physical capacity is hard to re-deploy, and producers may overshoot long-run demand.

Non-physical capacity (financial and human capital) can be quickly

shifted to new uses.

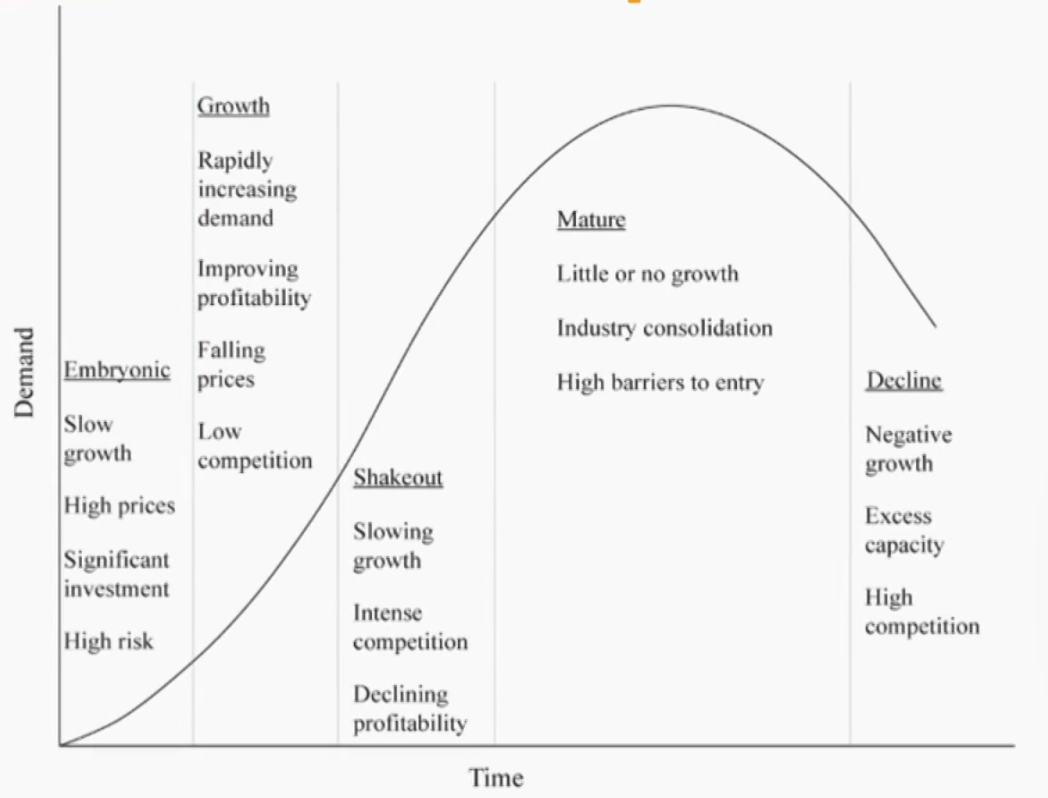

Industry life cycle行业的生命周期

continuous, not discrete

Price competition

Industries for which price is a large factor in customer purchase decisions tend to be more competitive than industries in which customers value other attributes more highly.

Industry life cycle phases

Embryonic stage(初期阶段): the industry is just beginning to develop.

Slow growth: customers tend to be unfamiliar with the products.

High prices: sales and production are not yet sufficient to achieve economies of scale.

Substantial investment is generally required.

The risk of failure is high.

Growth stage(增长阶段):

Rapid growth: demand is fueled by new customers.

Falling prices: economies of scale are achieved, and distribution channels develop.

Improving profitability: sales rise and economies of scale are attained.

Relatively low competition: rapidly expanding demand allows companies to grow without needing to capture market share from competitors.

Threat from new entrants is usually highest as barriers to entry relatively low.

Intense competition: growth becomes increasingly dependent on market share gains.

Increasing over-capacity: company investments exceed demand growth.

Declining profitability: companies cut prices to fill excess capacity Increasing failure

Mature stage(成熟阶段):

Little or no growth: market is saturated and growth is limited to replacement demand and population expansion.

Increasing consolidation: market evolves to oligopoly due to - merges and acquisitions.

High barriers to entry: surviving companies tend to have brand loyalty and efficient cost structures.

Stable pricing: companies are interdependent and try to avoid price wars. But periodic price wars do occur during periods of declining demand

Companies with superior products gain market share and grow faster than industry average.

Decline stage(下降阶段):

Negative growth: demand declines due to technological substitution, social changes, and global competition.

Declining prices: excess capacity, and price wars often occur.

Consolidation: weaker companies exit, merge, or redeploy capital into different products/services.

Limitations of industry life cycle analysis

The evolution of an industry does not always follow a predictable pattern.

Various external factors may cause stages to be longer or shorter,or to be skipped altogether.

Life-cycle models tend to be most useful for analyzing industries during periods of stability.

Not all companies in an industry experience similar performance

Firm's competitive strategy

Cost leadership(low cost)成本领先: lowest costs of production,lowest prices; sell enough volume to earn superior return.

Product or service differentiation差异化: distinctive in terms of type,features, quality, or delivery; achieve price premium.

Spreadsheet Modeling

Although spreadsheet models are a valuable tool for understanding past financial performance and forecasting future performance, the complexity of such models can at time be a problem.

Sector rotation strategy

timing investment to take advantage of business-cycle conditions在经济周期的不同阶段投资对应板块

Equity Valuation:Concepts and Basic Tools

Background of Dividend

Types of Dividend

A dividend分钱 is a distribution paid to shareholders based on the number of shares owned.

Cash dividend现金股利: distribute cash to shareholders, typically paid out regularly at known intervals.

Special/Extra dividends特殊现金股利: dividend that is not regularly paid to shareholders or as a supplement to regular cash dividend.

A stock dividend分股票 is a distribution of additional shares.

Stock split拆股: increase in the shares outstanding with a decrease in share price.(e.g.2-for-1 stock split)

Reverse stock split: reduction of shares outstanding with a increase in share price. (e.g.1-for-20 reverse stock split)

Share repurchase股票回购,买自己的股票: a transaction in which a company use cash to buy back its own shares. Can be viewed equivalent to cash dividends.

Signaling a belief提振信心 that their shares are undervalued;相当于Cash dividend

Flexibility of distributing cash to shareholders;

Tax efficiency省税 in markets where tax rates on dividends exceed tax rates on capital gains;

The ability to absorb increases in outstanding shares because of the exercise of employee stock options.

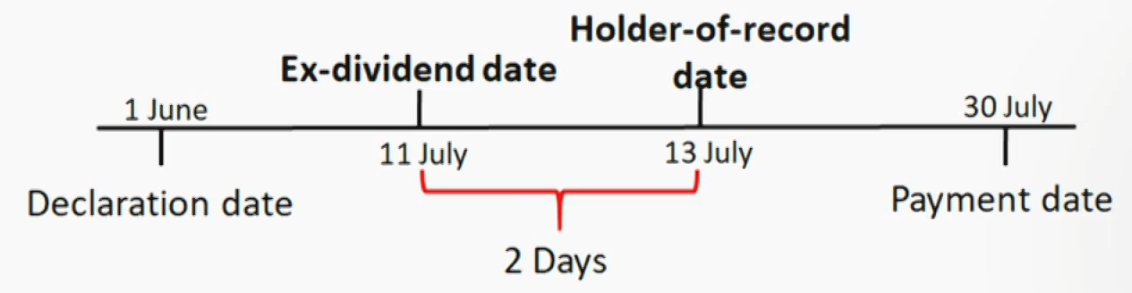

Dividend payment chronology顺序

Declaration date宣布如何分配股利: the day that the corporation issues a statement declaring a specific dividend.宣告派发

Ex-dividend date (ex-date)除息/权日: the first date that a share trades without the dividend.之前买的股票才能享受这一轮股利,之后买的股价扣除股利

Holder-of-record date登记日: the date that a shareholder listed in the corporation's records will be deemed to have ownership of the shares for purposes of receiving the upcoming dividend.这一天登记在册的可以享受股利,因为美国从购买股票到登记入册需要两天

Typically two business days after the ex-dividend date.相差一到两天

Dividend Discount Model

Principal of DDM

Rationale for using the present value models:

Investors expect a rate of return over the investment period.

The value of an investment should equal to the present value of the expected future benefits.

Small changes in model assumptions and inputs can result in large changes in the computed intrinsic value of the security

The intrinsic value of a share is the present value of expected future dividends.

V_0=\sum_{t=1}^{\infty} \frac{D_t}{(1+r)^t}

Where V_0 is the value of a share of stock today; D_t is expected dividend in year t; r required rate of return on the stock.

D_t is hard to predict. If we hold the stock infinitely, it is almost impossible to get an intrinsic value.Thus, we can further discuss the following situations:

N holding period: hold the stock for N period then sell it.

Gordon growth model: assume a sustainable growth rate for dividend.

Preferred share valuation: assume the growth rate of dividend is zero (fixed dividend).

Two stage DDM: assume different stages of dividend growth.

N holding periods Model

The intrinsic value is the present value of the expected dividends for n periods plus the present value of the expected price in n periods.

V_0=\frac{D_1}{(1+r)^1}+\cdots+\frac{D_n}{(1+r)^n}+\frac{P_n}{(1+r)^n}

Where, \mathrm{V}_0=is value of a share of stock today, at \mathrm{t}=0; D_n=expected dividend in period n, assumed to be paid at the end of the year; r=required rate of return on the stock; P_n=the sell price after N period (terminal value).

The Gorden growth model

The Gordon Growth Model assumes dividends grow indefinitely at a constant rate.红利永续增长

Assumptions of the Gordon Model:

The dividend growth rate is forever and never change.

The required rate of return is constant over time

The dividend growth rate is less than the required rate of return.

The formula of GGM:

V_0=\frac{D_1}{\mathrm{r}-g_c}=\frac{D_0\left(1+g_c\right)}{\mathrm{r}-g_c}

Where, g = \text{retention rate}\times ROE=(1-\text{dividend payout ratio})\times ROE

Prefered Stock Valuation

Preference stock valuation as a special case of Gordon growth model if we assume zero growth (fixed dividend).

For a non-callable, non-convertible perpetual preferred share paying a dividend D each period, and assuming a constant required rate of return r over time:

V_0=\frac{D}{r}

For a non-callable, non-convertible preferred stock with maturity at time n, the estimated intrinsic value can be estimated by

V_0=\frac{D_1}{(1+r)^1}+\cdots+\frac{D_n}{(1+r)^n}+\frac{F}{(1+r)^n}

Two-stage DDM Model

Assumes the company experiences an initial and finite period of high growth, followed by an infinite period of sustainable growth

Appropriate for a company already moved through its growth phase and is currently in the transition phase prior to moving to the maturity phase.

The Gordon growth model is used to estimate the terminal value at the end of period of high growth.

For most publicly traded companies (that is, companies beyond the start-up stage), practitioners assume growth will ultimately fall into three stages: growth、transition、maturity.

This assumption supports the use of a three-stage DDM, which makes use of three growth rates: a high growth rate for an initial finite period, followed by a lower growth rate for a finite second period, followed by a lower, sustainable growth rate into perpetuity.

For company that just entering the growth phase

The formula of DDM:

\begin{gathered}V_0=\sum_{t=1}^n \frac{D_0\left(1+g_h\right)^t}{(1+r)^t}+\frac{V_n}{(1+r)^n} \\ V_n=\frac{D_{n+1}}{r-g_l}\end{gathered}

Free Cash Flow Model

The intrinsic value is the present value of the expected FCFE.

FCFE is a measure of dividend-paying capacity.

FCFE model is appropriate for a non-dividend-paying stock.

FCFE = net income + non-cash charges - investment in working capital -fixed capital investments + net borrowing

Formula:

V_0=\sum_{t=1}^{\infty} \frac{F C F E_{\mathrm{t}}}{(1+r)^t}

Multiplier Models

The method of comparable股票

Price multiple compares the share price with some sort of monetary flow or value.

P/E: Price/每股盈利(EPS)

P/B: Price/Book Value

P/S: Price/每股销售额

P/CF: Price/每股CFO

The comparable method uses a price multiple to evaluate whether an asset is fairly-valued, undervalued, or overvalued relative to a benchmark value

Choices for the benchmark include: the multiple of a closely similar stock, average or median value of the multiple for the industry

Trailing vs. leading price multiples

Trailing price multiples(实际价格乘数) use trailing or current values of the divisor.当前股价除以前一期EPS

E.g. P0/E0

Leading price multiples(预期价格乘数) use leading or forward values of the divisor.当前股价除以预测的EPS

E.g. P0/E1

Price multiples based on fundamentals

The stock value is justified by fundamentals or a discount cash flow model.由基本面信息得到

\begin{align}

&\frac{P_0}{E_1}=\frac{D_1/ E_1}{r-g}=\frac{\text { dividend payout ratio }}{r-g}

\\

&\frac{P_0}{E_0}=\frac{D_1/ E_0}{r-g}=\frac{\text { dividend payout ratio }\times (1-g)}{r-g}

\end{align}

The P/E ratio is inversely related to the required rate of return r,and positively related to the growth rate g.

The relationship between P/E and payout ratio b is ambiguous because a higher payout ratio may imply a slower growth rate

Advantages

Allow for relative comparisons, both cross-sectional and in time series.

Price multiples are popular among investors.

Disadvantages

May generate a contradictive conclusion with those of the discounted cash flow methods.

Differences in accounting standards and/or methods can result in multiples not easily comparable.

The multiples for cyclical companies may be highly influenced by current economic conditions.

Enterprise value multiples企业

Enterprise value = market value of common stock + market value of preferred stock + market value of debt - cash and cash equivalents

Market value of debt is difficult to obtain

Enterprise value is often viewed as the cost of a takeover.

\text{Enterprise Value Multiple}=\frac{\text { Enterprise Value }}{\text { EBITDA }}

Enterprise value is most useful when comparing companies with significant differences in capital structure.适用于不同的资本结构

EBITDA is usually positive.

Asset-based Valuation

Market value of equity = market value of assets - market value of liabilities

Appropriateness for companies which

primarily hold tangible short-term assets尽量是短期有形资产

hold assets with ready market values尽量是市场价

are held privately不是上市公司

cease to operate and are being liquidated.要终止运营

Asset-based valuation is problematic when:

Companies with assets that do not have easily determinable market values.得不到市场价值

Fair values of assets and liability can be very different from their book values.账面价值和市场机制差异大

It may understate value of a company because of some important intangible assets. Thus it gives a "floor" value.往往会低估

Asset values are more difficult to estimate in a hyperin-flationary environment.市场恶性通货膨胀